Grain logistics outlook: Record crop meets trade uncertainty

Key points

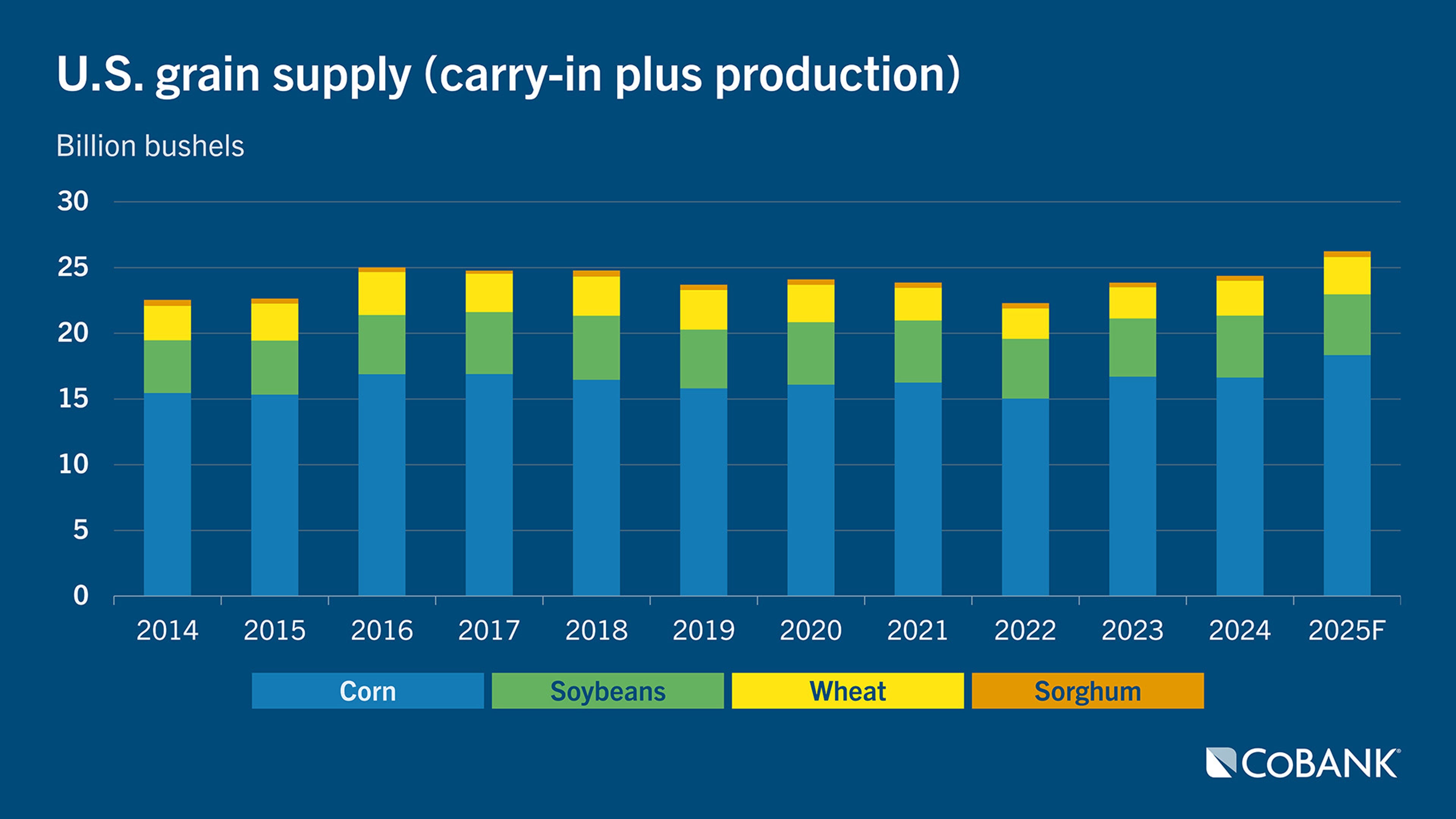

- The U.S. is bracing for a record fall harvest this year totaling 21.5 billion bushels of corn, soybeans and grain sorghum – up 10% YoY and a new record on the heels of the largest wheat harvest in five years.

- Storage will be tight with grain merchandisers charging higher storage fees on scarce capacity and strained infrastructure. Grain elevators, though, will benefit from capturing wider carries in the futures markets while buying cheaper basis.

- Geopolitical uncertainty has weakened export programs for soybeans and grain sorghum, opening elevation capacity for corn and wheat, which have stronger programs.

- Lack of railroad cars to the Pacific Northwest and low water levels on the Mississippi River will constrain shipments, but ample rail car availability to Mexico and other destinations will support exports.

- The risk to elevators is farmers not selling, or opting for delayed pricing programs. Potential market rallies may also cause steep margin calls on heavy short-positions for company-owned grain.

Record fall harvest

The U.S. is expected to harvest a record fall crop of 21.5 billion bushels of corn, soybeans and grain sorghum this year – up 10% YoY and a new record – on the heels of the largest wheat harvest in five years.

