Dairy heifer inventories to shrink further before rebounding in 2027

Key Points

- The U.S. dairy industry is facing a potential shortage of its most important resource – milk cows.

- Replacement heifers available to enter the dairy herd are at a 20-year low just as dairy processors are making historic plant expansions.

- Part of the shortfall is being driven by record-high beef prices, which incentivize dairy farmers to produce higher-value beef calves via beef semen.

- As the supply of dairy heifers has dwindled and their value has climbed, dairy farmers are culling fewer cows to keep the milk flowing.

- While dairy farmers are now purchasing more gender-sorted semen units to produce more dairy heifer calves, dairy heifer inventories will shrink further before rebounding in 2027.

The U.S. dairy industry stands at a unique inflection point previously unseen in its modern-day history: Beef sales are contributing a larger portion to dairy farm profitability with each passing year. This market dynamic has pushed dairy farmers to send more calves to beef feedlots and fewer to milk barns.

As a result, dairy replacement numbers stand at a 20-year low. This is a looming concern as the U.S. is experiencing an historic $10 billion investment in dairy processing facilities through 2027. Those dairy plants will require more annual milk and component production, largely butterfat and protein. That begs the question, will there be enough milk cows given the dramatic shift towards beef semen usage on dairy heifers and cows?

Based on semen sales data, the national dairy heifer shortage could persist and grow deeper in the next two years. Therefore, dairy replacement inventories for the milking herd will not rebound until 2027 based on CoBank models. This will likely cause dairy replacement values to hold at or climb further past prevailing record prices. In the meantime, dairy farmers will continue to pull back on dairy cow culling to sustain herd sizes for financial viability.

