What’s replacing alcoholic beverages?

Key points

- Alcohol consumption is declining globally, driven by younger consumers focused on their health and wallets. As such, world-wide wine consumption in 2024 hit its lowest level since 1961.

- Non-alcoholic beverage sales are booming. Innovation is driving the category with new products offering unique sensory experiences rather than simply mimicking alcoholic drinks.

- Consumption of cannabis has surpassed alcohol, and cannabis-infused beverages are emerging. More than a quarter of consumers plan to try a cannabis beverage, though price remains a barrier.

- The adult beverage industry – in both the alcoholic and non-alcoholic beverage segments – faces headwinds from tariffs and potential bans on artificial ingredients.

More than 4 out of 10 (41%) of U.S. consumers are working to moderate their alcohol consumption, with Gen Z and Millennials at the forefront. Gen Z consumes roughly 20% less alcohol than even Millennials on average, according to International Wine & Spirits Record data. “Dry January” has grown increasingly popular as consumers recover from New Year’s and the holidays by eliminating alcohol, which may be as much an ambition to recover economically as to avoid alcohol. For that matter, recent Januaries have seen notable declines in restaurant foot traffic, again pointing to pocketbook recovery as a potential benefit for consumers to go “dry.”

This recent reduction in alcohol consumption reflects a 23-year period of attrition, but consumers are not eliminating alcohol entirely. NielsenIQ’s 2023 Non-Alcohol Report found 94% of non-alcoholic beverage buyers continued to purchase alcoholic beverages in addition to non-alcoholic alternatives, suggesting consumers are adopting more of a flexitarian type of approach to drinking alcohol. To put the trend in Gen Z parlance: “zebra striping” is a slang term that denotes an evening spent alternating between alcoholic and non-alcoholic drinks, effectively reducing the alcohol consumption, if not the cost, by half.

The shift from alcohol is a global phenomenon

The reduction in alcohol consumption is far from confined to the U.S. Wine consumption globally in 2024 hit its lowest level since 1961, per the International Organisation of Vine and Wine (OIV). The OIV pointed to high prices and lower demand in major markets for the global decline, with prices remaining up due to low production volumes and lingering inflation effects.