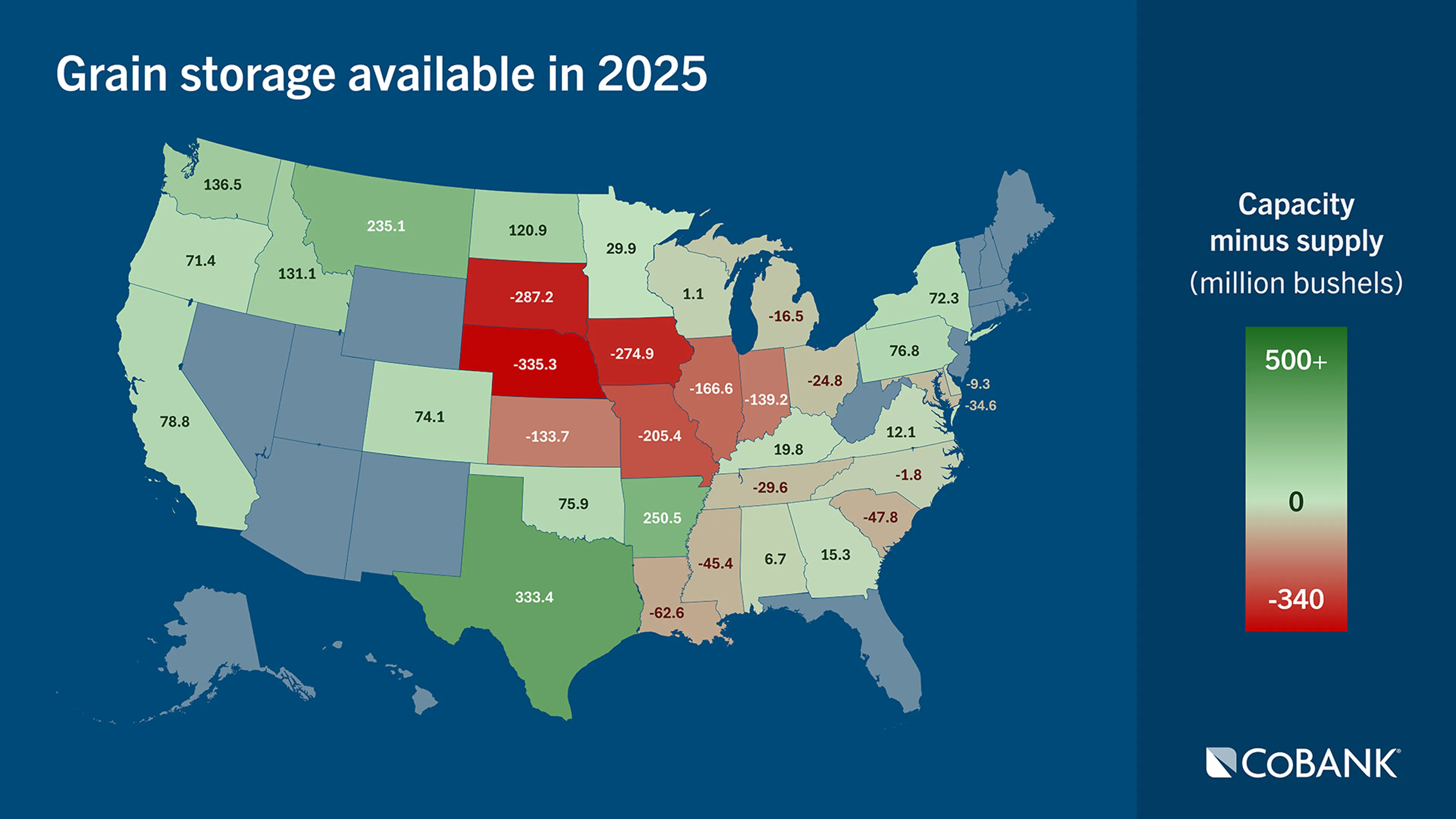

Prioritizing scarce grain storage will be a challenge for elevators. The U.S. is estimated to be short 73 million bushels of upright grain storage this year versus last year’s surplus of 1.8 billion bushels of capacity. Among the top 12 corn-producing states, storage is figured to be short by 1.4 billion bushels versus last year’s surplus of 361 million where elevators will rely more on bunkers and emergency storage like ground piles.

In the absence of Chinese demand, farmers may opt to store more soybeans and grain sorghum on the farm. Some farmers may be forced to haul grain to the elevator if they lack on-farm storage. Some will hold grain in temporary storage like grain bags.

Grain merchandisers will charge higher fees on scarce storage capacity and to cover strained labor and infrastructure to handle the volume. Or they may not accept delivery of commodities like soybeans and grain sorghum that currently lack a strong export market.

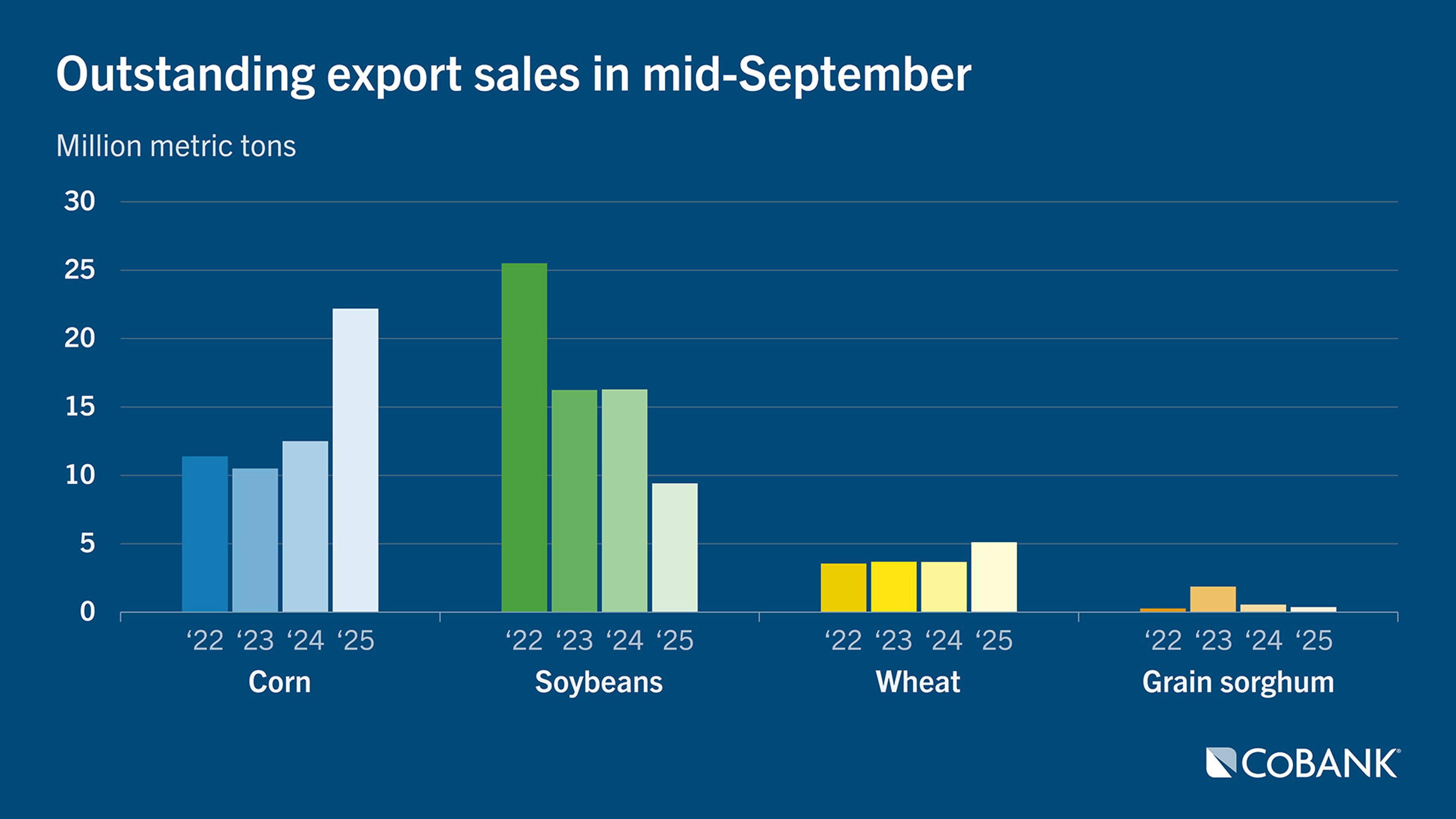

Outstanding export sales

The export program for both corn and wheat is heading into the fall with historically strong sales, aided by cheap prices, a weakening dollar, and favorable transportation costs. And, neither crop has been affected by the trade war between the U.S. and China. Outstanding corn sales are up 94% YoY while unshipped all-wheat sales are up 41% YoY.

