Ag retailers’ future rides on integrating agronomy and autonomy

Key points

- As ag retailers continue to contend with structural and operational challenges, including higher costs for labor and insurance, their customer is also evolving. Farm operators are demanding more data-enabled agronomic tools and new ways of doing business.

- One driver is sustainability. Focused on the environmental impact of crop farming, consumers and regulators are pressuring growers to reduce their applications of synthetic fertilizer and crop chemicals.

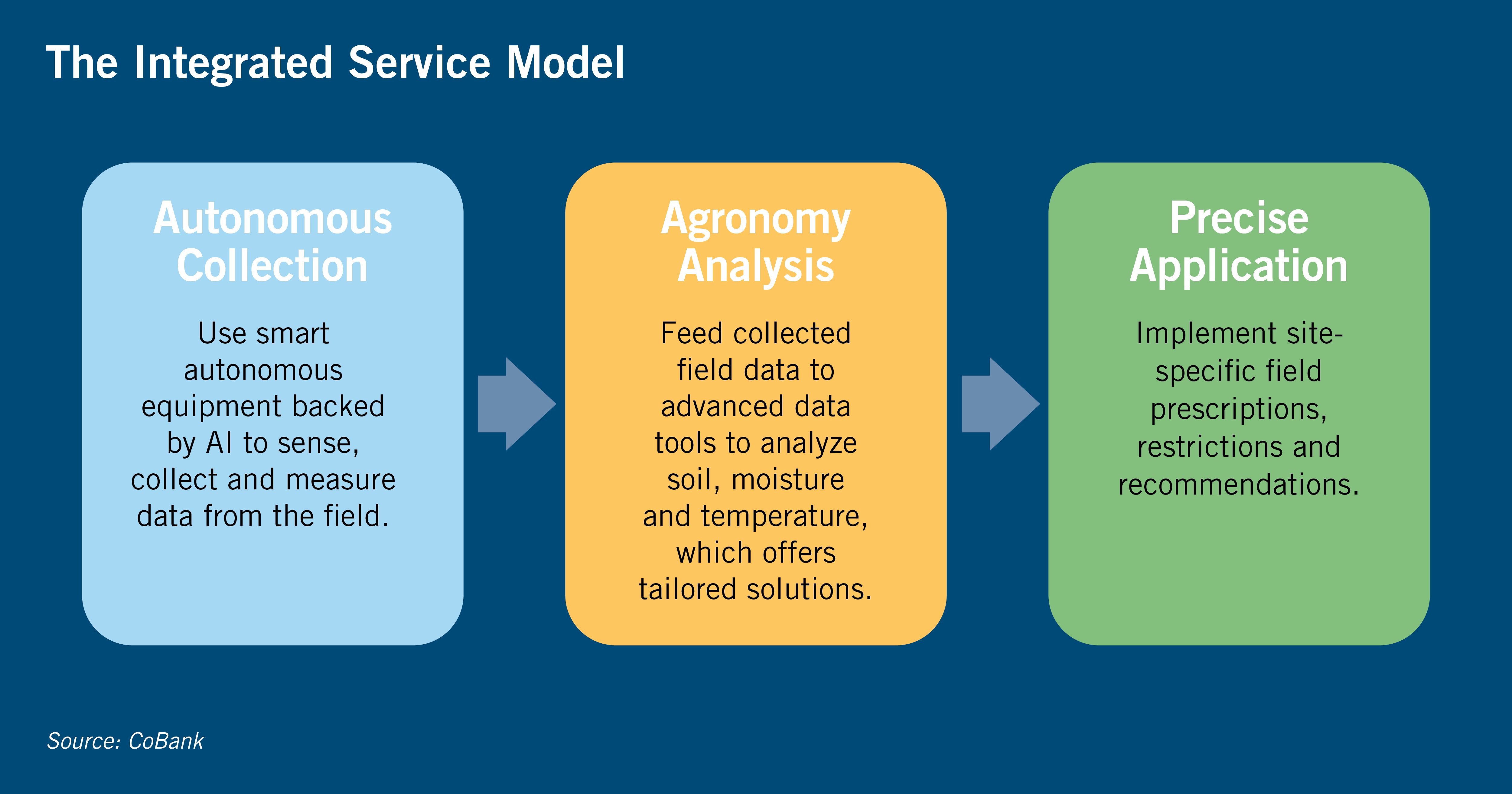

- The bottom line is the current generation of farmers needs more expert advice, while next generation farmers are looking for easy-to-implement, reliable solutions that provide proof they farm in positive ways. Ag retailers could provide the solution with an integrated and tailored service model offering of precision-driven agronomic advice and autonomous AI-powered equipment.

