Broadband M&A 2.0: Strategic discipline replaces pandemic euphoria

Key points

- Broadband M&A activity has accelerated in 2025, driven by lower interest rates, improved economic certainty and renewed strategic interest.

- After a post-COVID correction, large telecom and cable operators—rather than just institutional investors—are now leading deal activity.

- Valuations have moderated from record highs, opening opportunities for smaller strategic buyers to re-enter the market.

- Competitive threats from fixed wireless and LEO satellites are creating both risks and new strategic imperatives for broadband operators.

- Fiber-rich networks remain highly sought after, supported by healthy margins, AI-driven bandwidth demand and ongoing rural buildout needs.

Merger and acquisition activity in the broadband market has been on the rise in 2025. This trend reflects lower interest rates, increased economic certainty, and investors and strategic buyers looking to make up for lost time. Despite heightened competition and less optimistic growth plans than those seen immediately after the pandemic—when record-high valuation multiples were realized—investor interest in broadband assets remains strong. Strategic acquirers are also playing a larger role in deal activity.

In this report, we discuss our expectations for deal activity over the next few years, the factors influencing valuations and the evolving landscape of broadband acquirers.

Post-COVID boom

During COVID and the years that followed, the U.S. economy underwent a digital transformation that underscored the importance and value of broadband networks. This transformation caught the attention of private equity sponsors and infrastructure funds eager to gain exposure to the trend. Additionally, the uncertainty around traditional infrastructure investments (think roads, bridges and airports) were forcing investors to rethink their strategy. Were people going to travel like they did pre-COVID? What will the work-from-home trend look like long term and how will it impact traditional infrastructure projects? As a result, institutional investors went on an aggressive buying spree, investing in companies building fiber networks across a wide range of underserved and unserved markets.

This feverish level of M&A drove valuations to near-record highs.

Reality sets in…

Mike Tyson once said, “Everyone has a plan until they get punched in the face.” The post-COVID hysteria in the broadband market was soon followed by execution challenges, higher interest rates and labor shortages. These developments drove up costs and caused project delays.

Private equity sponsors slowed their deal cadence as investment holding periods stretched. Many private equity-backed operators struggled to meet fiber passings and revenue targets amid these headwinds. Additionally, the high multiples paid in 2023 began to fall as investors failed to realize their expected returns. As a result, many funds opted to hold onto investments longer than planned, hoping that improved execution and market liquidity would lead to higher multiples.

This reality check set the stage for roughly two years of relatively modest M&A activity.