Soybean and grain sorghum export sales are lagging well behind prior years due to the lack of Chinese demand while non-Chinese destinations are not picking up the slack. Soybean sales are down 51% YoY while grain sorghum sales are starting the season down 58% YoY.

The slow pace of soybean and grain sorghum exports may benefit corn and wheat. The weak shipping pace of soybeans and grain sorghum will allow more transportation and elevation capacity to be used to support corn and wheat shipments to the Pacific Northwest (PNW) and to the U.S. Gulf.

Elevators that are struggling with tight storage may prioritize corn and wheat over soybeans and grain sorghum due to the lower risk of corn and wheat, which have more reliable export flows.

Rail car capacity and rates

During peak harvest, railroad companies have planned for a general increase in grain rail capacity for the West/Central U.S., according to USDA-AMS. However, railroads plan to decrease rail capacity in the East, as its larger grain harvest this fall means end users are importing less grain from the Central U.S.

Rail rate reductions are helping to spur demand for U.S. commodities, specifically corn and wheat to Mexico and the Gulf. However, the lack of an export bid for soybeans in the PNW has caused railroad companies to run a limited program to the PNW region and to focus on corn and wheat shipments.

Railroads are reallocating cars to other regions of the country, specifically to feed the strong export program into Mexico with cheaper rail rates incentivizing corn, wheat and soybean shipments. Roughly two-thirds of Mexico’s imports from the U.S. are overland with one-third over water.

The risk to the rail market lies a U.S.-China trade resolution, which would return soybean export bids to the PNW and cause rail freight rates to suddenly jump.

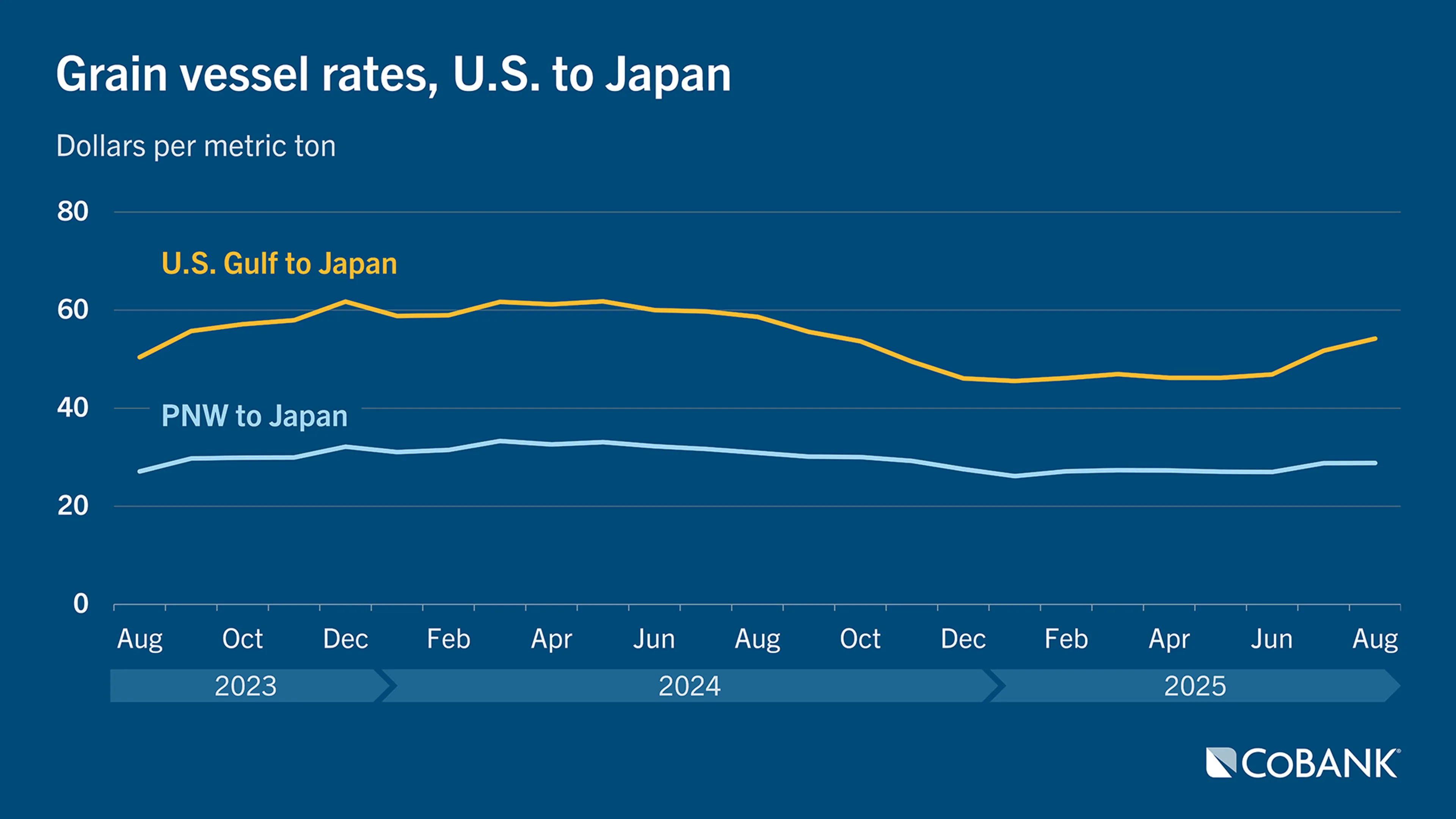

Grain ocean vessel capacity and rates

Bulk carrier ocean vessel rates in the PNW for carrying grain have fallen 6.8% YoY while rates at the U.S. Gulf are down 12.7%, incentivizing U.S. grain and oilseed exports. Rates, though, are climbing ahead of peak shipping season.

Concern over Section 301 fees on Chinese flagged or Chinese-made ocean vessels docking in the U.S. has been muted among grain traders due to exemptions for vessels under a dry weight tonnage of 80,000 tons or vessels arriving empty. The fees on Chinese made and flagged vessels is set to go into effect on Oct. 14.