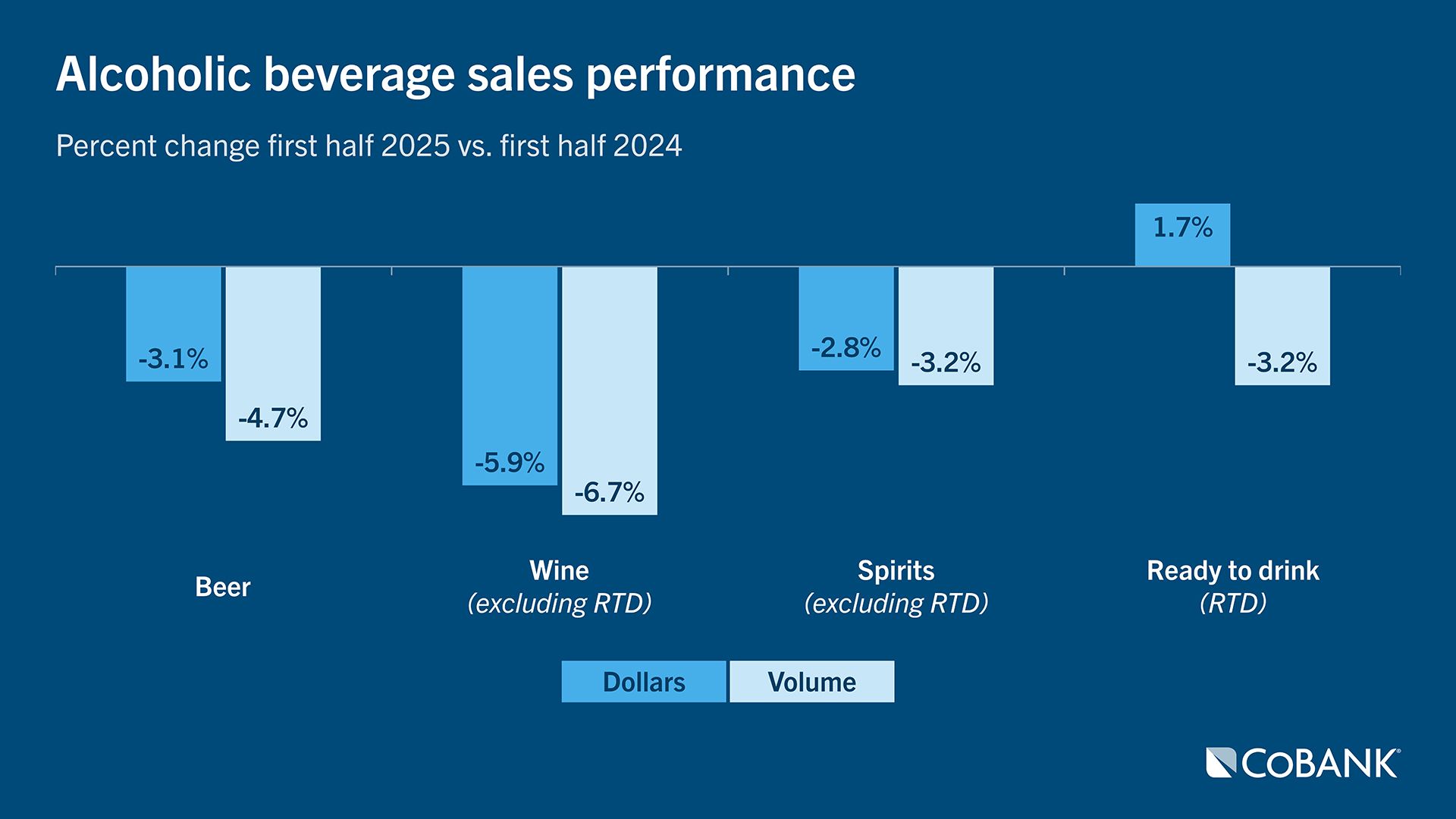

In the U.S. alone, wine consumption fell by 5.8% in 2024 and sales are not doing much better. Total U.S. wine sales were down 2.2% (-4.3% in volume terms) compared with the prior year for the 52 weeks ending Dec. 29, 2024, per Circana. Sales of spirits and beer are down as well. In the first half of 2025, total alcohol beverage sales were down 3% YoY, according to NielsenIQ’s “The Halftime Report,” with volume declines across the major segments. Dollar sales increased in only one category: ready-to-drink, the category of pre-mixed alcohol beverages packaged for convenience. The report notes that performance in the spirits segment faces challenges from RTD’s growth, yet in all alcohol segments volume sales have continued to erode. Beverage companies are facing those same headwinds in the second half of 2025, particularly with consumers shifting toward moderation, value and wellness.