M&A starts to heat up

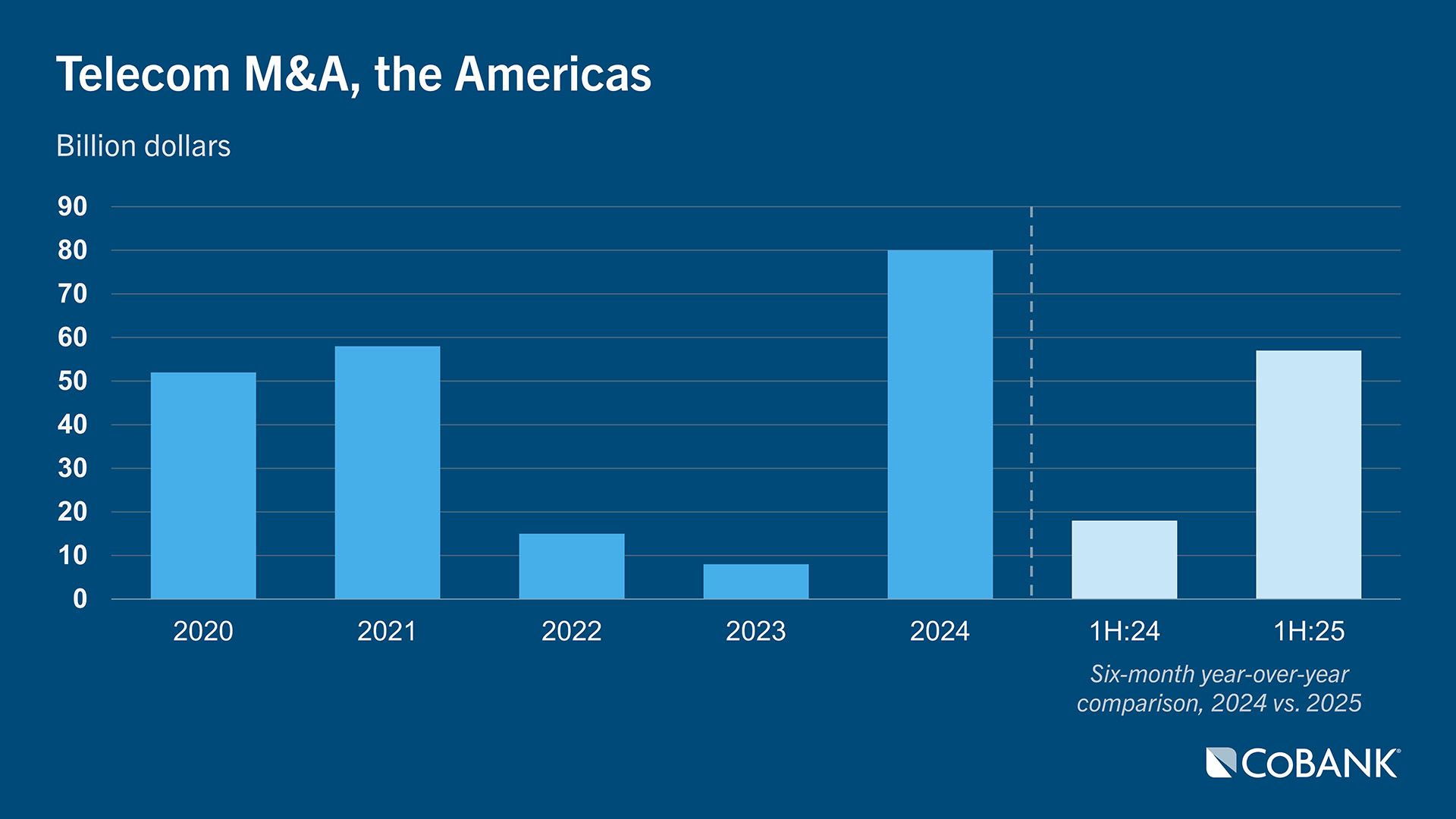

Over the last 18 months, broadband M&A has started to accelerate. Lower interest rates, improved economic certainty and a prolonged slowdown in prior deal flow have all contributed to this resurgence.

However, unlike the post-COVID boom, today’s activity is being driven by large telecom, wireless and cable operators rather than institutional investors. For example, of the roughly 35 deals announced in the first half of 2025, the top five included strategic buyers and accounted for more than 80% of total deal volume.

For wireless operators, owning fiber assets represents both a growth opportunity and a way to reduce wireless churn by bundling smartphone plans with fiber-to-the-home service. The postpaid smartphone market has reached saturation and is evolving into a switcher market. This is forcing wireless operators to look for inorganic growth opportunities. T-Mobile has been the most active strategic buyer, building on its fixed wireless success and disrupting the cable broadband market with its bundled offerings. Large cable operators, struggling to compete with wireless players, are pursuing horizontal integration strategies to gain scale.

What comes next

We expect a steady drumbeat of M&A activity over the next several years, with strategic acquirers playing an increasingly prominent role. During the post-COVID frenzy, deep-pocketed institutional investors often outbid smaller strategic buyers, pushing valuations to unsustainable levels. Now that valuations have normalized and competition for deals has eased, smaller strategics are re-entering the market—but with caution.

These buyers are conducting deep due diligence, including detailed “buy versus build” analyses, and are focusing on geographically strategic opportunities. Many prefer targets located adjacent to their existing markets or within a one-hour drive from their headquarters.