However, due to political uncertainty and fears they may still be taxed, Chinese vessel owners or operators of Chinese-made vessels are reluctant to send ships to the U.S. The loss of some ships among companies nervous over political uncertainty could potentially affect ocean freight rates during the peak shipping season.

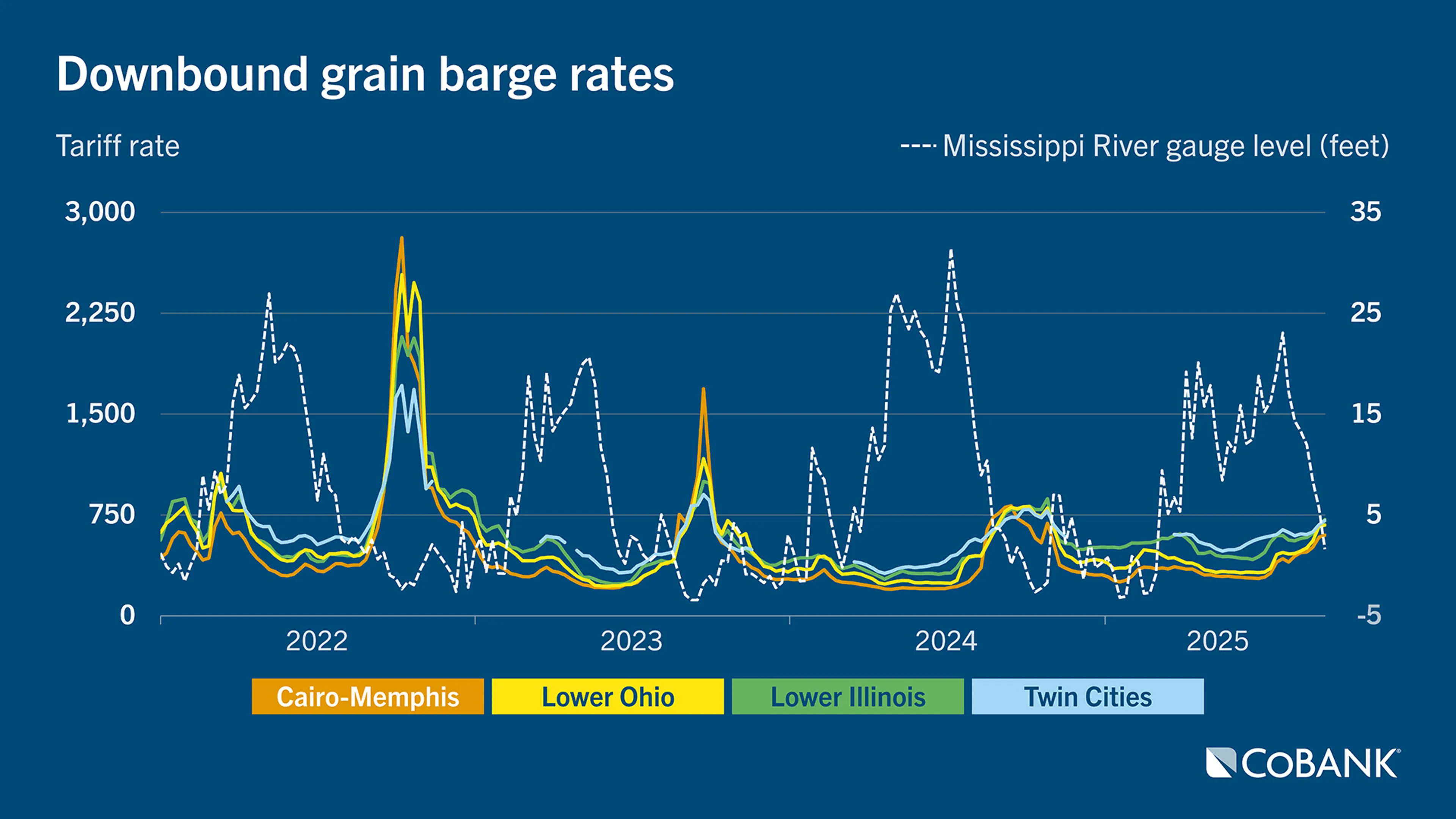

Barge rates

Following a historically dry August in the Ohio River Basin, which contributes about half of the water flow in the lower Mississippi River, water levels on the Mississippi are low. The result is restrictions on draft and tow sizes on the lower Mississippi River and higher rates on downbound barges.

As of Sept. 23, the barge freight rate for shipping grain along the lower Mississippi River was $19.53/ton, according to USDA-AMS. This rate is up 31% from four weeks ago but still 14% lower than the same time last year when extreme dryness had greatly restricted barge movement.

However, below-average soybean shipments down the Mississippi may slow the rise in barge freight rates and allow for larger shipments of corn and wheat. Similar to the rail system, a trade resolution between the U.S. and China may suddenly boost demand for soybean barge freight and lift barge rates.

