Dairy replacements should begin a slow rebuild in 2027 and 2028

Key points

- The smallest beef cattle herd in 75 years combined with historically high beef prices have motivated dairy farmers to create more beef-on-dairy calves to maximize farm revenue.

- The strong pivot in the beef-on-dairy category has sent dairy replacement inventories to the lowest level since 1978. That, in turn, vaulted dairy heifer replacement values into record territory well over $3,000 per head.

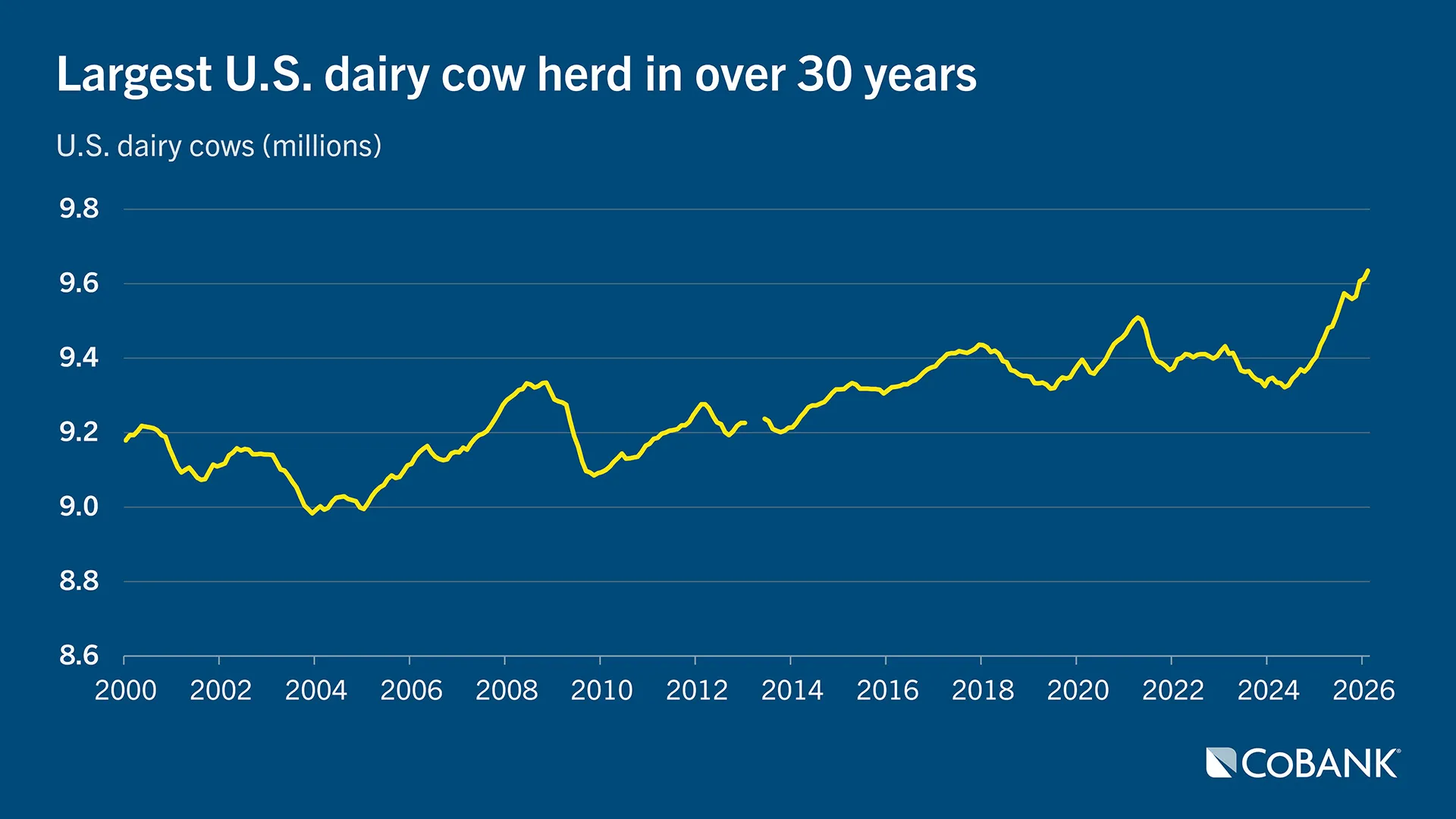

- To compensate for dwindling dairy replacements and continue capitalizing on historic beef prices, dairy farmers have sent fewer dairy cows to slaughter starting in August 2023. The pullback has been so profound that the U.S. dairy herd is now over 9.6 million head, the highest total in 30 years.