A market opportunity

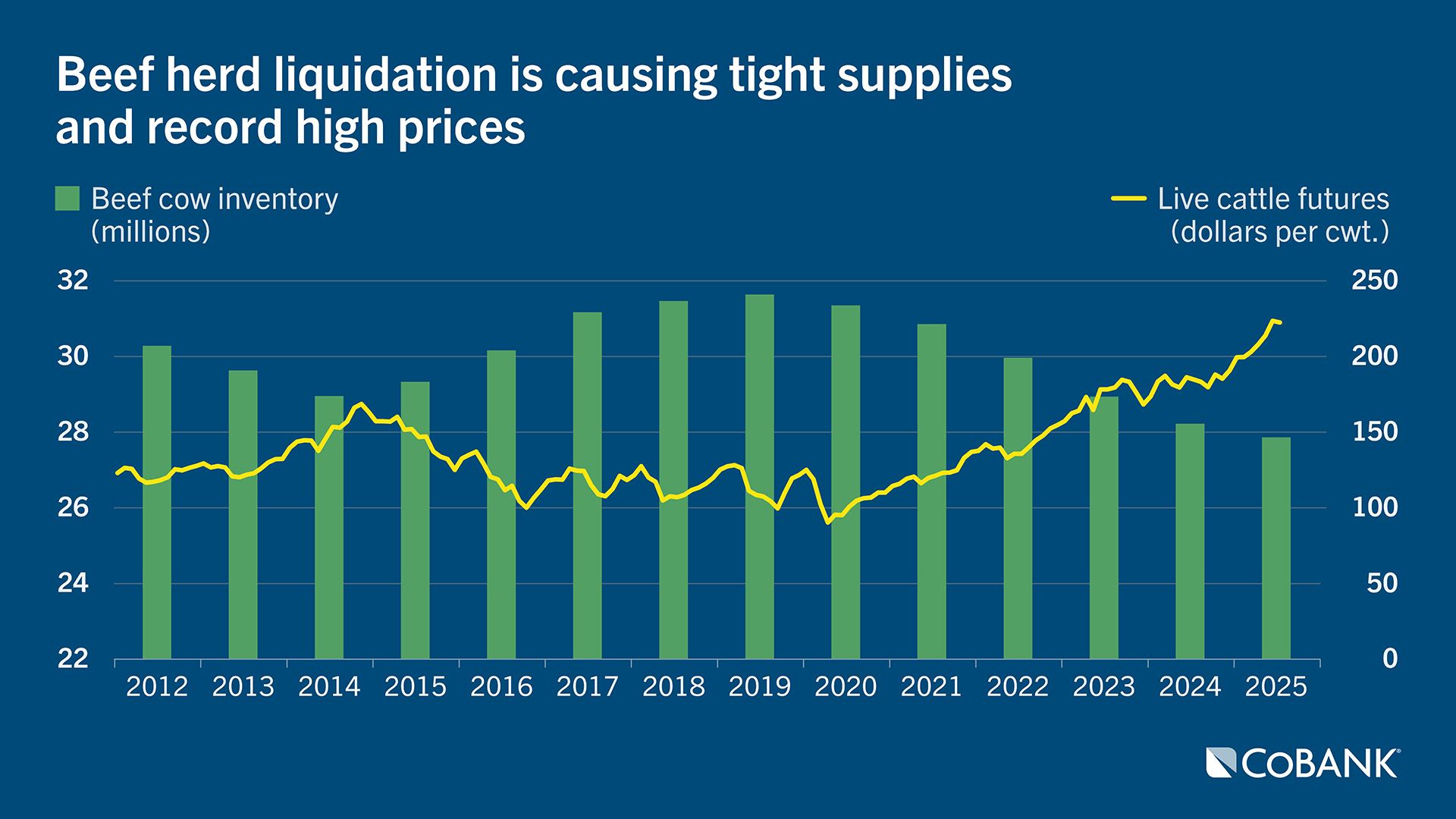

The foundation for this seismic change was set into motion as the U.S. cattle herd contracted to a 73-year low. As of January 2025, total beef and dairy cattle stood at 86.7 million head and USDA’s July 2025 Cattle report pegged numbers at 94.2 million head, the lowest mid-year inventory since 1972.

Limited beef supply and strong consumer demand have driven beef prices to record highs. In August, the nearby October 2025 cattle beef futures pushed even deeper into record territory at prices over $220/cwt, up 20% year-over-year. Outside of an unforeseen market shock, beef prices show no signs of receding in the near term.

Over the last decade, dairy farmers have been receiving lower prices for purebred dairy bull calves when compared to calves sired by native beef breeds. Purebred dairy beef’s larger mature frame size caused issues on the packing floor and were discounted by packers or no longer purchased. Plus, beef-on-dairy calves have better feed efficiency than purebred dairy steers. To remedy the situation, some innovative dairy farmers began breeding a portion of their dairy cows to native beef bull semen to receive higher prices for calves not destined as dairy herd replacements.

This market opportunity was possible because most dairy farmers breed their heifers and cows via artificial insemination (A.I.). Due to high A.I. use, dairy farmers also can utilize two rather new technologies – gender-sorted semen to produce heifer calves on demand and genomics to sort out the best herd replacements via DNA analysis. Additionally, fertility dramatically improved in lactating cows over the past decade as conception rates moved from 30% to 50% and that led to more gender-sorted semen use in cows. As a result, total U.S. beef semen sales nearly tripled from 2.5 million to 7.2 million units from 2017 to 2020. Although a demographic breakdown at that time was not available, the upward shift primarily came from dairy farmers, not beef cattle ranchers who largely rely on natural service bulls.

In 2020, when the National Association of Animal Breeders (NAAB) began tracking beef semen sales to dairy farmers it found they purchased 5 million of the 7.2 million units sold that year. That number eventually climbed to 7.9 million of the 9.7 million units sold in 2024. Dairy farmers’ skyrocketing purchases of beef semen translated to too few dairy herd replacements.