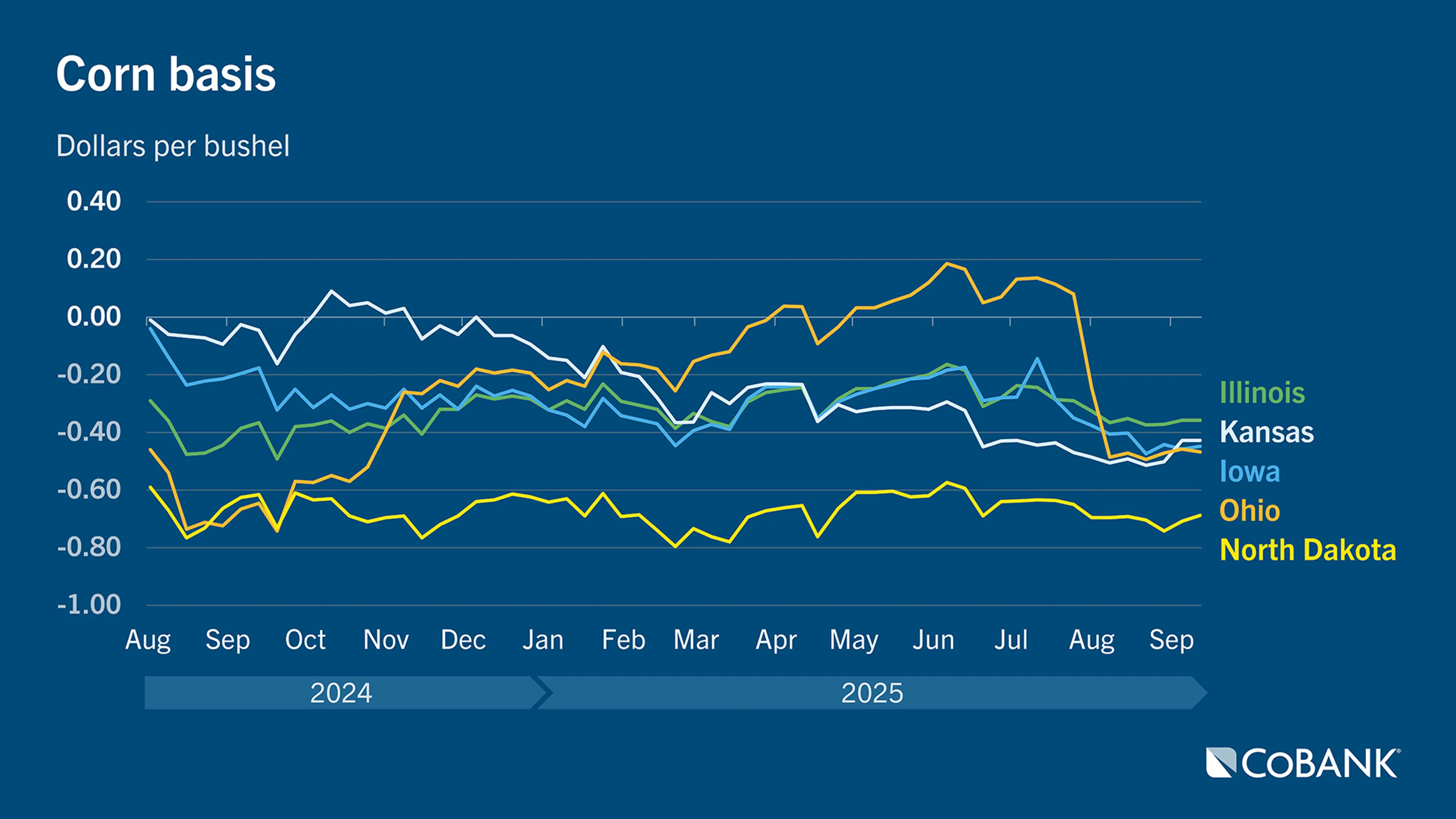

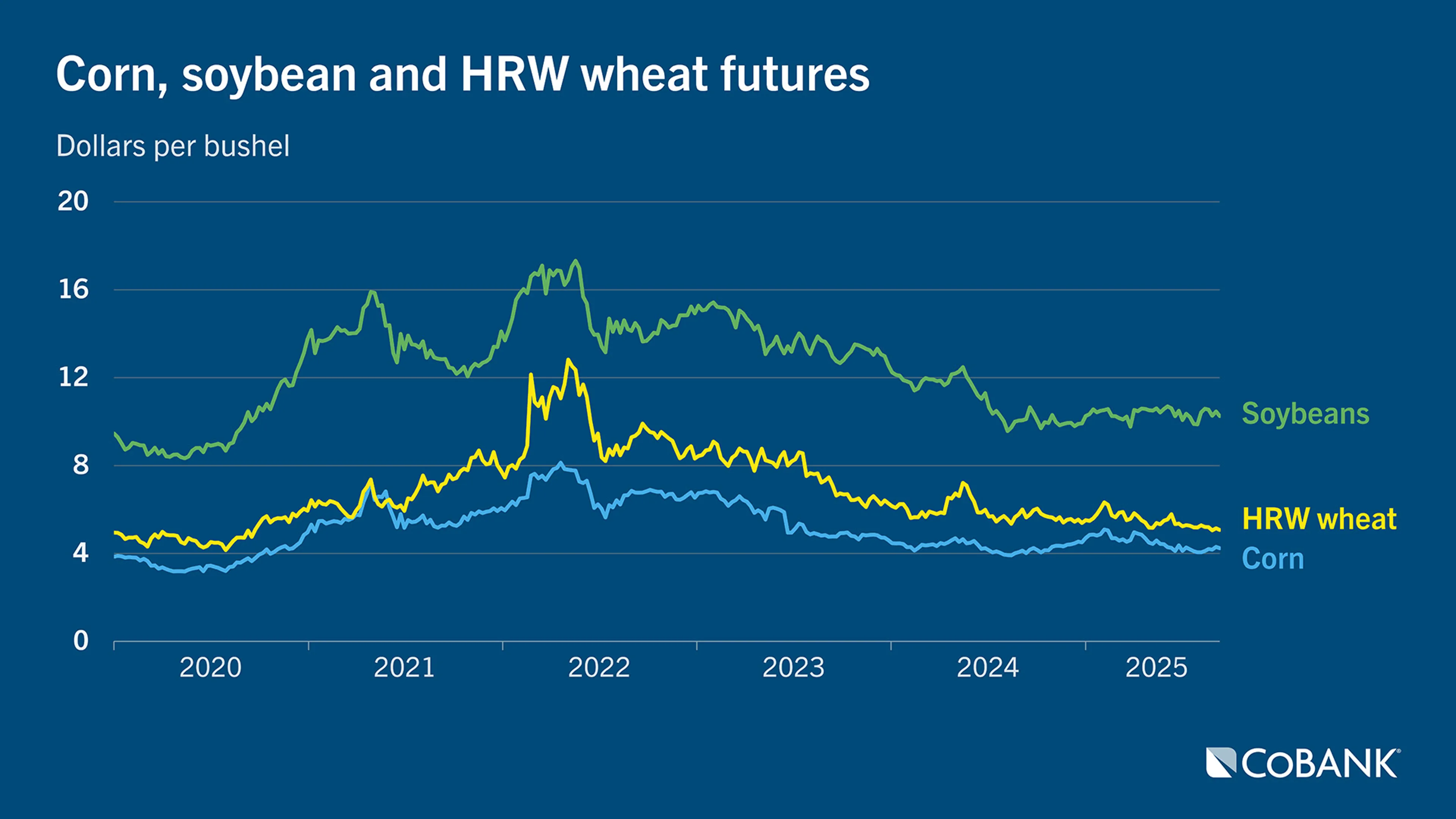

Corn basis

Corn basis levels across the U.S. interior continue to weaken on the prospect of a record harvest this fall with limited storage capacity.

However, deteriorating crop conditions from dryness in the eastern Corn Belt and corn rust disease further west has limited yield potential in some regions, which may result in less tightness in storage capacity.

With the combination of stable domestic demand from ethanol producers and livestock and poultry feeders plus a historically strong export program, elevators feel safe buying and storing corn from farmers.

Elevators will also have more incentive to accept delivery of corn because corn is more easily stored in bunker space and ground piles than soybeans, wheat or grain sorghum and has less risk of shrink from spoilage.