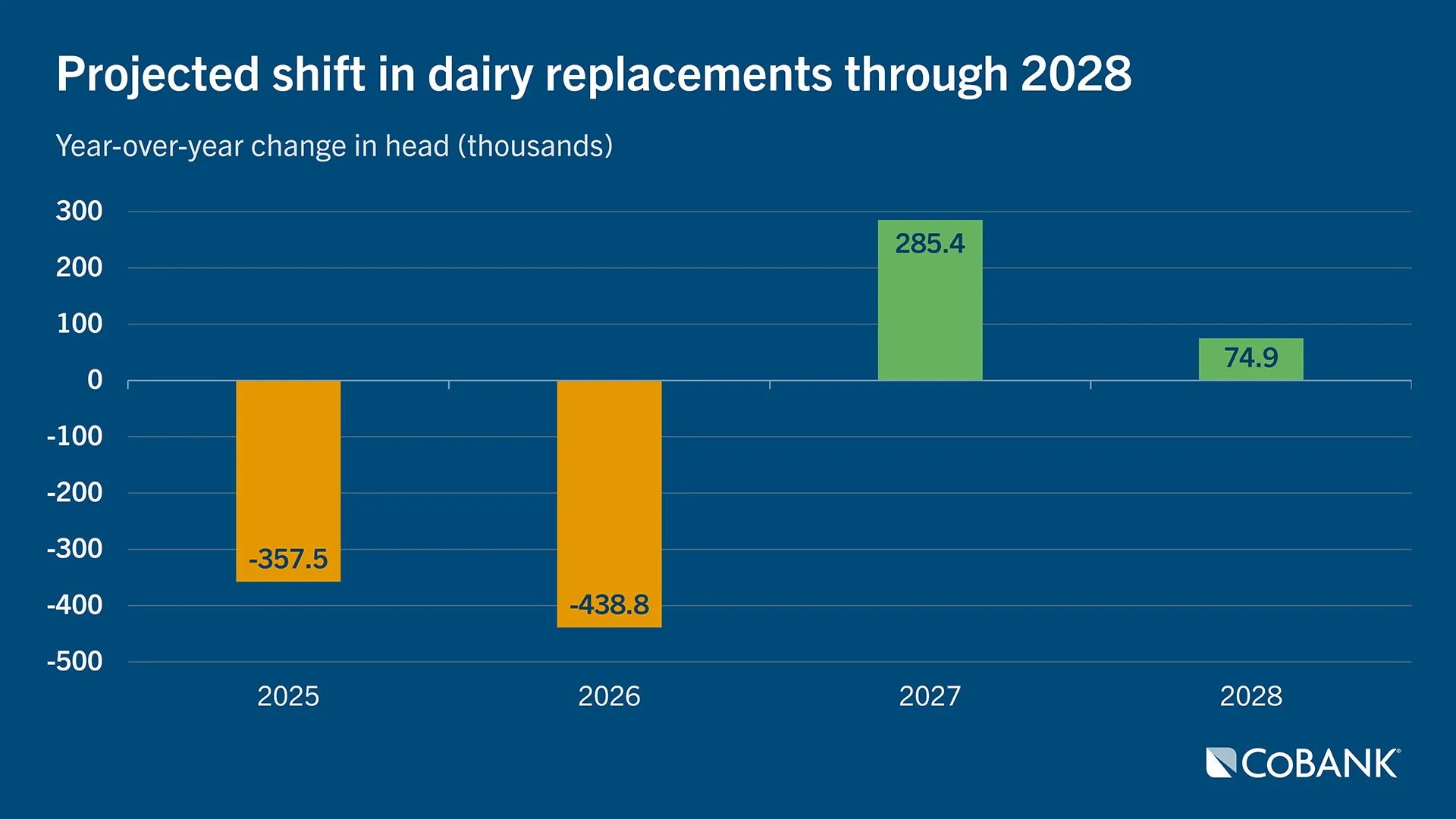

- Dairy replacements entering the milking herd will shrink by a combined 796,000 head in 2025 and 2026. However, shifts in the type of semen sales and patient investment in the dairy herd will help to rebuild dairy replacement numbers by 360,200 head in 2027 and 2028.

Strong consumer demand for high-quality protein is driving record beef prices and double-digit growth in protein-rich dairy products. This combination has created a rare opportunity for dairy farmers to grow revenue from both beef and dairy sales. However, those two revenue streams have different pay days for a farm’s cash flow. Raising dairy replacements from birth to maturity remains a two-year investment while selling beef-on-dairy cross calves is essentially an instant one-time revenue source.

The incentive to cash in on a beef-on-dairy calf a few days after birth is the main reason dairy replacement numbers are historically low. Based on our analysis of semen sales trends from National Association of Animal Breeders (NAAB) data, dairy replacements will remain tight through 2026 and begin to show some recovery in the ensuing years. The following analysis builds upon CoBank’s August 2025 report, Dairy Heifer Inventories to Shrink Further Before Rebounding in 2027 and digs deeper into the situation.