Worth more for beef than for milk

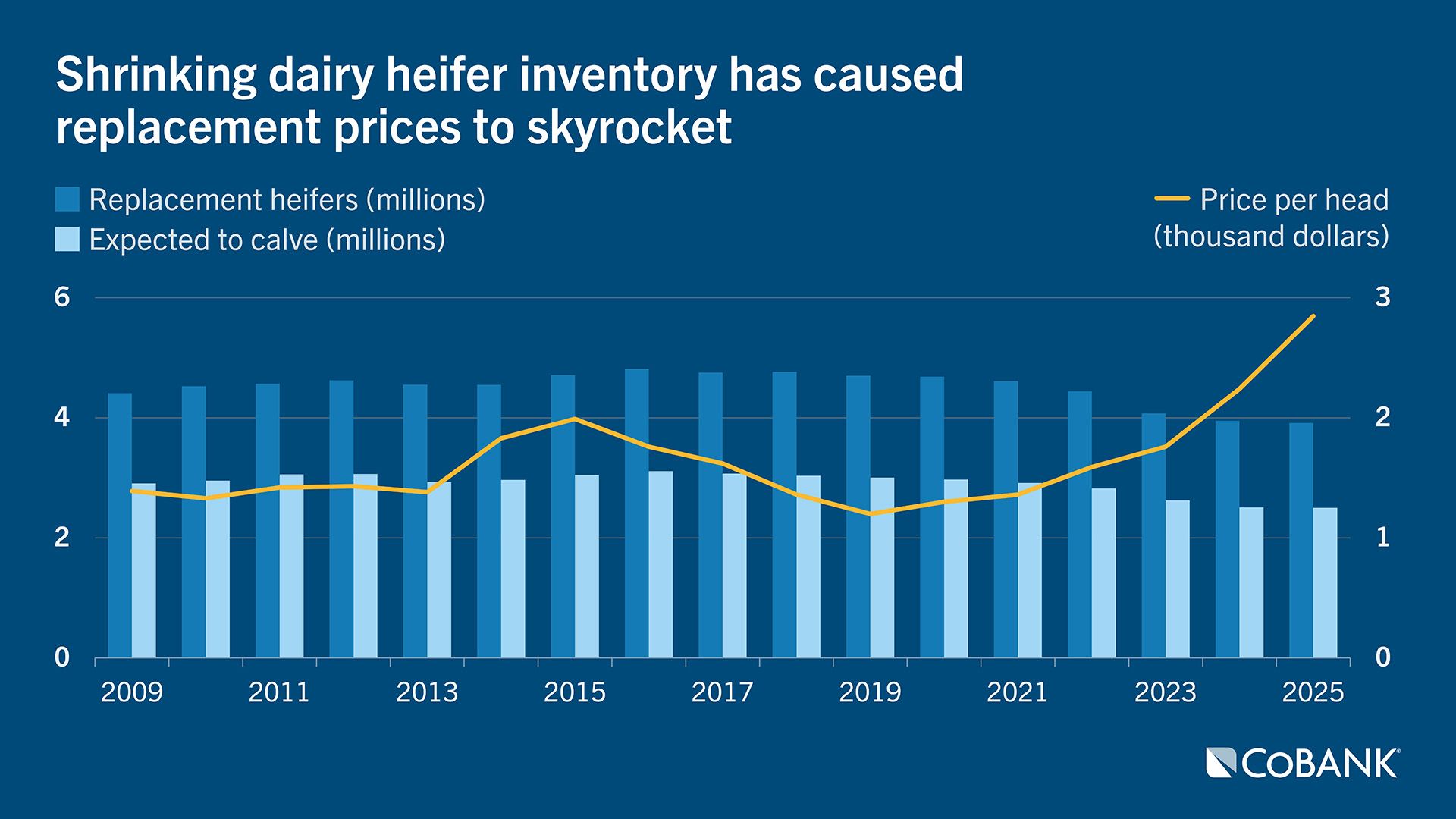

Just as this movement was taking root, dairy replacement prices began to slump. In fact, values dropped dramatically from $2,000 on average in 2015 to a meager $1,200 baseline by 2019 as shown in the chart below. Not only was this far below the nearly $2,000-plus cost to raise those heifers, but the dairy heifer held more value to feedlot operators and packers for beef rather than future milk production. This partial sell-off of dairy heifers further reduced heifer ranks and induced dairy farmers to use even more beef semen on dairy heifers and cows.

By January 2024, the number of dairy heifers weighing 500 pounds or higher – a proxy for the number of dairy replacements expected to enter the U.S. milking herd over the next year – fell almost 15% from 2019. Further proof of the shift taking place was when USDA revised down its January 2023 heifer inventory just one year later by a remarkable 263,600 head.

Dairy replacements shrunk even further to 3,914,300 head in January 2025, 18% fewer than 2018. This shortage caused dairy replacement prices to move from $1,720 per head in April 2023 to the unforeseen threshold of $3,010 per head – a 75% jump – based on USDA’s July 2025 Agricultural Prices. While those prices represent retrospective data, top dairy heifers in California and Minnesota auction barns were bringing upwards of $4,000 per head by mid-year 2025, speaking volumes to the limited supply.