Younger generations drive the teetotalling shift

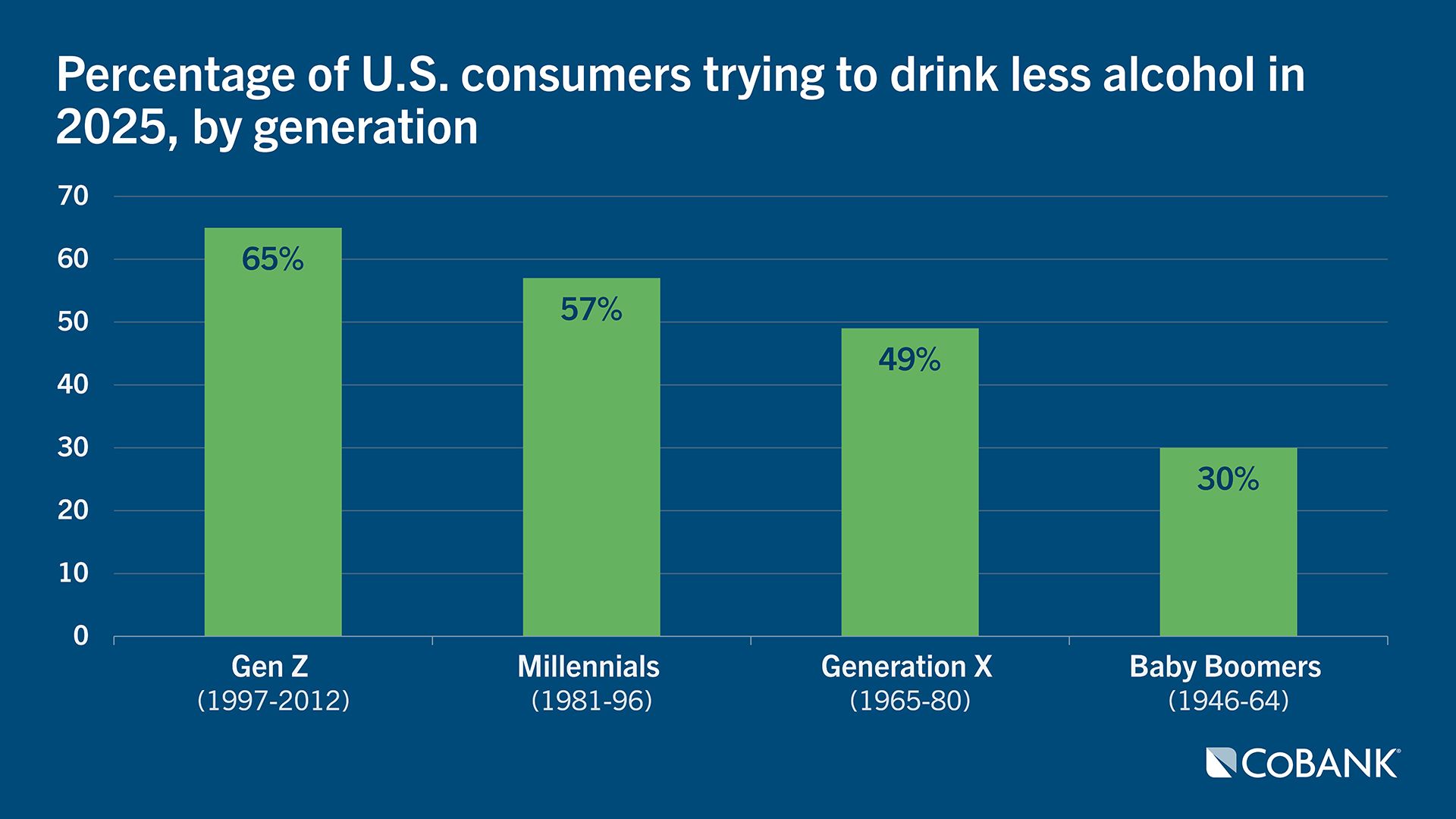

Nearly half of Americans are trying to drink less alcohol in 2025, a number markedly higher among younger generations, per NCSolutions. In just the last two years, the level of interest in sober-curious lifestyles has increased 44%, and fully a quarter of American adults report drinking no alcohol in 2024.

Avoiding mood-altering beverages does not seem to be consumers’ main motivation for curtailing their alcohol use. Instead, consumers appear much more motivated by economic and health reasons. The reasons respondents gave NCSolutions for drinking less alcohol:

- 62% to improve their physical health.

- 55% to save money.

- 42% to improve their mental health (58% of Gen Z).

- 36% to lose weight (48% of Baby Boomers).

- 35% see alcohol as a treat or luxury.

- 20% say drinking alcohol is a habit they can no longer afford.

Nearly 6 in 10 of all consumers (58%) plan to try non-alcoholic wine, beer or spirits in 2025. And while their reasonings may vary, the trend toward non-alcoholic beverages is not only gathering steam but significant investment. Non-alcoholic beer purchases increased 22% in alcohol-buying households from December 2023-November 2024, compared to the same period in 2022-23, per Circana data.