Record beef economics are reshaping dairy decisions

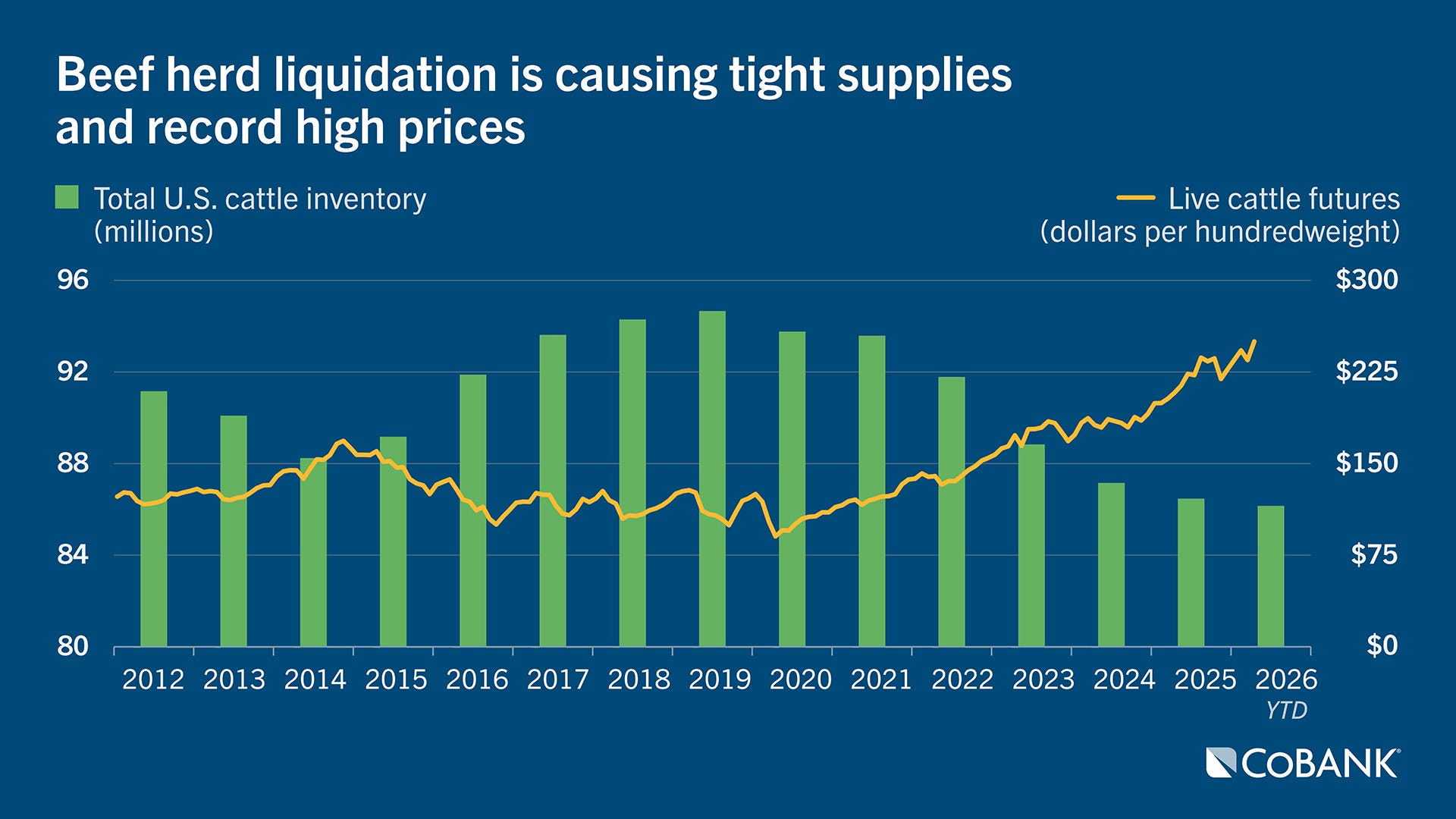

Successive years of drought and weak forage conditions have created a difficult operating environment for the nation’s cattle ranchers. Total cattle inventories most recently peaked at 94.7 million head in 2019 and have since contracted by 8.5 million head. Today’s 86 million head inventory is the lowest since 1951 and helped push live cattle futures to a record $251 per cwt. in May 2026. These prevailing prices are also the reason the cattle industry is not rebuilding, as heifers retained for beef cow replacement are up just 1% from 2025. Overall, the smallest U.S. beef cattle herd in 75 years has opened the door for dairy farmers to capitalize on record margins in this category.

Tight replacement supplies have pushed heifer prices to record highs

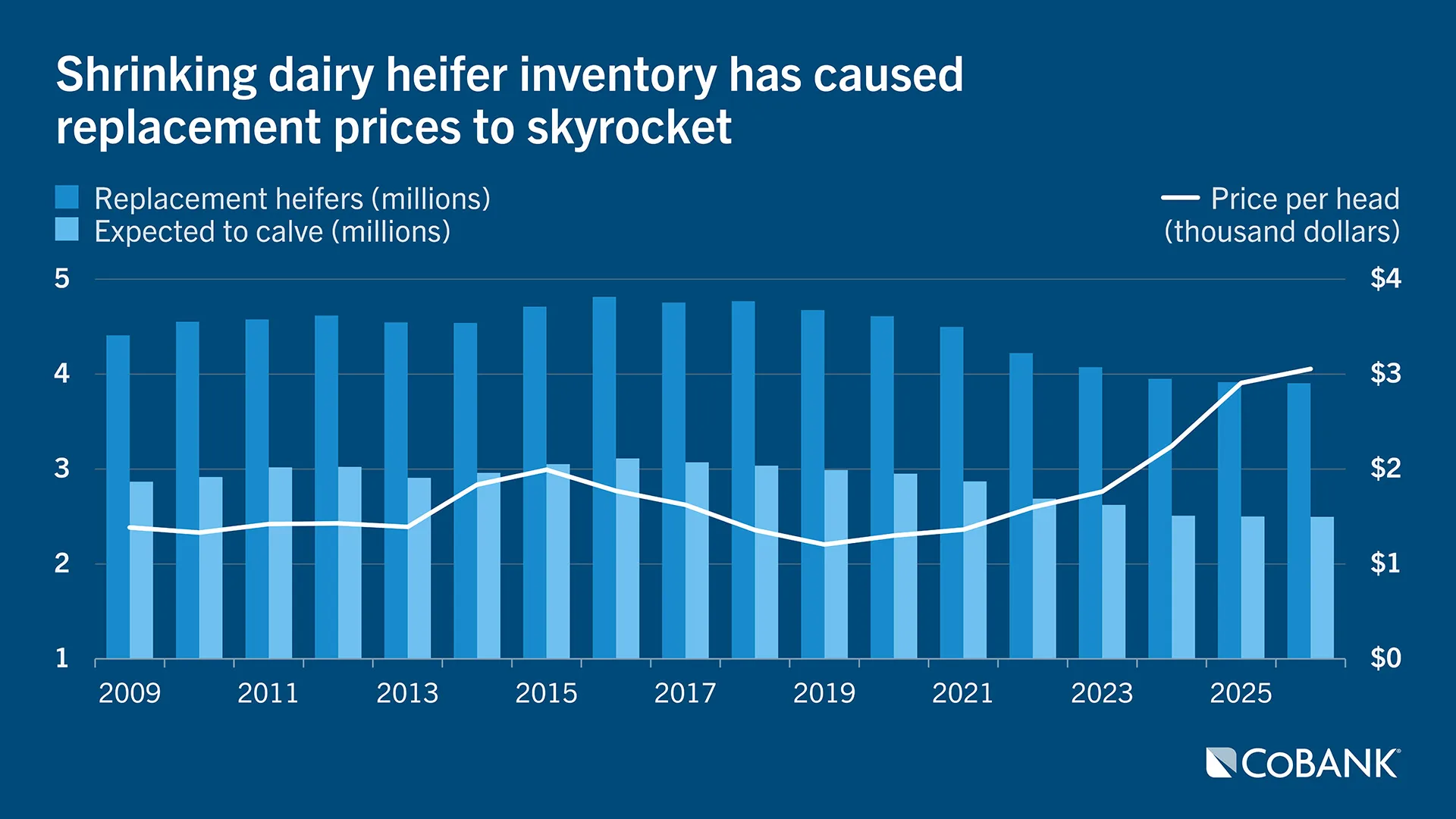

In 2016, U.S. dairy heifer replacement inventories pushed to 4.8 million head. This strong build-up of dairy heifers weighing 500 pounds and over was the response to 2014’s record mailbox price of $24.04 per cwt. By 2016, dairy producer pay prices fell to $15.95 per cwt. This caused replacement prices to drop from $2,000 per head to $1,600 per head in that two-year window. Then came oversupply, which caused dairy replacements to plummet to $1,200 per head by 2019. By this time, dairy heifers had more value in feedlots for beef than in dairy barns for milk, ushering in the beef-semen-on-dairy-cow movement. As a result of these market forces, the inventory of dairy heifers weighing 500 pounds and over shrunk by 909,400 head or 19% from 2016 to 2026.