Dairy farmers begin hoarding cows

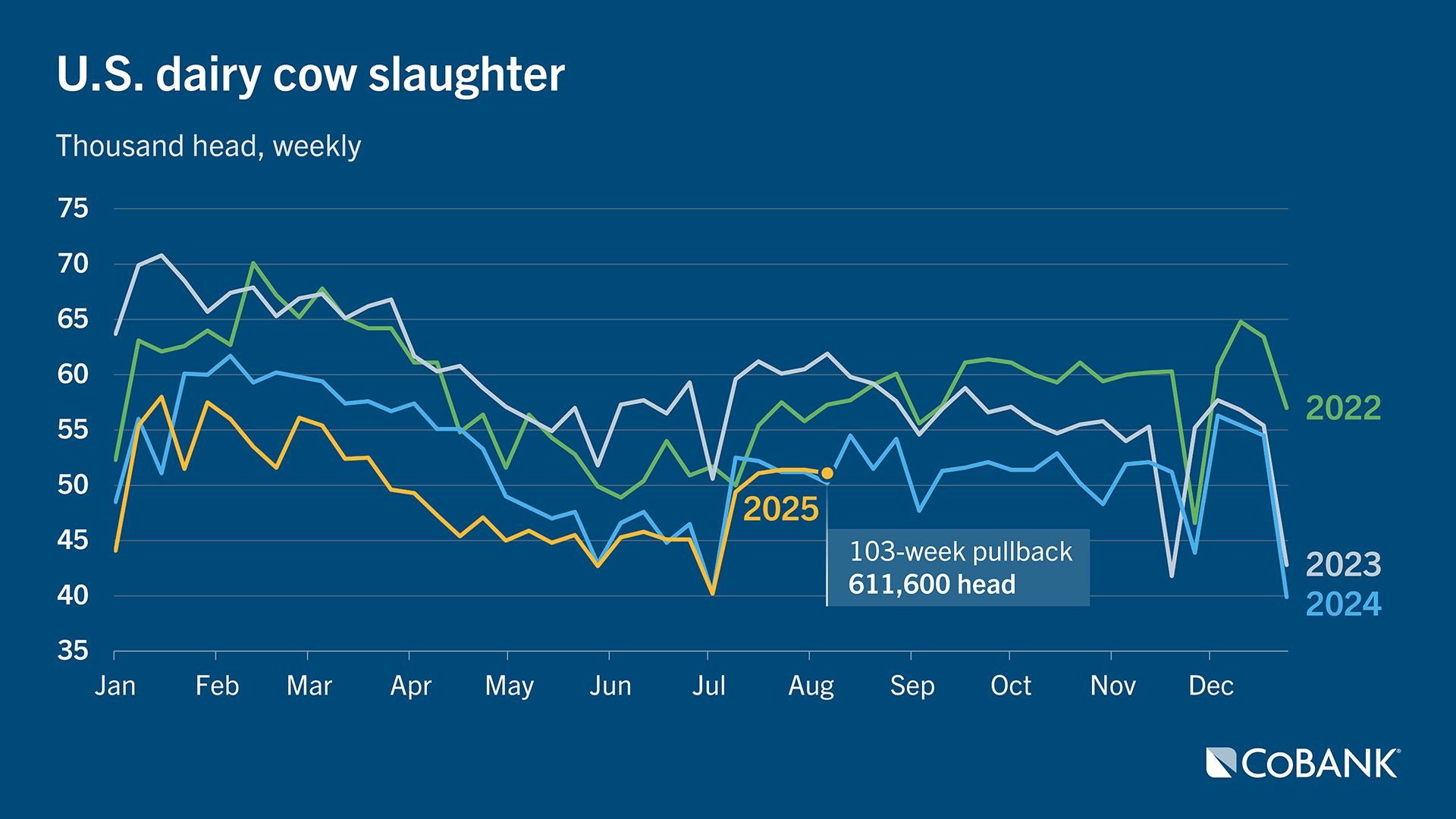

One way to shore up milk cow numbers given the headwinds of limited dairy heifer replacements is to send fewer cows to slaughter. Beginning Labor Day weekend in 2023, dairy farmers did just that. From September through December that year, 104,900 fewer dairy cows were culled compared to the same period the prior year. In 2024, that pullback exploded to 367,400 head based on USDA records from Actual Slaughter Under Federal Inspection. Through July 2025, 103,900 fewer dairy cows were sent to packing plants. All told, 611,600 fewer dairy cows were sent to slaughterhouses since Labor Day 2023. This historic pullback cannot be sustained long term.

Keep in mind that this is taking place with some unique market forces. For starters, 90 percent lean beef trimmings pushed past $400 per cwt. for the first time in market history. However, cull cows could bring more money by producing a beef-on-dairy calf, which has fetched well over $1,000 per head in recent data, at less than a week old. This suggests that dairy farmers may be holding on to cull cows to produce another calf because it is worth more than the cow that was being sent to the beef packer.