Virtually all alcohol beverage categories have seen competitors enter the market offering low-alcohol or non-alcoholic beverages, with beer alternatives proving most successful. In fact, while the market size of non-alcoholic wine may pale in comparison to other adult beverages, it registered 41% YoY dollar sales growth in 2024, per Beverage Industry.

Targeting alcoholic flavor without alcohol

Early non-alcoholic offerings in the mid-2010s tended to feature tea, botanicals or flavored distilled water and as might be expected, ultimately resulted in products more similar to herbal soda or sweetened water than to their alcohol-based raison d’etre. The trend toward non-alcoholic beverages and rapid growth in sales prompted considerable innovation in the space. In the process, producers — particularly in the consumer-packaged goods space – are introducing options that offer novel sensory experiences that can stand on their own, rather than simply mirroring alcohol-based counterparts. As a result, newer non-alcoholic ready-to-drink beverages tend to push the boundaries in terms of flavor and even viscosity, which are resonating with consumers.

As a consequence, the market has seen a range of brands emerge solely dedicated to non-alcoholic offerings, as well as beverage makers the world over leveraging familiar brands in the relatively new low-/non-alcohol space:

- Asahi expects fully a fifth of its group-wide portfolio will be comprised of low-/non-alcoholic products within six years. As of the first half of 2024, low- and no-alcohol products (i.e., with 3.5% or less alcohol by volume) accounted for 12.1% of Asahi’s total sales. Its investment strategy indicates confidence in the continued strength of the trend in the U.S. The company’s venture capital arm Asahi Group Beverages and Innovation contributed to a Series A funding round for non-alcoholic drinks retailer The Zero Proof in January of last year.