Dairy heifer inventories remain historically tight

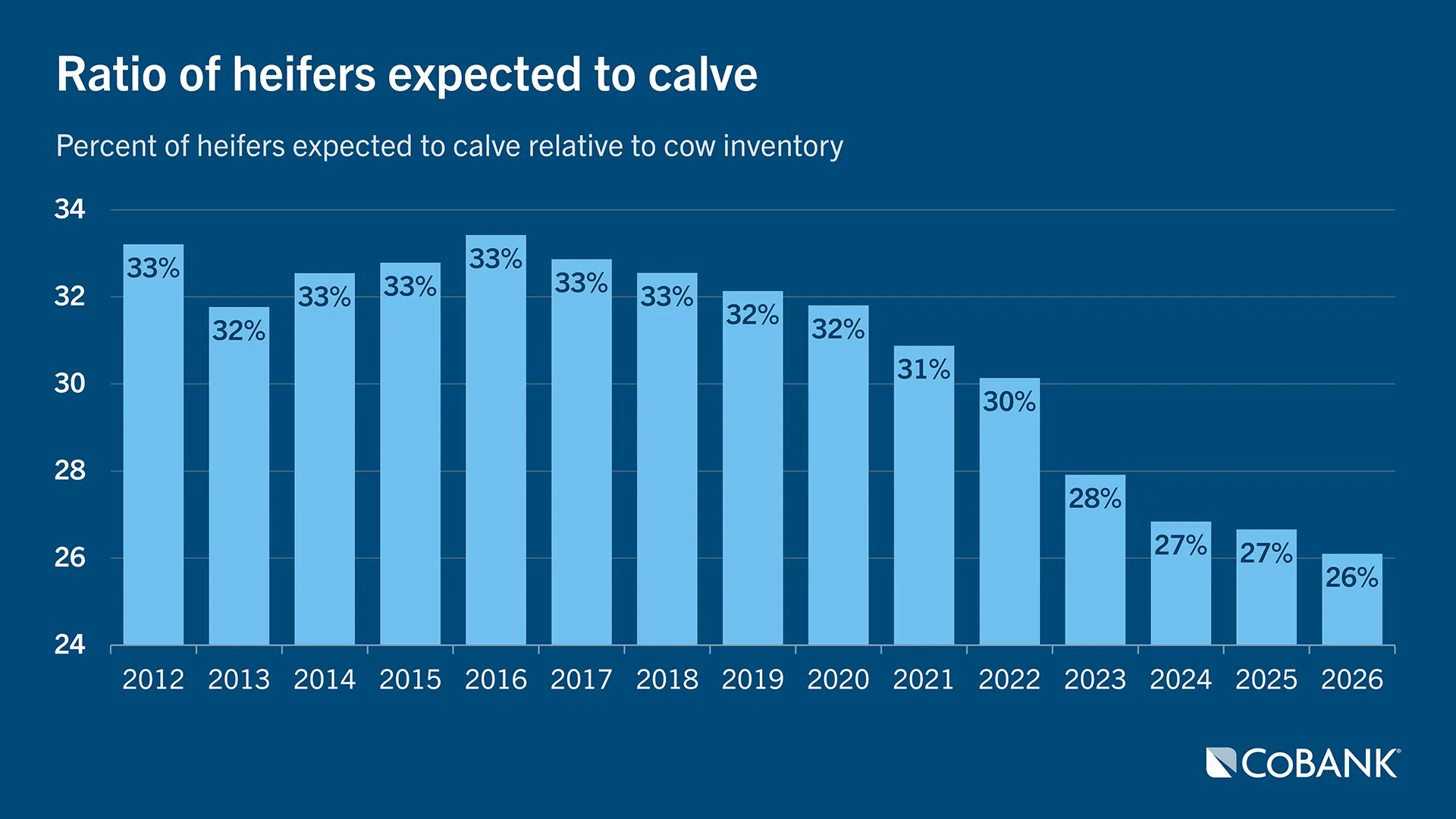

Tight supplies generally lead to higher prices. That is certainly the case for dairy heifers. From 2012 to 2022, the ratio of dairy heifers expected to calve to the dairy cow herd stayed above 30%. It began shrinking in 2023, falling to 27.9% and then tightening further to 26.1% today, based on data from USDA’s January 2026 Cattle report. That decline pushed dairy heifer replacement prices above $3,000 this year, based on USDA’s Agricultural Prices. Those prices are conservative compared to what’s happening in the marketplace. Market prices appear even stronger, with top quality dairy replacements fetching $3,400 to $4,400 in Minnesota and Wisconsin auction markets this spring.