Data from Farm Credit East (an agricultural lender in the Northeast U.S.) documents this growing revenue stream. In 2020, cattle sales, including calves, heifers and cull cows, contributed the equivalent of $1.25 per cwt. of milk revenue for a group of Northeast dairy farmers. By 2024, that share grew from 6.7% to nearly 11% as cattle sales netted $2.57 per cwt. While that’s the revenue proposition, the sheer profit is even higher given the lower costs of getting a young calf to market compared with milking a cow for an entire year.

Farmers begin to remedy the heifer shortage

If you are a dairy farmer looking to grow your herd to fill milk market demand with the $10 billion in dairy plant investment coming online through 2027, higher heifer prices just caused that “dairy replacement acquisition” line item on the ledger to double and nearly triple in cost.

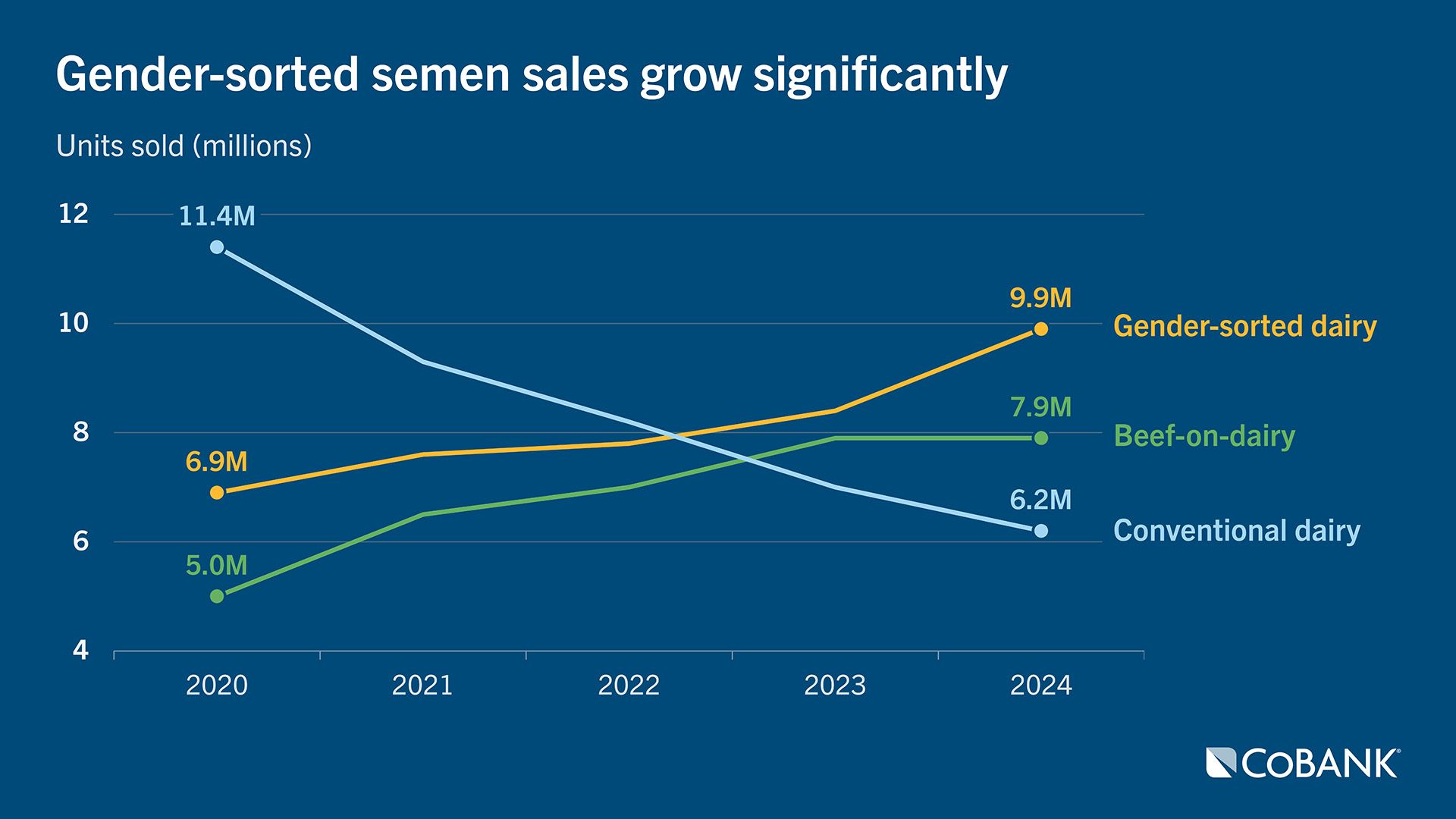

To solve for the situation, U.S. dairy farmers made some significant changes in semen purchases. From 2023 to 2024, gender-sorted semen sales grew by 1.5 million units and represented an incredible 17.9% growth rate in just one year. Conversely, conventional dairy semen purchases, resulting in a 50%-50% chance of a heifer or bull calf, fell 800,000 units and represented an 11.4% downturn. At the same time, dairy farmers kept their eye on the beef-on-dairy prize as beef semen sales to dairy farmers held steady at the record 7.9-million-unit threshold.