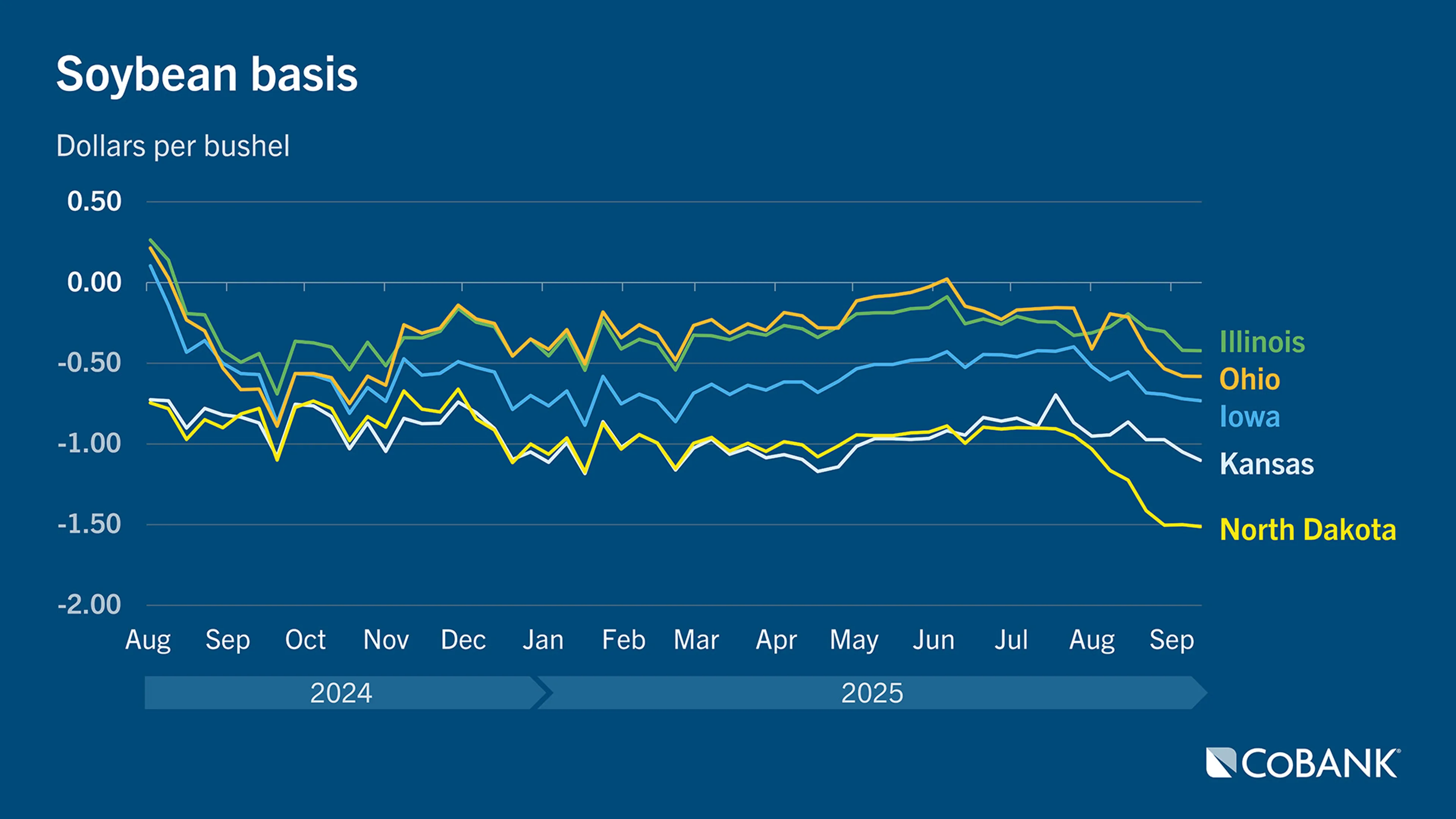

Soybean basis

The loss of Chinese business has weakened export demand for soybeans, dragging soybean basis levels across the U.S. – particularly in the northern Plains that rely heavily on export shipments to the PNW. Crush plants that typically compete with exporter bids are benefitting from lost export competition for soybeans while providing some support to basis in local regions.

Due to the risk of lost export demand, some elevators across the Northern Plains that lack local crush demand may not accept soybeans due to fears of not being able to deliver to the export market later. For elevators willing to take delivery, basis is being set at historically low levels to account for the higher risk.

Weak basis will incentivize farmers to hold soybeans off the market. More farmers will attempt to store soybeans on the farm but may lack experience in handling soybeans, which may result in quality degradation over time.