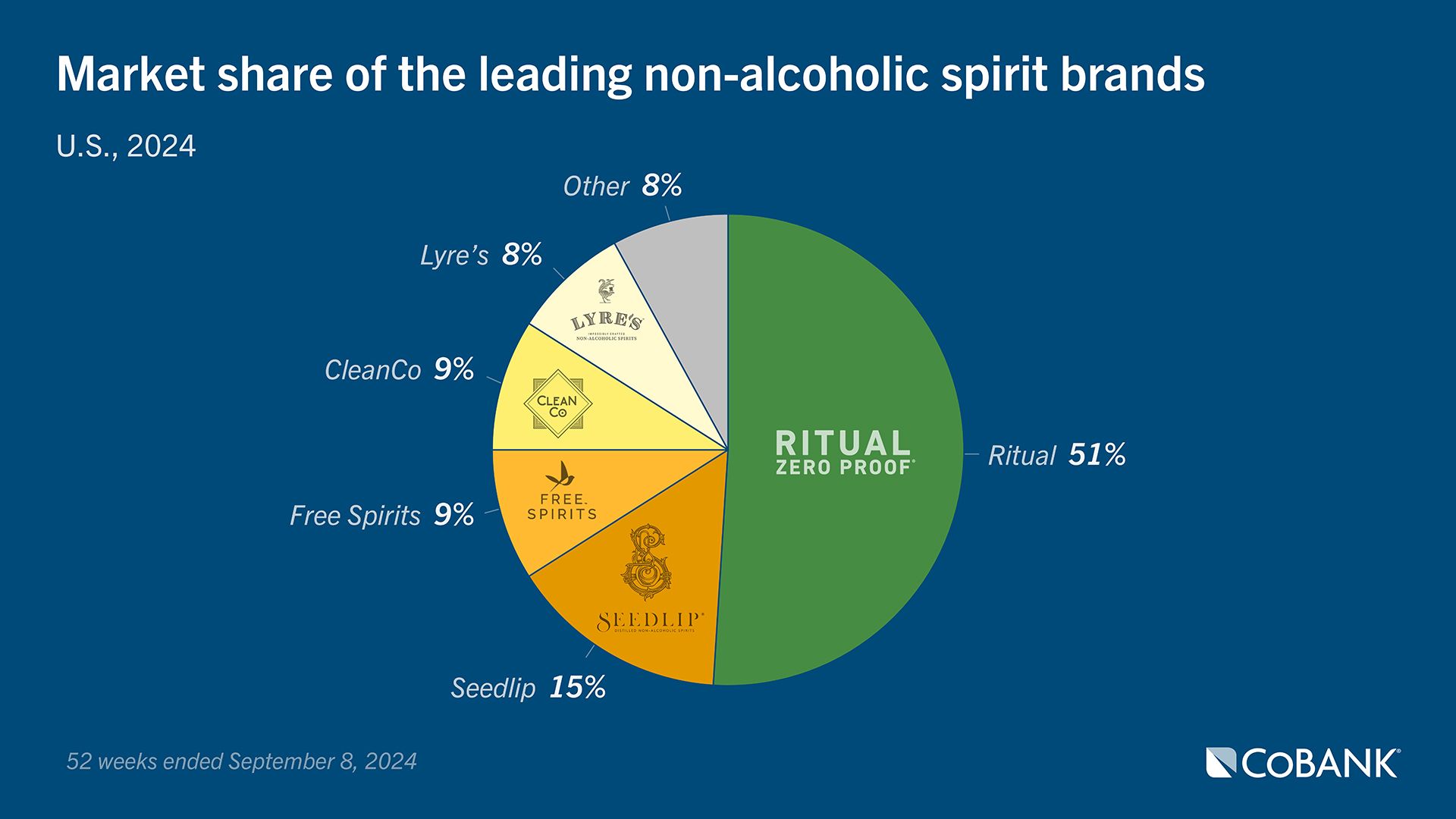

- Diageo has invested significantly into its non-alcoholic brand extensions – from zero-alcohol Captain Morgan’s and Tanqueray to Guinness 0.0. The company is investing €25 million to boost production capacity for the non-alcoholic variant of its Guinness Stout in Dublin, Ireland, and plans to build a two-story facility with six processing vessels and a total capacity of 500,000 hectoliters. In the spirits space, the company acquired U.S.-based Ritual Zero Proof, which has a portfolio of five non-alcoholic options in tequila, gin, rum and whiskey alternatives.

- Pernod Ricard has long had non-alcoholic versions of established brands, dating back to 1982. More recently, it acquired Swedish Ceder’s botanicals-based spirit line, Jacob’s Creek Unvined wine and the Suze Tonic 0% beverage exclusive to the French market. Pernod Ricard has also invested in agave-based and RTD spirits alternatives.

- Anheuser-Busch InBev (AB InBev) has increased the number of low-alcohol and non-alcoholic products in its portfolio by 60% (and volumes by 23%) since 2019. In an indication of just how prominent the non-alcoholic beverage trend is expected to be, the company’s non-alcoholic Corona Cero will be the global beer sponsor for the Olympic Games through 2028, which is ironically the Olympic Committee’s first sponsorship with an alcohol brand.

- Molson Coors plans to “scale and expand” its Beyond Beer portfolio, projecting the range will produce “about half of its Above Premium net sales revenue growth over the medium term.”

While the low-/non-alcohol space is claiming new fans, ingredient costs remain a key issue. A non-alcoholic beverage demands the same strict ingredient expectations (quality of ingredients and a flavor complexity) as well as production techniques that can replicate the depth and texture that alcohol imparts on its own. Many consumers figure that the price for a non-alcoholic beverage should be less than their alcohol-containing counterpart. The reality is that the alcohol itself is often one of the least-expensive components of a drink.