These NAAB sale trends show that U.S. semen sales to dairy farmers are quickly consolidating into two major product categories – gender-sorted dairy semen to produce a dairy replacement heifer and beef semen to produce a beef-on-dairy calf.

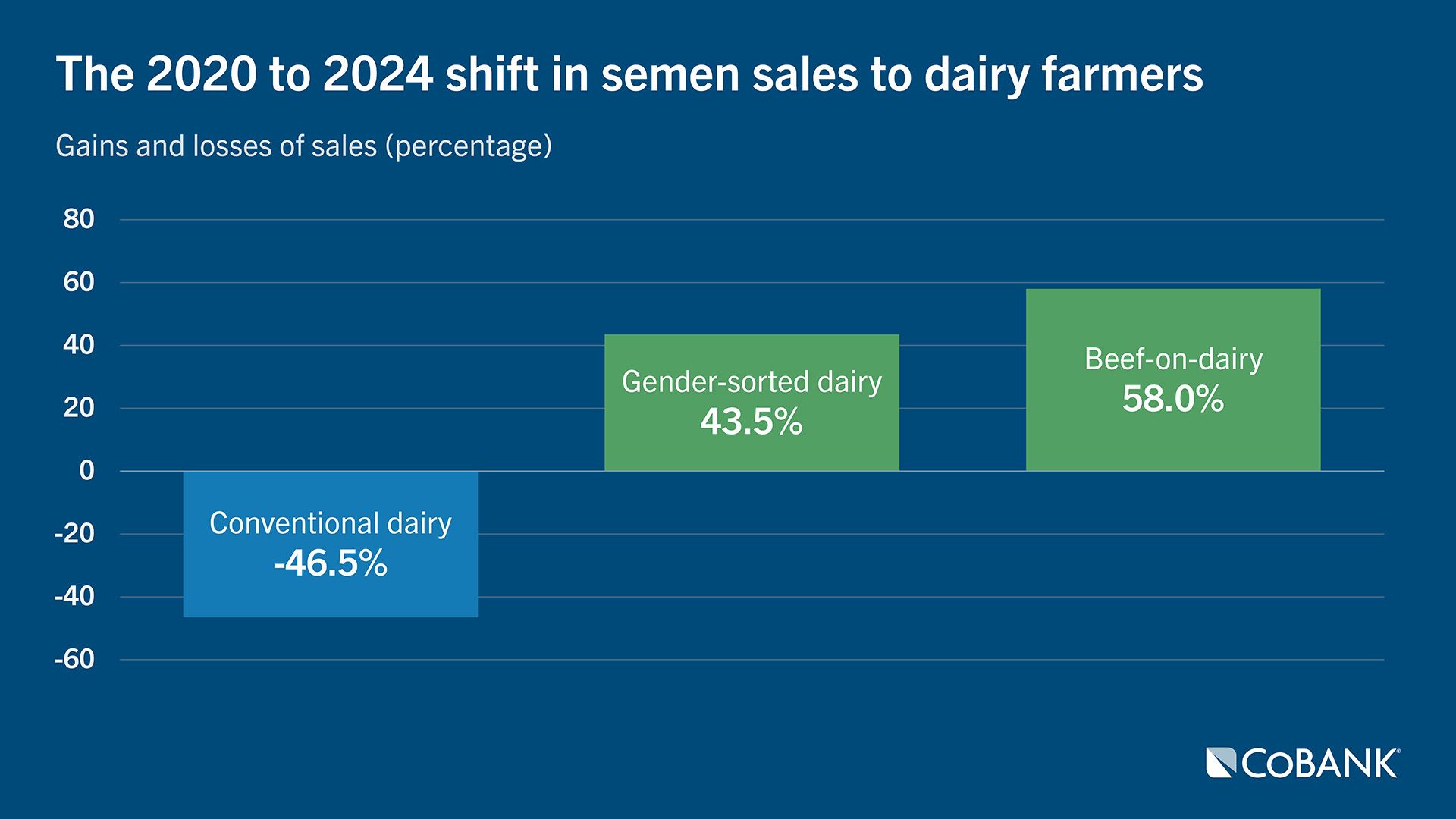

The old standard conventional dairy semen is falling out of favor as dairy farmers want to better manage their outcomes and capitalize on higher revenue streams. From 2020 to 2024, gender-sorted semen sales grew by 43.5% and beef semen sales to U.S. dairy farmers grew at a 58% clip, according to NAAB data. Meanwhile, conventional dairy semen sales plummeted by 46.5%.