National wireless operators, meanwhile, are likely to pursue deals that address specific strategic needs—such as alleviating wireless network capacity constraints stemming from their fixed wireless service, or filling fiber coverage gaps. Some of the recently announced fiber joint ventures (JVs) may also evolve into “mini aggregators,” rolling up smaller networks under JV structures.

For instance, T-Mobile may leverage its JVs to pursue smaller deals that are strategically valuable but too small for direct acquisition. Metronet’s announced plan to acquire US Internet is a prime example of this approach.

We also anticipate greater focus on integration and operational efficiency. Many of the early fiber rollouts were fueled by growth at any cost, but acquirers today are emphasizing disciplined network buildouts, optimized capital allocation and improved customer retention. Many investors learned that building and running a successful broadband business is harder than it looks. And instead of holding management teams accountable to fiber passings, investors are now focused on value-generating metrics like market penetration and revenue targets.

Private broadband valuations

Private broadband valuations are expected to remain rangebound in the near term. Each operator’s unique mix of assets, growth opportunities, competition, operating structure and leverage makes it difficult to define a precise range. Generally, we see EBITDA multiples for fiber-rich operators with some level of scale and attractive near-term growth prospects in the 14–18x range. Meanwhile, for smaller carriers with robust fiber networks but fewer growth opportunities, we see multiples in the range of high single digits to low teens.

Investor interest in fiber assets remains strong, supported by healthy margins, continued buildout opportunities in underserved areas, and rising bandwidth demand from AI applications. These factors should put a floor under valuations in the coming years.

Conversely, competition and limited pricing power are likely to cap upside potential.

The influx of capital and new technologies has created a more competitive environment than the broadband industry has ever experienced. This heightened competition introduces risks and uncertainties that may limit private valuations for the next several years.