Dairy farmers are retaining dairy cows to offset replacement shortage

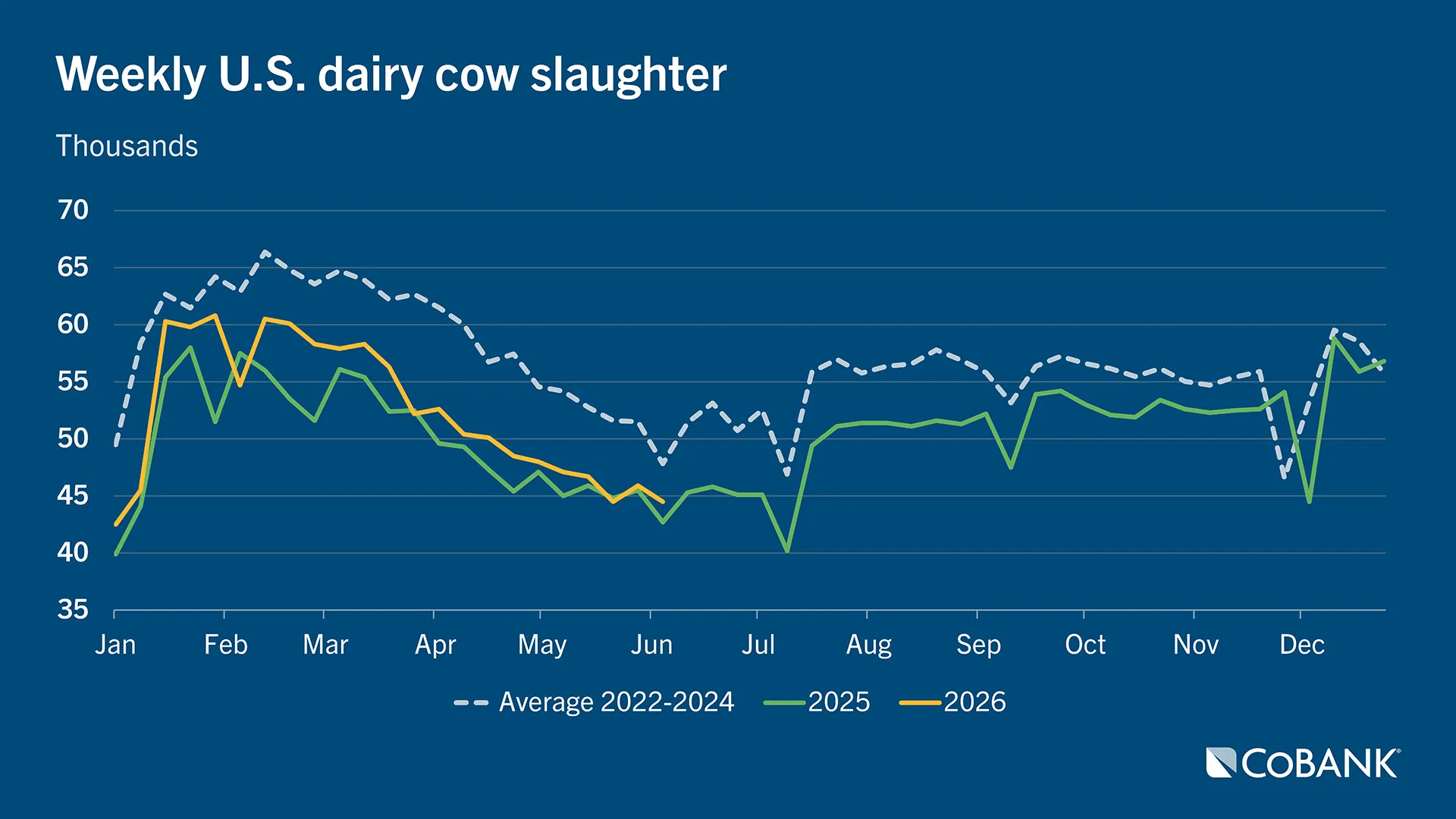

With dairy replacements in short supply, dairy producers across the country responded by sending fewer dairy cows to slaughter. From August 2023 through August 2025, U.S. dairy farmers collectively retained over 600,000 dairy cows based on USDA’s Food Safety Inspection Service slaughter data. Culling has since picked up slightly, with cull cow slaughter increasing 35 of the last 38 weeks from mid-September through mid-June 2026. Even so, this net increase of 83,100 dairy cows sent to slaughter remains far off the 2022 to 2024 pace.

Beef revenue is keeping more dairy cows in the herd

Tight heifer supplies are one reason producers have sent fewer dairy cows to slaughter. Another is the growing value of the cow’s uterus, that is, the cow’s ability to produce a calf for the beef market that is sold shortly after birth. Five years ago, calf and cull cow sales contributed 5% to the dairy farm’s bottom line, versus 95% from milk. Today, beef sales contribute 12% to 15% on many dairy farms with some operations approaching 20% on a per-hundredweight basis. On most dairy farms, the beef check is now driving margins more than the milk check, helping explain why the U.S. dairy herd has grown by 254,000 head since January 2025.