What does this mean for dairy heifer inventories?

This data serves as a foundation to forecast the future. The 2024 NAAB sales data, when combined with some biology, allows us to forecast future herd replacements. The 2024 sales year is the best place to start as it represented the largest one-year shift to gender-sorted semen with an additional 1.5 million units sold, and an 800,000-unit downturn in conventional dairy semen. Beef semen sales remained constant from 2023 to 2024 at 7.9 million units.

To forecast eventual live births and full-grown dairy replacements eligible to enter the milking herd, we developed multiple modeling assumptions from scientific research reports, national records analysis and consulting dairy reproduction specialists:

- Gender-sorted semen use, new unit allocation by year: 14% heifers, 43% first-lactation cows, and 43% second-plus lactation cows. It was assumed that most dairy heifers were already being serviced with gender-sorted semen.

- Conventional semen, reduced unit allocation by year: 14% heifers, 43% first-lactation cows, and 43% second-plus lactation cows.

- Conventional semen conception rate of 60% in heifers, 50% in first-lactation cows, and 45% in second-plus lactation cows.

- Gender-sorted semen conception rate of 90% of conventional semen (Reports of conception rates range from 85% to over 95%).

- Gender-sorted semen resulted in 90% heifer calves.

- Pregnancy loss was set at 5% and cows sold pregnant at 5%.

- Completion Rate (number of live heifer calves born and will enter the milk-cow herd two years later) at 79% for dairy heifers based on field data collected from 85 Holstein herds by Dr. Michael Overton with Zoetis. No completion rate was factored for beef-on-dairy as a beef calf does not enter the milking string.