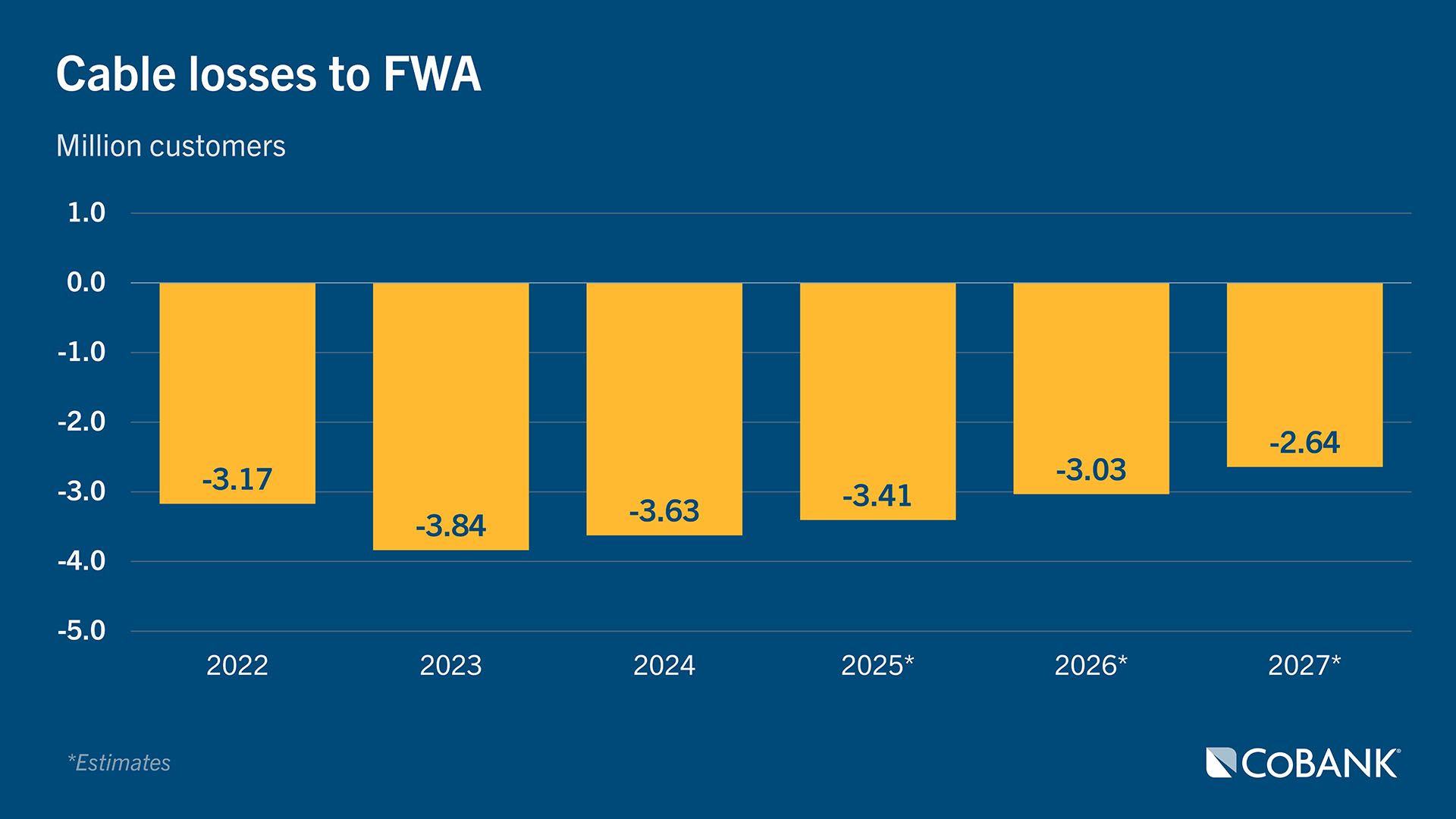

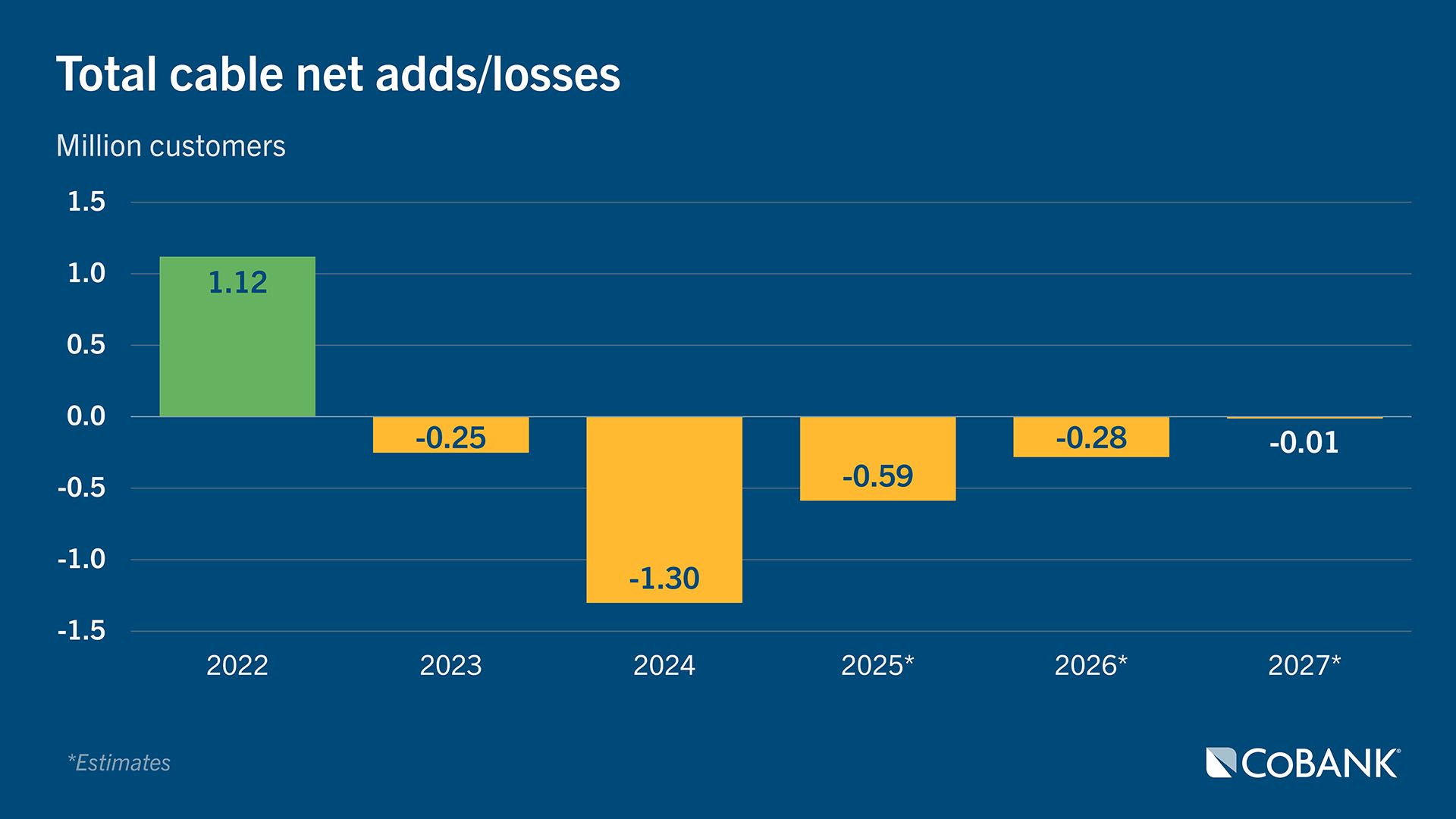

Fixed wireless access (FWA) technologies have had a particularly large impact on publicly traded cable operators, resulting in two consecutive years of broadband subscriber losses. Initially, fixed wireless growth was concentrated in urban and suburban markets where operators had excess capacity. Now, however, it is beginning to encroach on smaller and rural markets, creating new growth headwinds for rural broadband operators.