Industry challenges

Ag retailers’ ongoing structural and operational challenges, including labor shortages and consumer resistance to chemical and fertilizer applications, are not going away any time soon. And, two additional pressures have surfaced over the past 18 months — higher insurance costs for health and commercial property and higher costs of capital. A year ago, the federal funds target rate was 2.25%; now it’s 5.25%. Of course, commercial borrowing costs are even higher than that.

Beyond these issues, it’s clear the U.S. farmer is changing. Professional crop producers continue to evolve into more sophisticated, financially savvy rural entrepreneurs. As entrepreneurs who are managing a growing number of acres, these farmers are interested in gaining economies of scale on their operations. And this means becoming a low-cost operator, something that ag retailers know sophisticated customers are willing to pursue with new technology and advanced agronomic practices, augmented by new ways of operating.

These customers are also increasingly interested in collaboration. Over the past year, we have learned about several digitally connected communities of farmers, independent crop advisors, and input suppliers who have the ability to communicate in real time (two examples are XtremeAg and AGvisorPro). These agronomic information-sharing platforms could be precursors to a next-generation retailer where advice is the value-added product, rather than seeds, chemicals and fertilizer — a strategy proposed in previous Knowledge Exchange reports. Some industry practitioners refer to this operating model as a “virtual cooperative,” and if successful, it could disrupt the current ag retailer business model.

| Challenge | Explanation |

|---|---|

| Higher operating costs | Weather-related property catastrophe losses are pushing up costs and limiting availability of commercial property insurance. Higher capital costs (with rising interest rates) and rising wage and benefit costs are two more factors. |

| Labor shortages and mismatches | Attrition and retirements, aging (shrinking number of working age people), urbanization and more restrictive immigration policies have collectively reduced the pool of talent available to be hired by ag retailers. Another factor is competition from other industries, such as mainstream technology firms. |

| Changing customer needs | As their operations grow larger and more financially sophisticated, farmers are more willing to embrace disruptive technologies that reduce physical labor. |

| Consumer litigation and regulatory pressure | Glyphosate, the most widely used pesticide applied on farm fields and residential lawns to eliminate weeds, is the latest pesticide to face restrictions (following the elimination of chlorpyrifos). Other pesticides such as Atrazine, 2,4-D and Dicamba are likely to come under greater scrutiny by both consumer and regulators. Finally, ag retailers and farmers face pressure to reduce fertilizer applications in order to contain nutrient runoff. |

| Source: Agricultural Retailers Association, Meister Media and CoBank ACB. | |

USDA is forecasting that net farm income will decline during 2023, which we believe will carry into 2024. When crop farming income drops—whether from lower commodity prices, higher input costs, or both—farmers typically reduce their input purchases. We have already seen this in 2023 even though fertilizer prices have sharply dropped since the 2022 peak. Another factor is farm consolidation, a natural reaction to a difficult profit outlook. Farm consolidation means fewer customers for retailers, thereby creating more competition for customer wallet share among farm supply cooperatives and independent ag retailers.

Another emerging dynamic is the push for sustainability. As society demands more precise application of synthetic fertilizer and crop chemicals, farmers will need to spend an ever-increasing amount of their crop budgets on advanced precision equipment and technology, as well as staff to operate the new technology. While farmers know how to consolidate acres, there is no proven playbook for consolidating or aggregating enough technical and agronomic talent to produce crops in the future.

The business opportunity

While the list of challenges and changes looks like a problem for ag retailers, it may actually be a new business growth or pivot opportunity. Ag retailers’ next revenue stream could be earned by solving customers’ challenges with an integrated and tailored service model. The ag retailer would deliver customized farmer- and field-specific solutions, derived from the combination of precision agronomy and the new data and information technologies (artificial intelligence) embedded in autonomous equipment. These new revenues could offset a portion of declining input sales in the future.

To develop and capture new sources of recurring revenue, retailers must not only partner and collaborate with precision equipment providers and ag-tech services companies, but also build out internal capabilities to develop, market and sell the integrated solution package. The idea of combining precision agronomy with autonomy will require a new approach with new skill sets and go-to-market strategies.

This “digital agronomy department” would be a profit center focused on digital agronomy, risk management and environmental compliance. Examples of products and services could include:

- Premium data-enabled custom-farming and application services, especially for larger farm operators that are willing to outsource these activities;

- Advanced product delivery and logistical services; and

- Compliance reporting for the growing list of new environmental regulations and certifications that farmers will need to follow, document and report.

The path forward

Making the leap from selling commodity products to integrated services will not be easy. It will first require a willingness by ag retailers to engage and shift into a new selling mindset. Next it will require collaboration with precision equipment providers and outside technology companies to properly recruit, train and develop technical talent. Finally, it will require a growth mindset by senior leadership of the ag retailer, willing to invest and fund the expansion of the new business model while maintaining high service levels for the current product offering.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.