Alcohol out, cannabis in

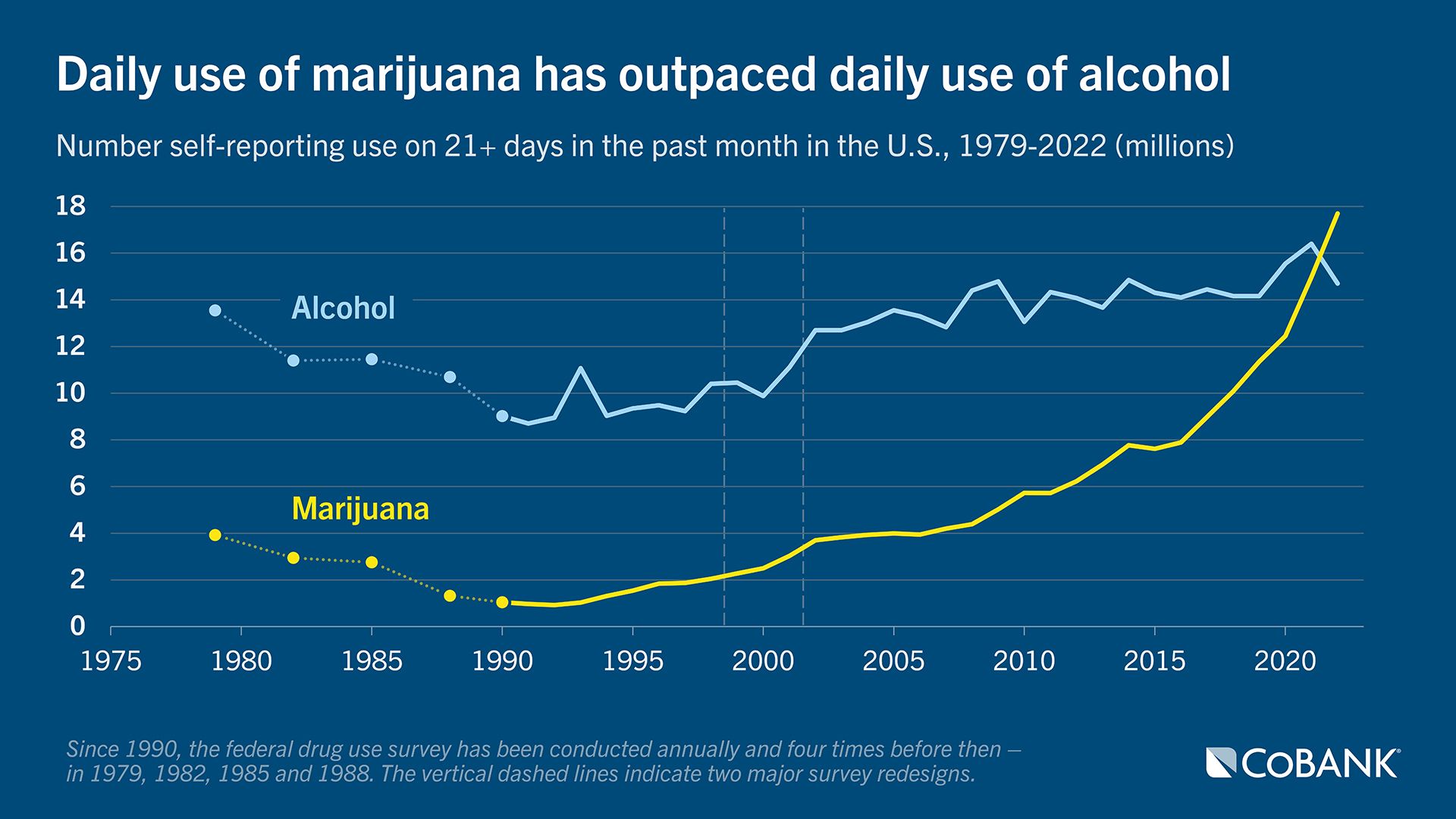

While alcohol use has waned, cannabis consumption is on the rise. A 2022 study found 17.7 million people reported daily or near-daily marijuana use; comparatively, 14.7 million people reported drinking at the same frequency.