Dairy farmers reallocate semen use, switch to a triple play

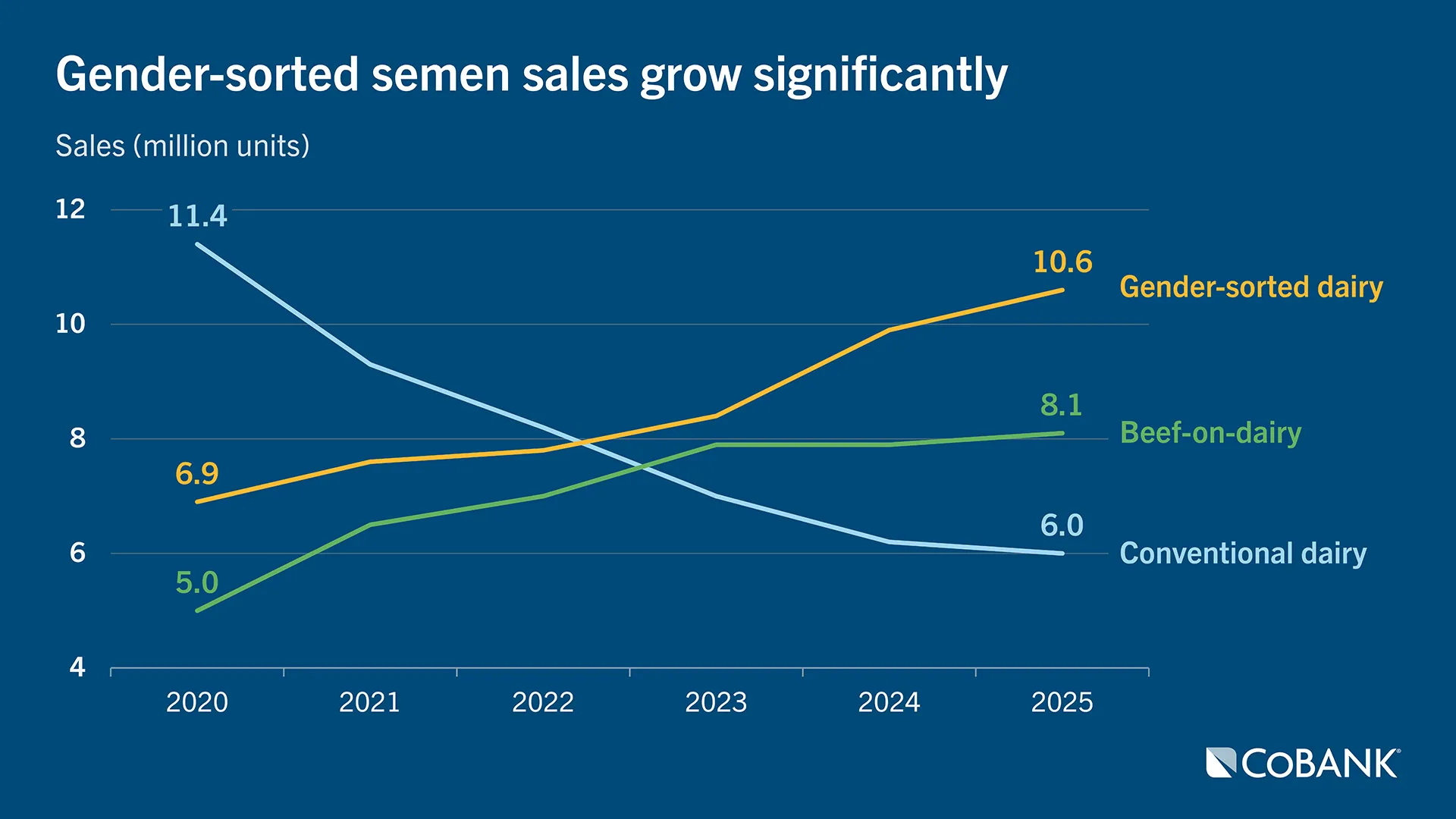

As market dynamics have shifted, many dairy farmers have incorporated portions of a triple play: gender-sorted semen, genomics, and beef-on-dairy. Gender-sorted semen to create future herd replacements from the best dairy heifers and cows; genomic testing to sort out the best dairy heifer calves; and beef semen on the rest of the dairy herd. This has caused a historic shift in U.S. semen sales as dairy farmers purchase two major product categories: gender-sorted dairy semen to produce a dairy replacement heifer and beef semen to produce a beef-on-dairy calf. The long-time standard bearer — conventional dairy semen — is falling out of favor as dairy farmers want to better manage their outcomes and capitalize on higher revenue streams.