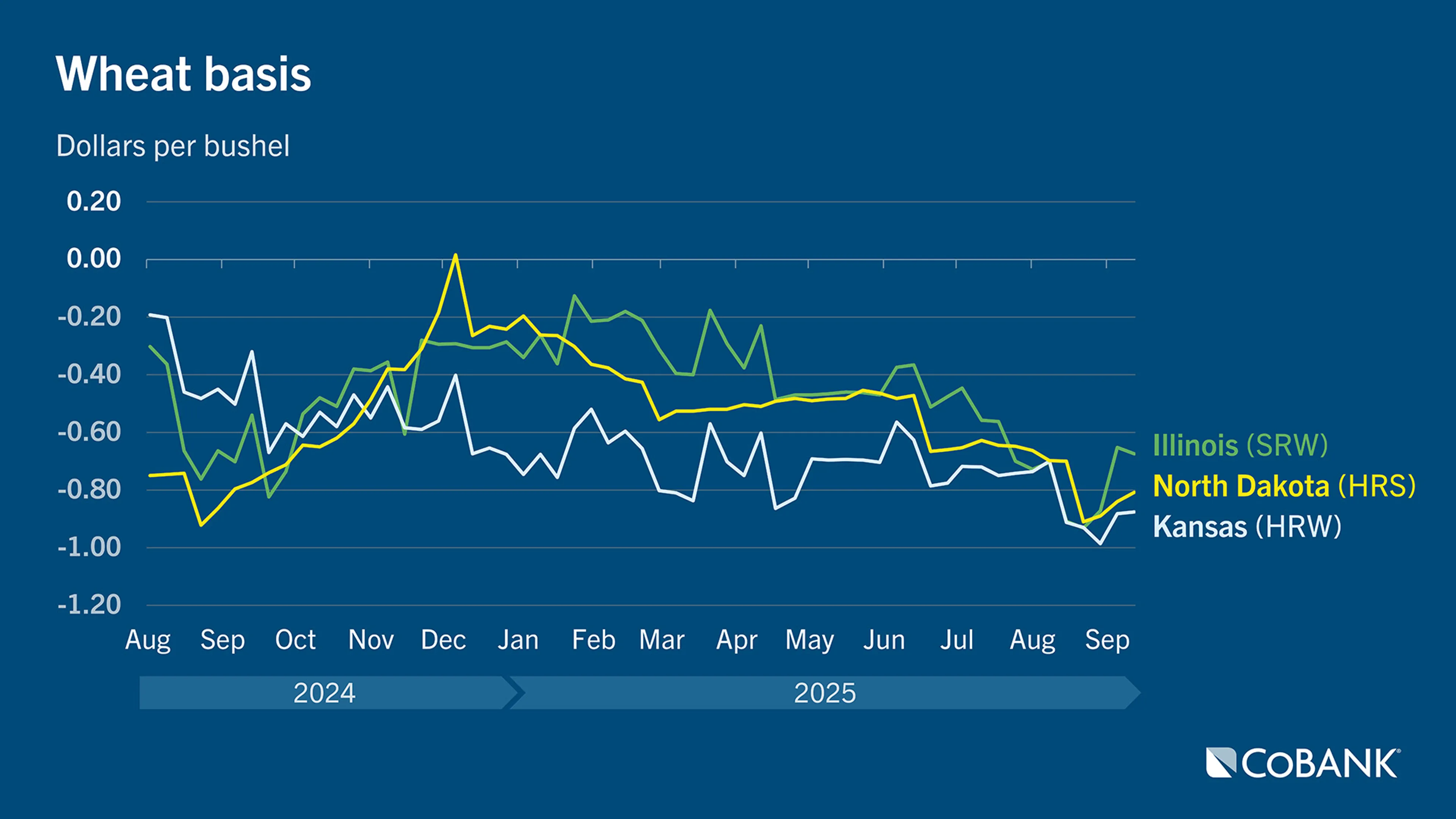

Wheat basis

Elevators are storing more wheat this year following the biggest wheat harvest in five years. With more bushels already in storage, space will be limited in wheat country for the record fall harvest.

Elevators with ample wheat bushels heading into fall harvest are raising storage rates. Although wheat elevators have also benefited from cheaper basis and bigger carries on wheat, some have decided to move wheat to make space for fall harvest.

The U.S. currently is enjoying an impressive export program for wheat, allowing elevators the opportunity to make space for corn, soybeans, and grain sorghum. Increased export competition from the Black Sea region and the southern hemisphere, particularly Australia, will drag on U.S. exports in the months ahead while feed demand for wheat will be limited due to ample supplies of corn, causing wheat spreads to widen.

Implementation of the CME’s variable storage rate (VSR) in October will trigger a wider storage rate, incentivizing elevators to store more wheat, which may tighten basis.

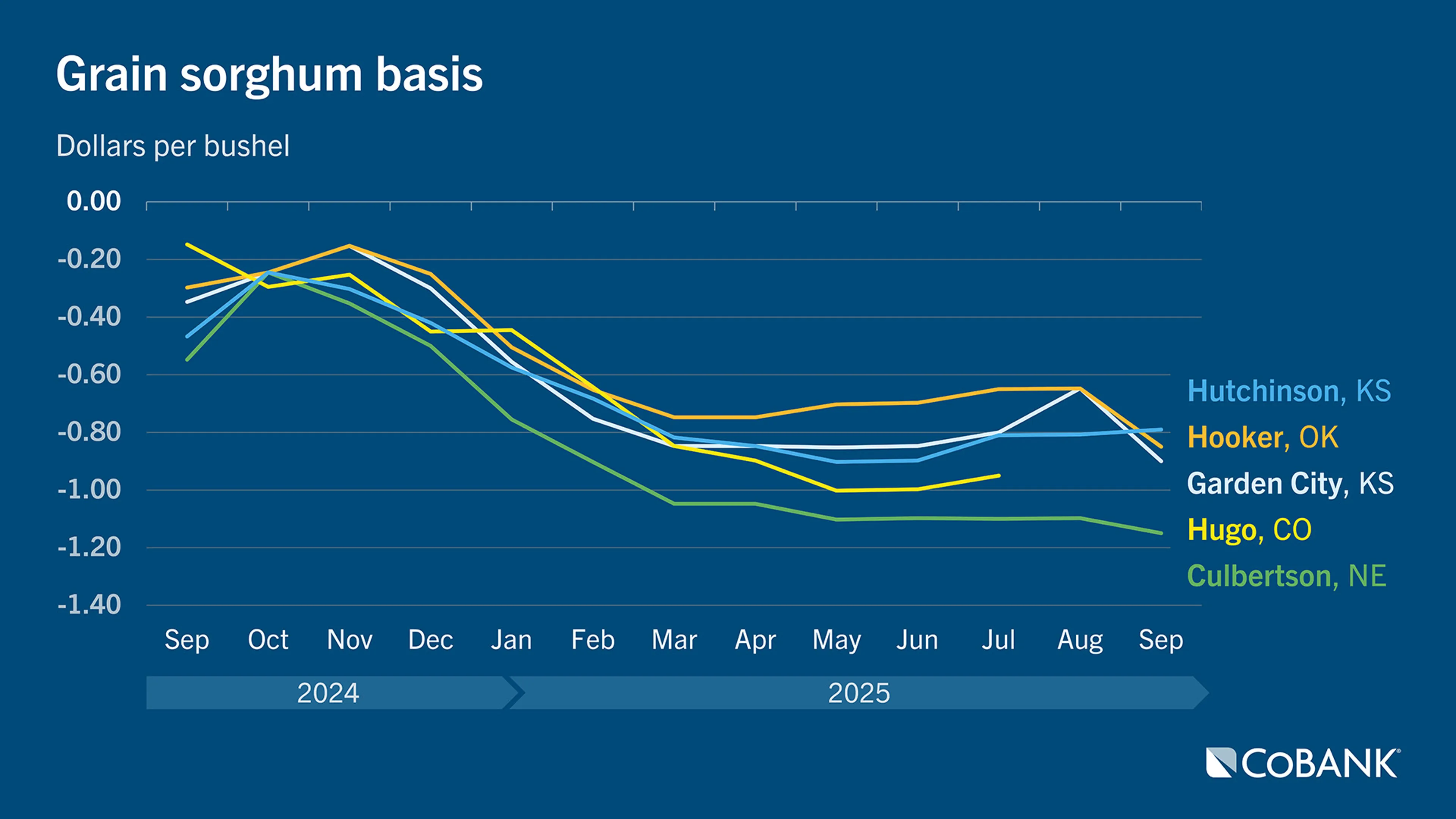

Grain sorghum basis

With China accounting for 80%-90% of historical U.S. grain sorghum exports, the loss of Chinese business has dramatically affected grain sorghum basis.

Grain sorghum basis has fallen to historically low levels with elevators reluctant to take on the risk of buying and storing grain sorghum. Some elevators will not be accepting grain sorghum from farmers this fall. For elevators storing wheat, grain sorghum will likely be stored in bunkers or ground piles.