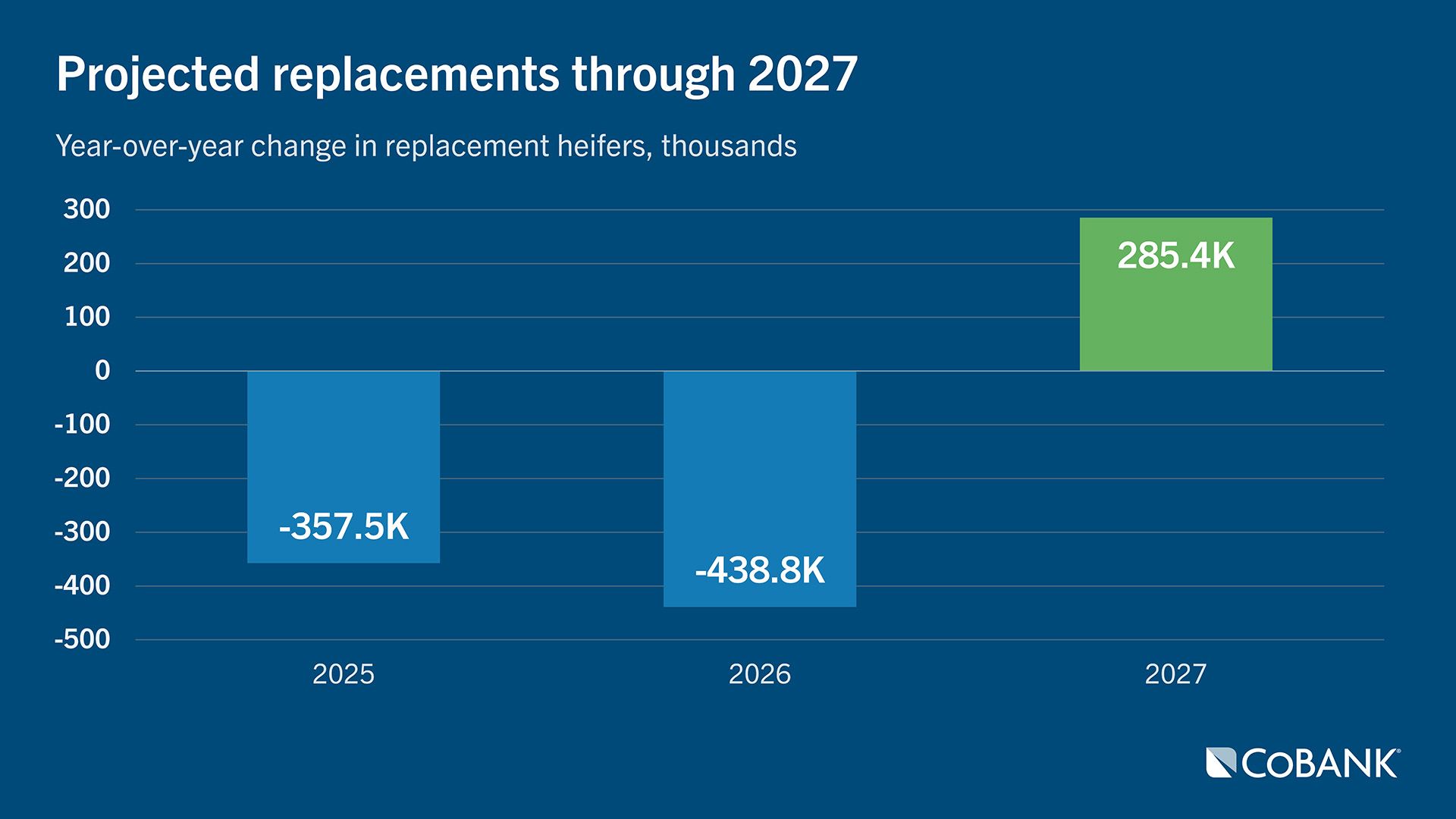

When applying 2024 NAAB semen sales to this model, there is a potential net gain of 285,387 dairy heifers available for herd replacements in 2027 when compared to 2026 numbers.

This number came from 425,454 additional dairy replacement heifers potentially entering the milking herd from gender-sorted semen usage. Likewise, the model found conventional semen produced 140,067 fewer dairy heifers. With no change in beef semen sales, there were no further impact changes.

That’s the good news if one is looking for more dairy heifers. However, the other part of the story is that fewer dairy heifers will be available both in 2025 and 2026. The 2022 sales year indicates fewer heifers available to enter the dairy cow herd in 2025. That year, NAAB sales data resulted in:

- 200,000 more units in gender-sorted semen sales, up 2.6% year-over-year (YoY)

- 500,000 more units in beef semen sales to dairy farmers, up 7.7% YoY

- 1,100,000 fewer units of conventional dairy semen sales, down 11.8%

Here, the model predicted 357,490 fewer dairy heifers for 2025 when compared to the prior year. This was driven by 221,625 more beef-on-dairy calves born that year; 192,592 fewer dairy calves reaching the completion rate threshold due to lower conventional dairy semen sales, and just 56,727 more dairy replacements resulting from gender-sorted semen sales. The 2023 sales year also predicts fewer heifers available to enter the dairy cow herd in 2026. That year, NAAB sales data resulted in:

- 300,000 more units in gender-sorted semen sales, up 7.7% YoY

- 900,000 more units in beef semen sales to dairy farmers, up 12.9% YoY

- 1,200,000 fewer units of conventional dairy semen sales, down 14.6%

In 2026, the model predicted 438,844 fewer dairy heifers when compared to 2025. This was driven by 398,925 more beef-on-dairy calves born that year; 198,925 fewer dairy calves reaching the completion rate threshold based on lower conventional dairy semen sales, and 170,181 more dairy replacements resulting from gender-sorted semen sales.

Relief in two years

No model is perfect. However, a model can help predict the future.

To that end, this model predicts that dairy replacements will remain historically tight through 2026. To maintain cow numbers and the necessary milk production levels, dairy farmers will have to reduce dairy cow culling even further. This will be incredibly difficult given the existing pullback in culling over the previous two years. This aging herd brings a unique set of management challenges as older dairy cows are more susceptible to fresh cow diseases, metabolic issues, and declining fertility rates. The good news is that genetics and health traits have improved over the past decade, and the modern dairy cow should be more up to the challenge.

Lastly, remember that this 285,387-head forecast in net improvement in dairy replacements compared to the prior year. Dairy heifer replacement inventories were already at a 20-year low, and it will take many more dairy heifer calves in future years to bring the national herd back to historic levels. This would be the reason gender-sorted dairy semen sales continue to grow given dairy farmers desire to reap financial rewards from record beef prices.

The authors would like to thank external reviewers including Joe Dalton, Paul Fricke, Michael Overton, Jay Weiker and Nate Zwald.

The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.