Two semen categories are expanding rapidly

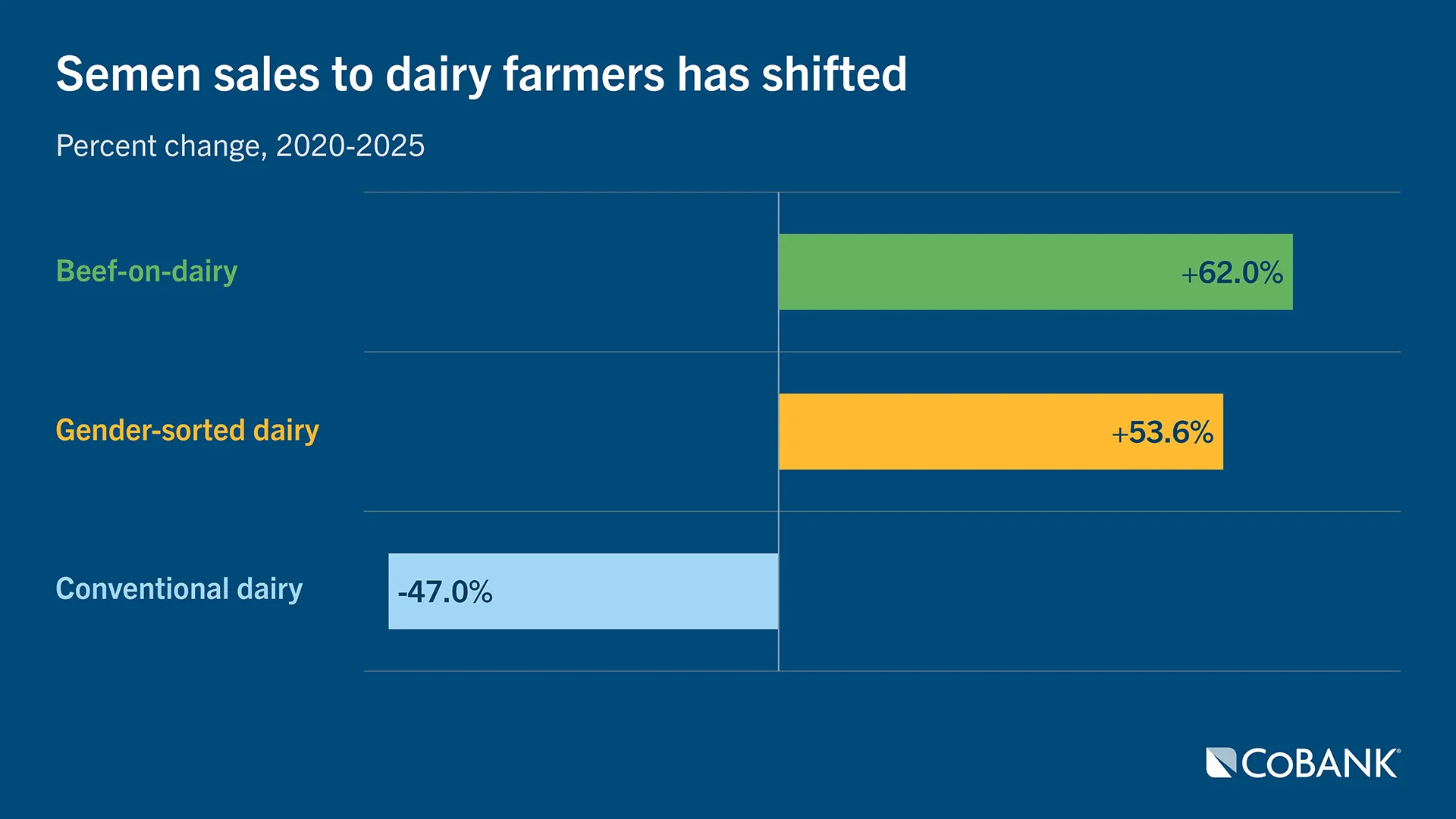

The shift has been both dramatic and significant. Beef-on-dairy semen sales grew a remarkable 62% from 2020 to 2025, while gender-sorted semen sales climbed 53.6% during that same window. On the flip side, conventional dairy semen sales have plummeted over those five years, falling by 47.4% from 11.4 million to 6.0 million units.

Beef-on-dairy semen sales initially set the pace by growing at the fastest clip between 2020 to 2023. Since then, gender-sorted semen sales outpaced that growth as markets couldn’t find replacement heifers. Over this entire five-year period, conventional dairy semen sales fell most dramatically from 2020 to 2021 and have since contracted at a more reasonable pace.

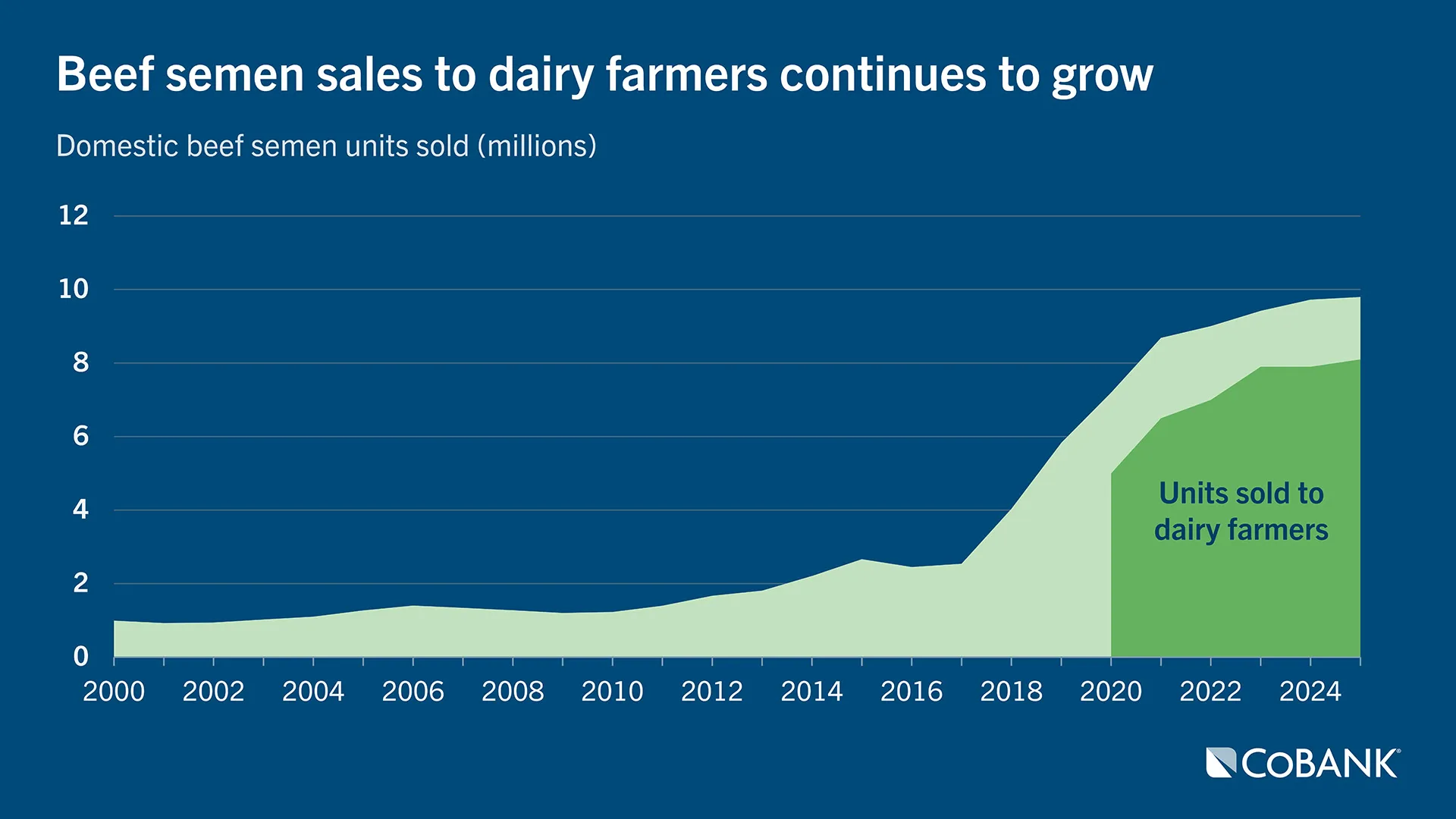

Dairy producers now purchase the super majority of beef semen

When it comes to adopting technology, dairy has an edge over the beef cattle sector. This includes both on-farm data collection systems and using genetics via semen collected from native beef bulls at artificial insemination companies. In theory, some of the nation’s best beef bulls are collected for artificial insemination. For certain, a bull collected for artificial insemination can yield more offspring than via natural service.

In 2020, NAAB began tracking beef semen sales to both cattle ranchers and dairy farmers. That year, U.S. dairy farmers purchased 69.4% of the 7.2 million units of beef semen sold in the U.S. By 2025, the dairy purchasing share climbed to 82.7% of the 9.8 million units sold.

