Pandemic, higher costs and avian flu put Easter egg supplies at risk

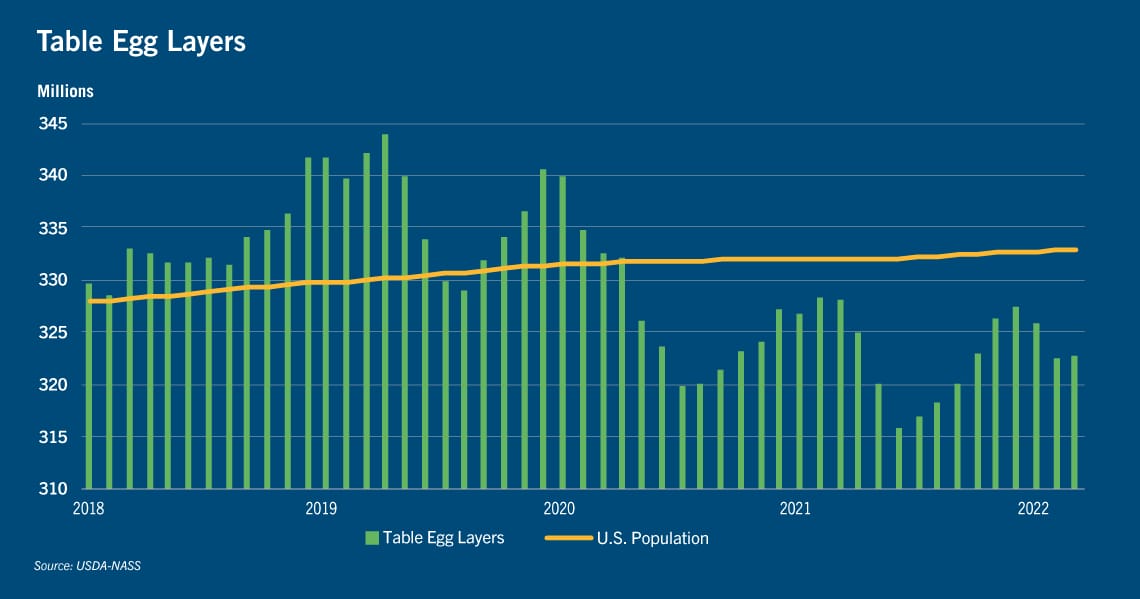

U.S. egg producers have been hard-pressed in the past two years to align supplies with market demand. The flock typically expands ahead of demand for Easter and contracts during the summer months when interest wanes. But overall, the long-term average typically seeks to stay on track with consumer demand (i.e., the U.S. human population). The table egg layer flock trended ahead of target growth in 2019; however, it has fallen well below consumer estimates since then.

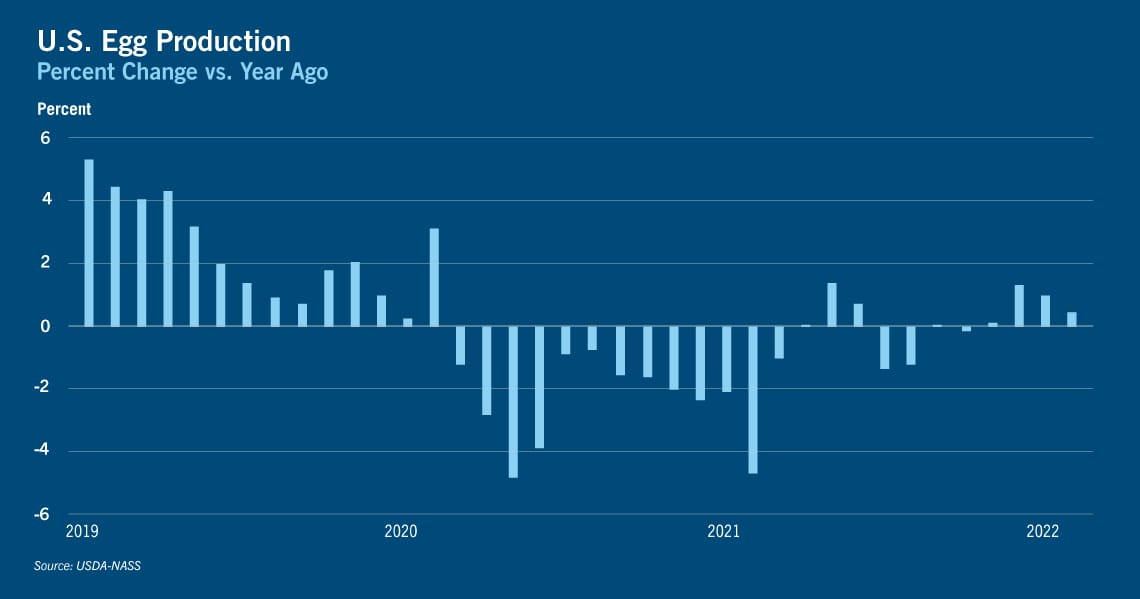

The supply decline stems from extreme shifts in consumer behavior during 2020. Although grocery demand shot through the roof in the infancy of the pandemic, egg producers were not initially set up to shift lost food service volumes into retail channels. The lack of packaging equipment and supplies led to empty store shelves, sky-high retail prices, and ultimately, lower egg consumption. Compounding the pandemic challenges was a 14% YoY increase in the overall 2020 producer price index for large eggs, underscoring the higher input costs for grain, energy, and transportation.