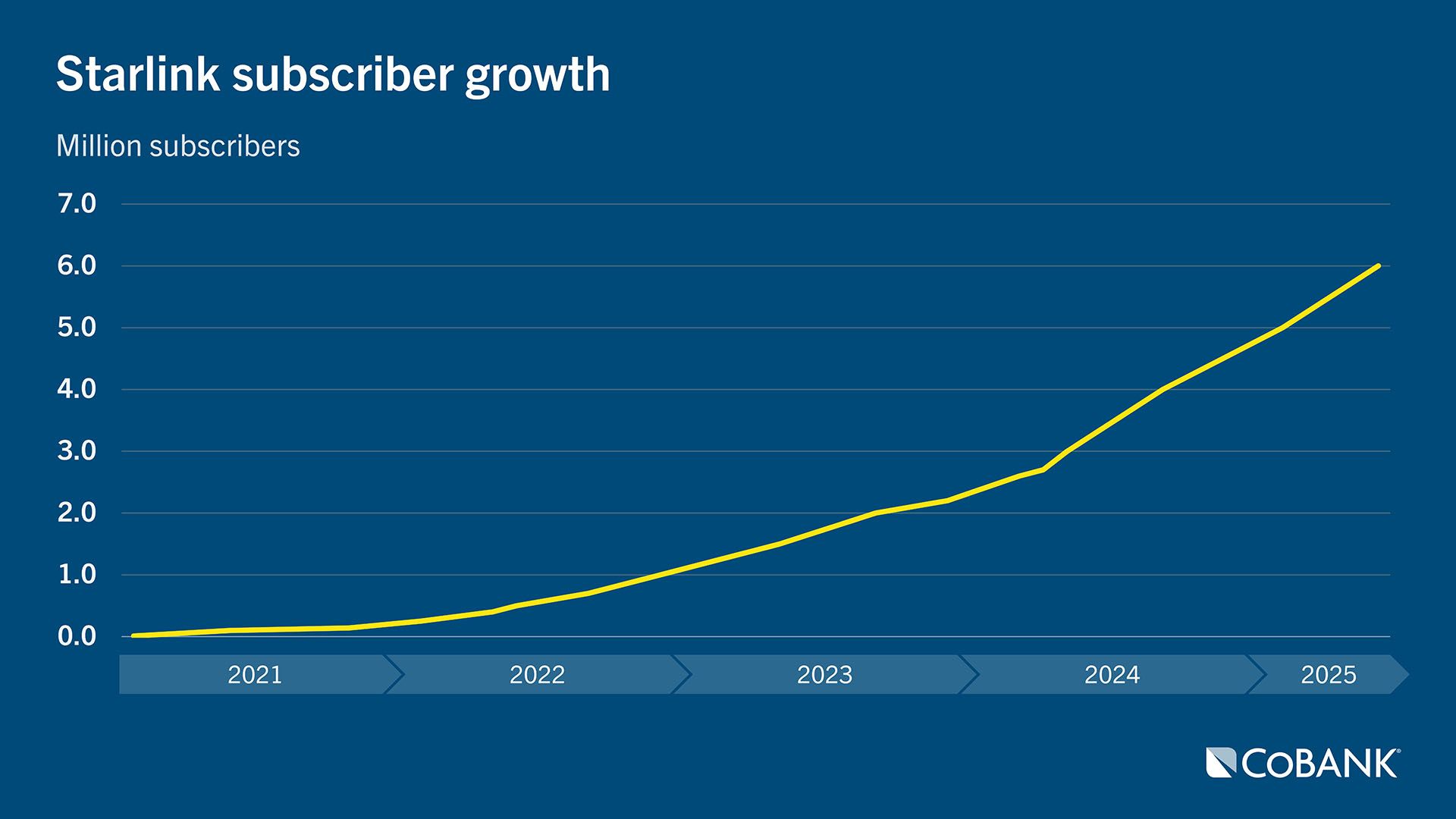

Another emerging threat comes from Low Earth Orbit (LEO) satellites. Starlink—the 800-pound gorilla in this space—has achieved impressive subscriber growth driven by greater network capacity and aggressive pricing. While satellite internet has historically served only remote, unserved customers, that may change as technology improves and Amazon enters the market with its Amazon Leo service.

Given Amazon’s track record of disruption, there’s concern that Amazon Leo could be bundled with Amazon Prime, creating a powerful value proposition—similar to how Prime Video reshaped the media industry. Amazon spends over $20 billion per year on media content that is bundled with Amazon Prime. This service, along with Netflix, has accelerated cord cutting, helped decimate the movie theater industry and fundamentally changed how brands advertise on TV.

Could something similar happen to the broadband industry?

Critics argue that LEO satellites will never match fiber performance, but the same was once said about mobile voice versus landline voice. History shows that “good enough” technology, combined with compelling value, can disrupt incumbents.

Pricing power and margin pressure

Most broadband operators remain hesitant to raise prices by more than roughly 5% annually. With multi-year price-lock guarantees and growing competition, it is becoming increasingly difficult to pass rising costs through to customers. This dynamic is creating margin risk and a valuation ceiling for many operators.

Operators that can pair creative pricing models with a differentiated service will be best positioned to insulate themselves from these challenges. Leaning into the benefits of being small, nimble and local and providing best-in-class service is a winning combination for smaller broadband operators.

Summary

M&A activity in the broadband market has rebounded in 2025, driven by lower interest rates, greater economic certainty and renewed confidence from investors and strategic buyers. Unlike the post-COVID buying frenzy led by private equity sponsors and infrastructure funds, today’s deals are dominated by large telecom, wireless and cable operators pursuing strategic synergies and fiber expansion. Lower valuations and a more reasonable bidding environment have opened the door for smaller strategic buyers to enter the market. While fiber assets remain highly attractive, supported by strong margins and growing AI-driven demand, rising competition from fixed wireless and emerging LEO satellite providers like Starlink and Amazon Leo could pressure pricing and valuations in the years ahead.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.