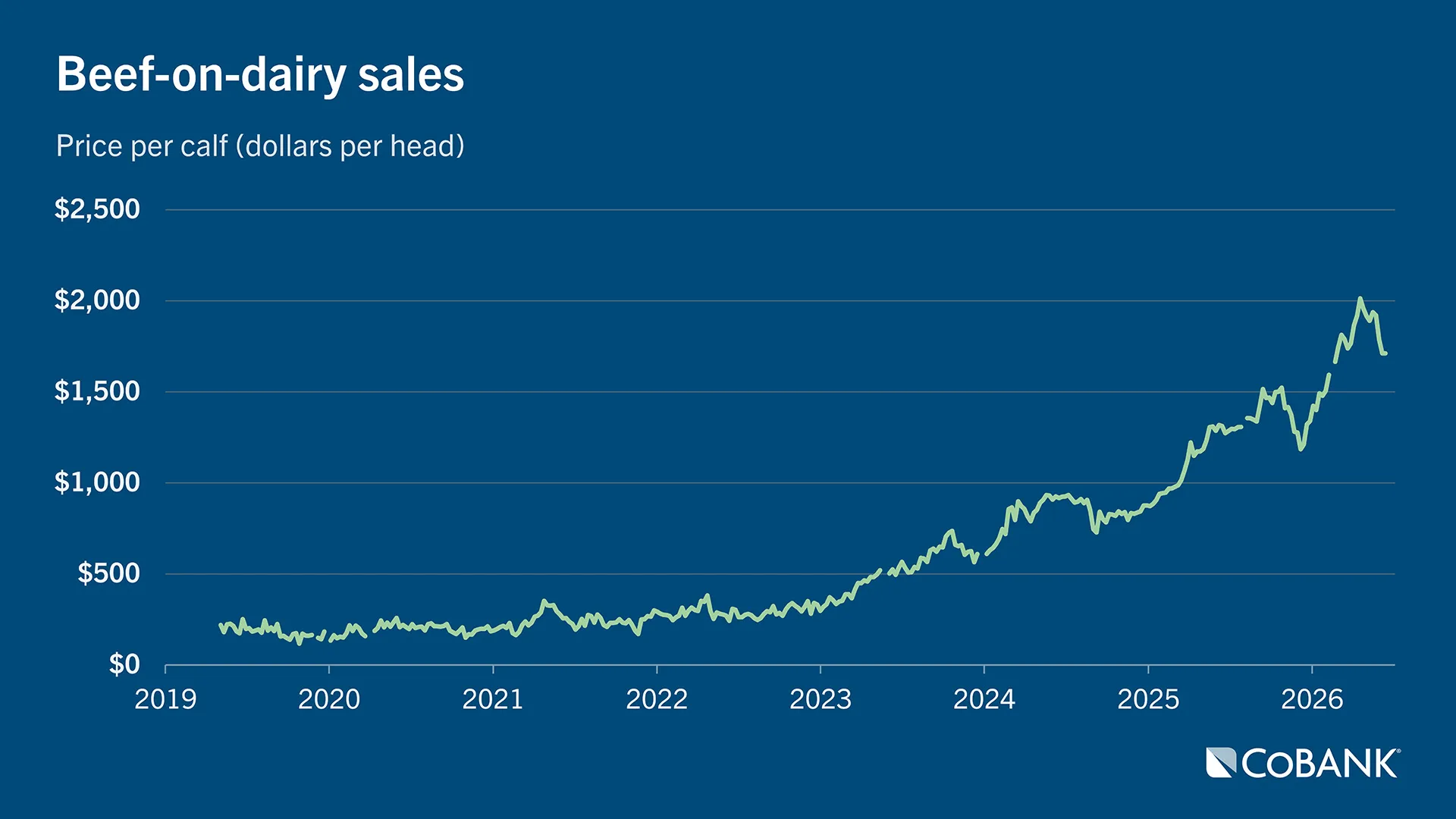

Calf prices continue to climb with tight beef supplies

Dairy continues to play an important role in the beef market as roughly 1 in 5 pounds of beef come from a dairy cow either via the dairy cow herself at slaughter or her calf entering the supply chain. With beef cattle inventories at a 75-year low and strong consumer demand for beef, crossbred beef-on-dairy calf prices have followed the record-high trend of the beef cattle market. For example, beef-on-dairy calves tracked via the Lancaster, Pennsylvania, auction has moved from $1,400 in January 2026 to nearly $2,000 by May. This trend will continue to encourage dairy farmers to maximize beef revenue and may cause beef semen sales to push higher this calendar year.

Replacement numbers should begin rebounding in 2027

The strong growth in beef semen sales to dairy farmers in 2023 will suppress dairy replacement inventories this year due to the three-year biological cycle from conception to becoming an adult dairy cow. It’s expected there will be 438,800 fewer heifers entering dairy herds this year, based on the CoBank model highlighted in our report last year.

That trend will begin to reverse in 2027 with 285,400 dairy replacements projected to enter the milking herd. Triggering the reversal is 1.5 million additional units of gender-sorted dairy semen sold to U.S. dairy farmers during the 2024 calendar year. This uptick in replacements should continue in 2028 with 74,900 more heifers being available to become dairy cows resulting from 700,000 additional units of gender-sorted semen sold in 2025. While that represents significant growth in units, those gender-sorted sales are muted by 200,000 more units of beef semen sold to dairy farmers in the most recent calendar year and only a 200,000-unit reduction of conventional dairy semen.

It’s important to keep in mind that these are forecasts based on national averages of conception rates, pregnancy loss, birth rates, and completion rates, which will vary from region to region as outlined in our model last year. In addition, replacement prices will vary based on dairy plant investments. New York, Texas, Wisconsin, Michigan, Idaho and the I-29 corridor area including western Iowa, western Minnesota, and South Dakota top the list for the $13 billion in new dairy processing investments. This demand for milk will cause dairy replacement demand to be higher in these regions.

The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.