The supply decline stems from extreme shifts in consumer behavior during 2020. Although grocery demand shot through the roof in the infancy of the pandemic, egg producers were not initially set up to shift lost food service volumes into retail channels. The lack of packaging equipment and supplies led to empty store shelves, sky-high retail prices, and ultimately, lower egg consumption. Compounding the pandemic challenges was a 14% YoY increase in the overall 2020 producer price index for large eggs, underscoring the higher input costs for grain, energy, and transportation.The Shrinking Flock

The U.S. table egg layer flock itself is shrinking, from a record of more than 340 million head in April 2019 to about 322 million head as the ongoing cage-free transition has complicated operations. The latest blow is the worst outbreak of Highly Pathogenic Avian Influenza (HPAI) in years – at least 11 million layers have been lost in recent weeks. With APHIS reporting new cases almost daily, and depopulation of operations ranging from in the tens of thousands to more than 5.3 million, it’s hard to say how many more will be lost.

While egg production has stabilized in recent months, it is still well below pre-Covid levels. Weekly supplies have been relatively balanced overall through the beginning of 2022, but sharply higher feed costs as a result of the Ukraine invasion suggests further risk to the egg supply entering this year’s second quarter. Egg reserves listed in freezers in USDA’s monthly Cold Storage report show that, albeit only a small portion of the puzzle at 27 million pounds, total frozen eggs are down about 10 million pounds from pre-pandemic levels, and about 2 million YoY. This suggests risk to wholesale markets if demand returns full circle.

The most recent AMS weekly shell egg demand indicator shows about five days of inventory are currently on hand, which normally suggests a tight but not alarmingly tight supply. However, based on these metrics it does not appear that supplies will be able to accommodate the reduction in layers as a result of HPAI outbreaks, especially at a regional level.

Regardless, it seems obvious that egg availability heading into Easter is sure to be hampered.

These supply pressure coincide with typical in-store grocery features ahead of Easter celebrations. As eggs serve both decorative and cooking purposes, retailers typically rely on eggs as a loss leader. Market forces result in seasonally higher wholesale values for shell eggs ahead of Easter anyways, but with the tight supply situation now exacerbated by flock reductions, prices are cracking fundamental ceilings.

Consumers Face Rising Prices

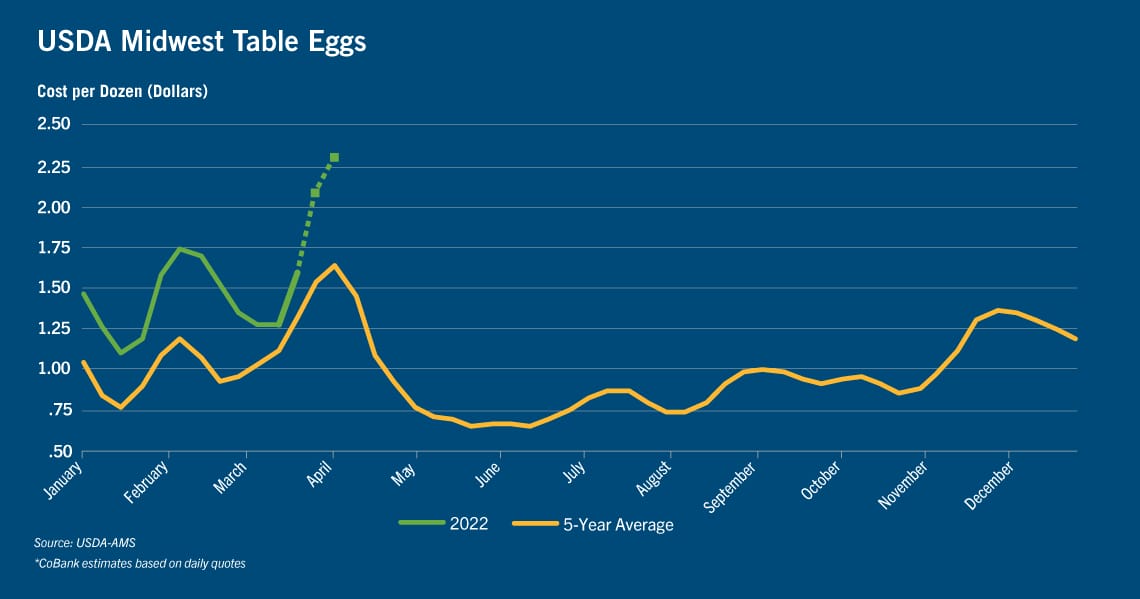

Wholesale prices for cartoned eggs usually range about $0.75/dz.-to-$1.50/dz. The last time the egg market took flight was during consumer runs on product in the early stages of COVID-19. In March 2020, wholesale values were just over $1.00/dz., and went over $3.00/dz. in just two weeks. USDA’s Midwest large cartoned egg quotation has surged roughly $0.25 through mid-March 2022 when compared with the trough at the end of the last rally, but daily quotations suggest prices are on a path to rally $1.00 or more before Easter, and could top the brief highs experienced in 2020.

Producers have an opportunity now. Spot market values usually see their strongest appreciation during peak seasonal interest, suggesting one of the largest opportunities for returns on production will occur during the current period. With supplies potentially spiraling, and stress on conversion to more expensive cage-free-type eggs, consumers appear likely to bear at least a portion of the brunt of higher prices for eggs tendered in 2022, at a time when they are actively seeking low-priced protein items as they grapple with overall inflation.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.