Strong ethanol demand for grain sorghum has supported basis in some local markets. However, the increased demand has not replaced the loss of export demand. Elevators that are short grain sorghum basis face substantial risk of basis quickly climbing should the U.S. and China sign a trade agreement and a strong export bid for grain sorghum returns.

Persistently low grain sorghum prices may also trigger new demand from other countries like Mexico that see opportunity in feeding low-cost grain sorghum instead of corn, which could prompt grain sorghum basis to rally.

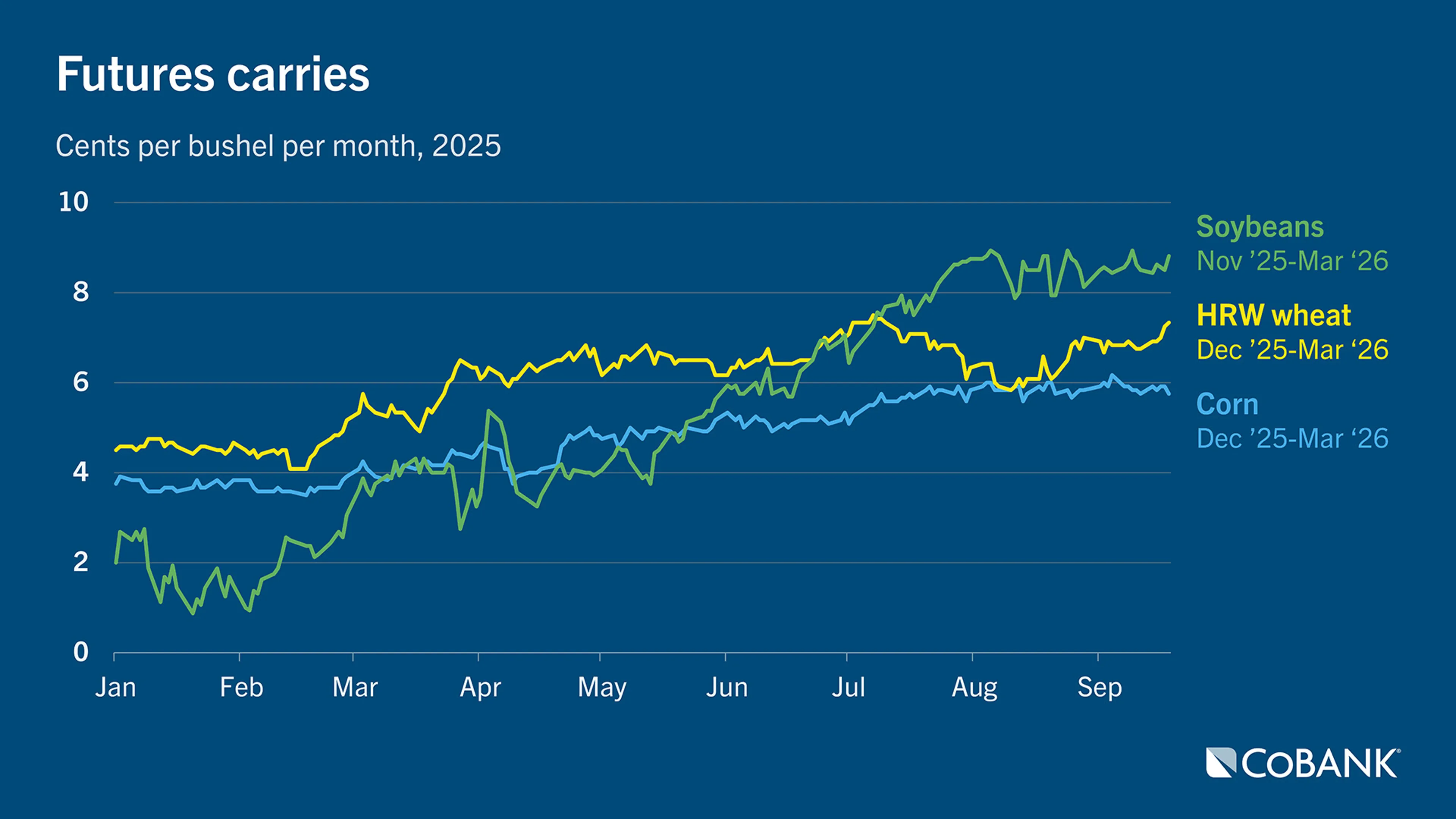

Corn, soybean, and HRW wheat carries

Grain merchandisers will benefit from bigger carries this year for corn, soybeans and wheat that continue to widen, giving elevators ample opportunity to profit on storage.

Elevators, though, must prioritize how they use their scarce storage space. With interest expense top of mind for elevators, soybeans will have the highest cost of carry versus corn, wheat or grain sorghum. Storing soybeans indefinitely amid a slow export pace also comes with the risk of quality degradation over time.

The higher cost of storing grain in ground piles must also be factored into the cost of carrying a commodity over time, due to higher rates of shrink and spoilage and the higher costs associated with moving piles.

Farmers, though, may be reluctant sellers amid low prices, thereby limiting how many bushels the company can own to capture carries in the futures market. Storage fees must be appropriately set to account for elevators’ opportunity cost of not profiting from carries.

Delayed pricing (DP) programs

With commodity prices at multi-year lows, farmers may desire to market grain through delayed pricing (DP) programs where the title of ownership transfers to the elevator and the farmer is able to price the grain at a later date.

DP programs pose a higher risk for the grain merchandiser if the farmer’s marketing price does not cover the cost of carry. Limiting enrollment in a DP program and structuring fees appropriately ahead of harvest may encourage farmers to sell.

Some elevators have opted for cash-only programs with farmers to eliminate the risk and uncertainty associated with DP programs. In lieu of DP programs, some elevators may offer minimum price contracts and extended price contracts to create alternative marketing programs for farmers.

Conclusion

- The record fall harvest will be an opportunity for grain elevators this year to profit on bigger carries, cheaper basis, higher storage fees, and higher turning of assets.

- Elevators face greater risks of storing soybeans and grain sorghum in the absence of Chinese demand. The lack of soybean and grain sorghum exports, though, will make more transportation and elevation capacity available for the strong corn and wheat export programs.

- Low water levels on the Mississippi River may restrict exports and widen basis, particularly for corn and soybeans. The lack of soybean exports to the PNW will continue to depress soybean basis, particularly across the Northern Plains.

- DP programs must be well structured and limited to account for higher risk of carrying unpriced grain for the elevator in a carry market.

- Merchandisers should coordinate with their lenders for appropriate lines of credit to account for greater bushel handles, potentially longer durations of carry, and the risk of a sudden increase of margin calls on short futures positions.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.