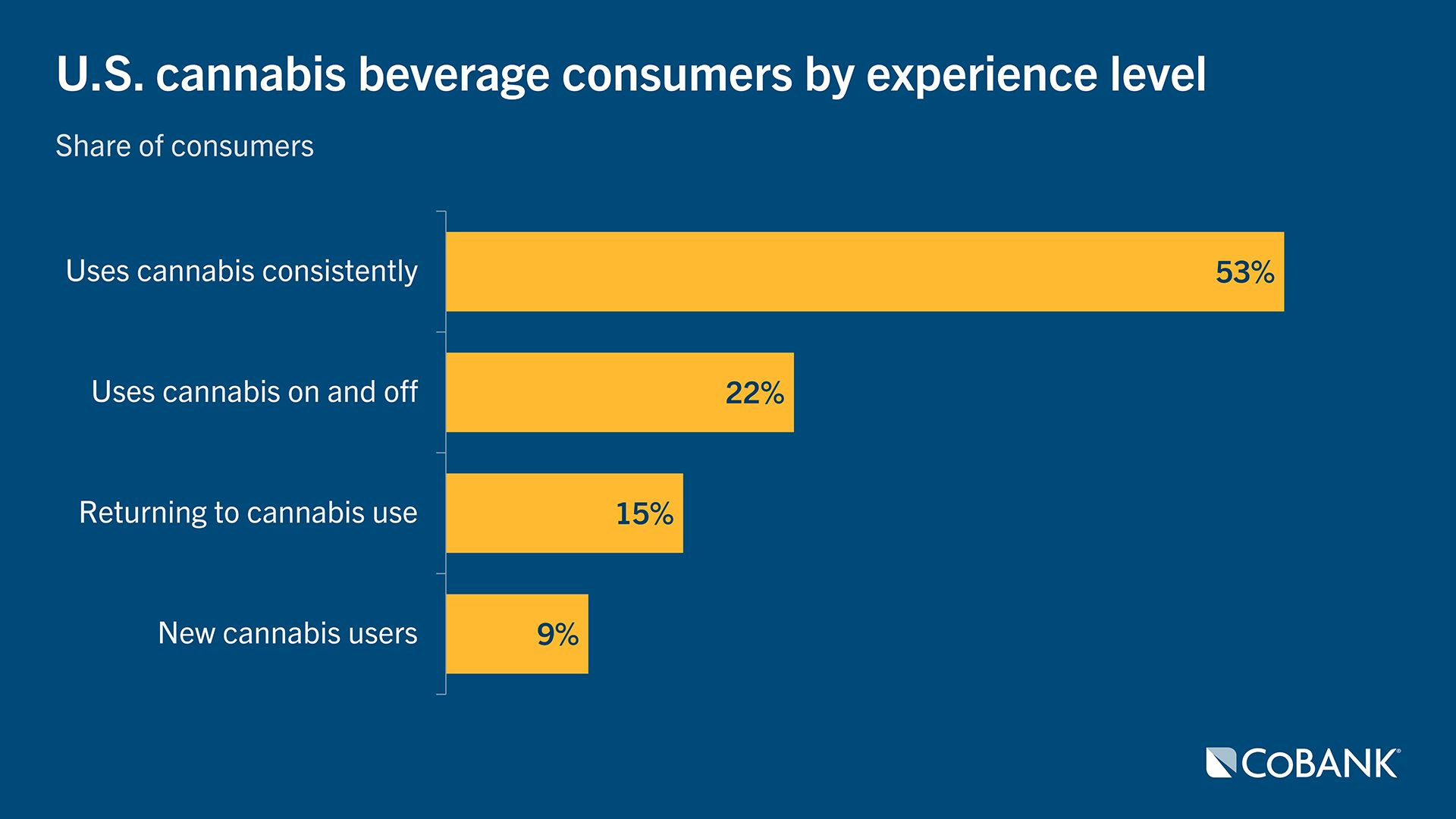

Bear in mind, cannabis is legal for recreational use in only 24 states (and 40 for medical use). The decline in alcohol drinkers is partly due to consumers choosing to live an alcohol-free lifestyle, but consumers now have another option: access to legal cannabis, including cannabis-infused beverages. In fact, a quarter of all consumers (26%) plan to try a cannabis beverage (THC or CBD infused), an interest strongest among younger generations – 38% of Gen Z, 37% of Millennials. The interest in trying these beverages faces a bit of headwind as their usage strongly correlates to consistent cannabis use. Not that it would be impossible for the category to introduce new consumers to cannabis, but at present, cannabis beverages appear directed at those already familiar with cannabis.

The market shows significant potential. Projections indicate U.S. sales of cannabis beverages will reach $2.8 billion by 2028. That remains a fairly small competitor to the U.S. market for alcoholic beverages ($309 billion in 2025, two thirds of which is sold at the retail level). However, their growth rates differ considerably: cannabis beverages have a projected compound annual growth rate (CAGR) of 16.9% through 2028; at-home alcoholic beverages are expected to have a CAGR of 2.4% through 2030, but largely due to price increases. In volume terms, alcoholic beverages have declined across virtually all segments for the past two years.

A bigger challenge for cannabis drinks is the typically higher price point. Brands in the cannabis drink space attempt to counter price concerns by noting the value of convenience, variety of flavors and by prioritizing wellness and social elements, not to mention their lack of hangover effects. The drivers for cannabis drinks vary considerably by generation. Millennials and Gen Z have led the trend, citing the options as a lower-calorie and “more-natural” alternative to alcohol, as well as the ability to consume cannabis in a format such as a seltzer or tonic. For older consumers seeking relaxation or a medical benefit from cannabis, drinking an infused beverage is an appealing alternative to smoking marijuana.

At present, cannabis beverages remain a small but growing niche of the adult beverage market. Its potential is strongly driven by not only a consumer desire to unwind – a product benefit that has long boosted alcoholic beverages – but also health and wellness trends. Product benefits range from relaxation to stress relief to enhanced sleep and even fitness recovery. Continued growth will be boosted by further advancements in flavor varieties and different dosage formulations that can attract more mainstream users, ultimately with the potential to position the products as a component of both wellness and recreational consumer trends.

Headwinds from potential tariffs and artificial bans

As with most beverages, adult drinks particularly in the RTD space are exposed to potential crackdowns on artificial ingredients, including colors, flavors or sweeteners. For non-alcoholic offerings marketed as a healthier alternative, the fallout from such bans could be profound, but companies are developing solutions. These include colorings drawing from a host of plant-based solutions, including reds from radish, sweet potato and black currant; yellows from turmeric, safflower and pumpkin; blues from spirulina; and orange from paprika and annatto. Similarly, natural solutions are available for flavor and sweetening, though the latter face somewhat negative healthy perceptions of their own, not to mention significant exposure to tariff policy.

Tariffs – both realized and potential – pose a distinct challenge, even to the few segments of alcoholic beverages that have proven relatively resilient among the onslaught of non-alcoholic competition. The 25% tariffs, which were initially set for February 2025 and briefly implemented in March before being abruptly put on hold, have negatively impacted the tequila sector, leading to reduced sales and increased operational costs. Producers and consumers have stockpiled tequila to mitigate potential tariff impacts, incurring significant costs in storage and production. These costs could lead to price increases regardless of whether tariffs are enacted. Storage fees alone are expected to add up to 10% to costs, which will be incurred now regardless of tariff implementation. The potential negative consequences from tariffs could lead to significant challenges for tequila, which has heretofore been a strong performer, one of the few bright spots, in the spirits market in the U.S.

Similarly, reported potential tariffs of 15%-20% on imports from the EU risks potential reciprocal tariffs on American exports of wine, beer and whiskey. Considering the bloc is the largest importer of U.S. spirits, the consequences – for alcoholic or non-alcoholic brands – could be considerable.

Conclusion

Non-alcoholic wine, beer and spirits have proven to be one of the more-resilient segments of the beverage industry, with growth even as sales slip for their alcohol-based brethren. The alcohol industry is living the trend and investing heavily in non-alcoholic adult beverages. With younger generations looking for a wider variety of adult beverages, alcoholic drinks will continue to fight for share not only with non-alcoholic iterations of familiar bar favorites, but also with an increasing array of cannabis-infused beverages and similar products to come, including potentially in smaller formats such as shots that may help offset some of their price shock, while still delivering on a relaxing drink experience.

Information contained in this report from Circana and its affiliates is the proprietary and confidential property of Circana and was made available for publication herein by way of limited license from Circana. Circana data may not be republished in any manner, in whole or in part, without the express written consent of Circana.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.