U.S. dairy market structure shifts to short on protein, long on butterfat

Key points

- For decades, U.S. dairy markets have been balanced for butterfat while excess dairy protein was exported to international customers.

- In the future, the U.S. dairy industry may be short on protein but long on butterfat given strong consumer demand for dairy proteins and the historic growth in butterfat production.

- The changing dynamics between butterfat and protein production will cause more price fluctuation as dairy processors look to balance product in both domestic and international markets.

The U.S. has been a butterfat-deficit market for many decades. However, the tide has turned, and America may be structurally short on dairy protein moving forward. This will change how products and ingredients are moved in both domestic and export markets. We will balance product flows based on dairy protein production, and butterfat will need to find new markets, with the export market being a significant focus. This transition will create more market volatility, as we have already witnessed from August 2025 through March 2026.

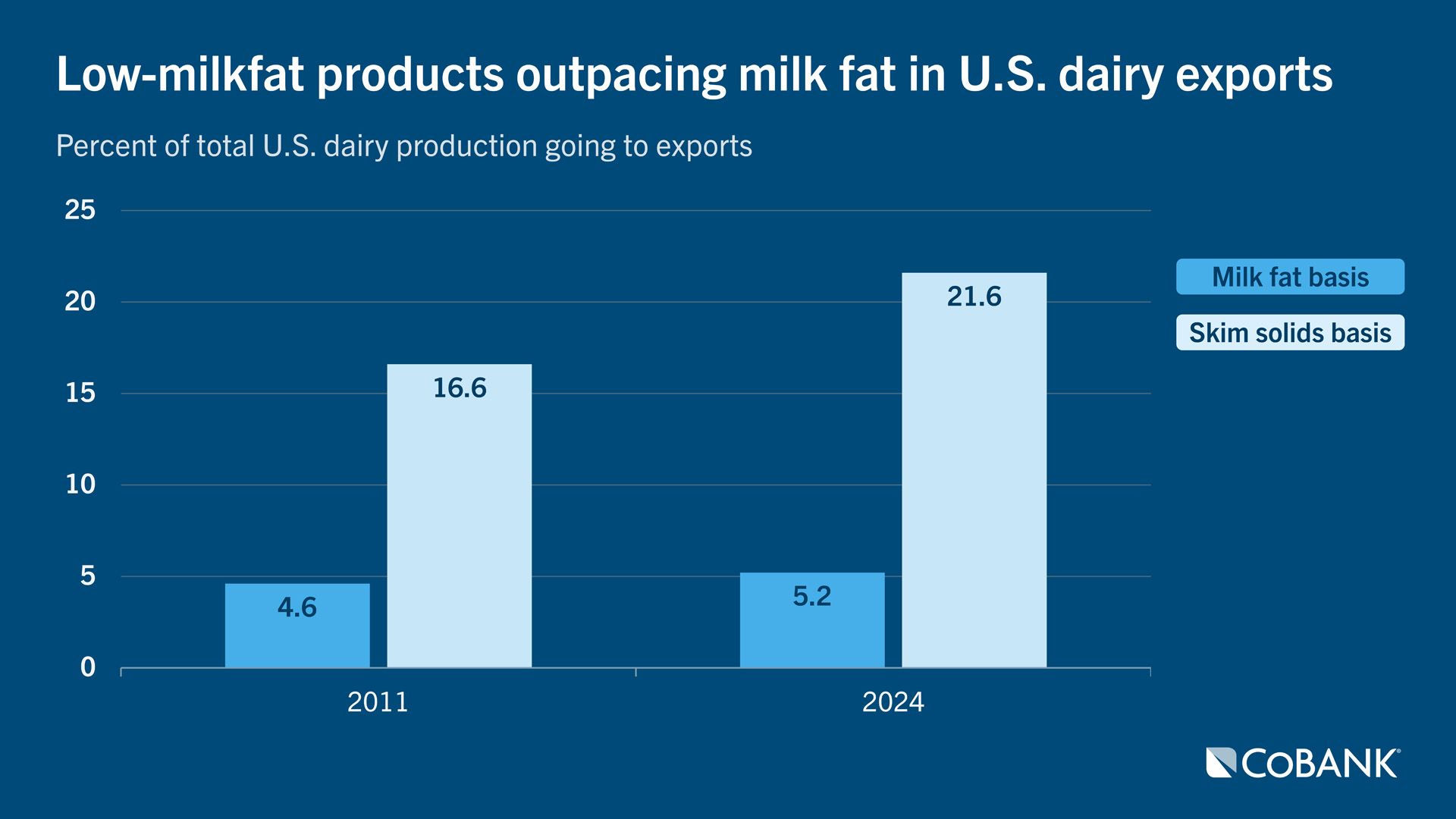

Prior to the creation of the North American Free Trade Agreement in 1994 and the U.S. Dairy Export Council in 1995, the U.S. was largely a nonplayer on the dairy export stage. By 2011, the U.S. was exporting 16.5% of its milk production on a skim solids basis. In other words, the U.S. kept the skimmed off butterfat from the milk stream and sold the skim solids (largely in the form of protein and lactose) to customers around the world. In fact, the spread was so large between the product mix that exports measured on a milk fat basis were a meager 4.6% of U.S. milk production.

The story hadn’t changed much by 2024. That year, U.S. dairy processors exported 21.6% of America’s milk production on a skim solids basis. But exports on a milk-fat basis hardly budged, posting just 5.2% in exports even though total exports represented 17% of the nation’s total milk production. In other words, domestic consumers were buying nearly all of America’s butterfat production in the form of dairy products and little was available for export markets.

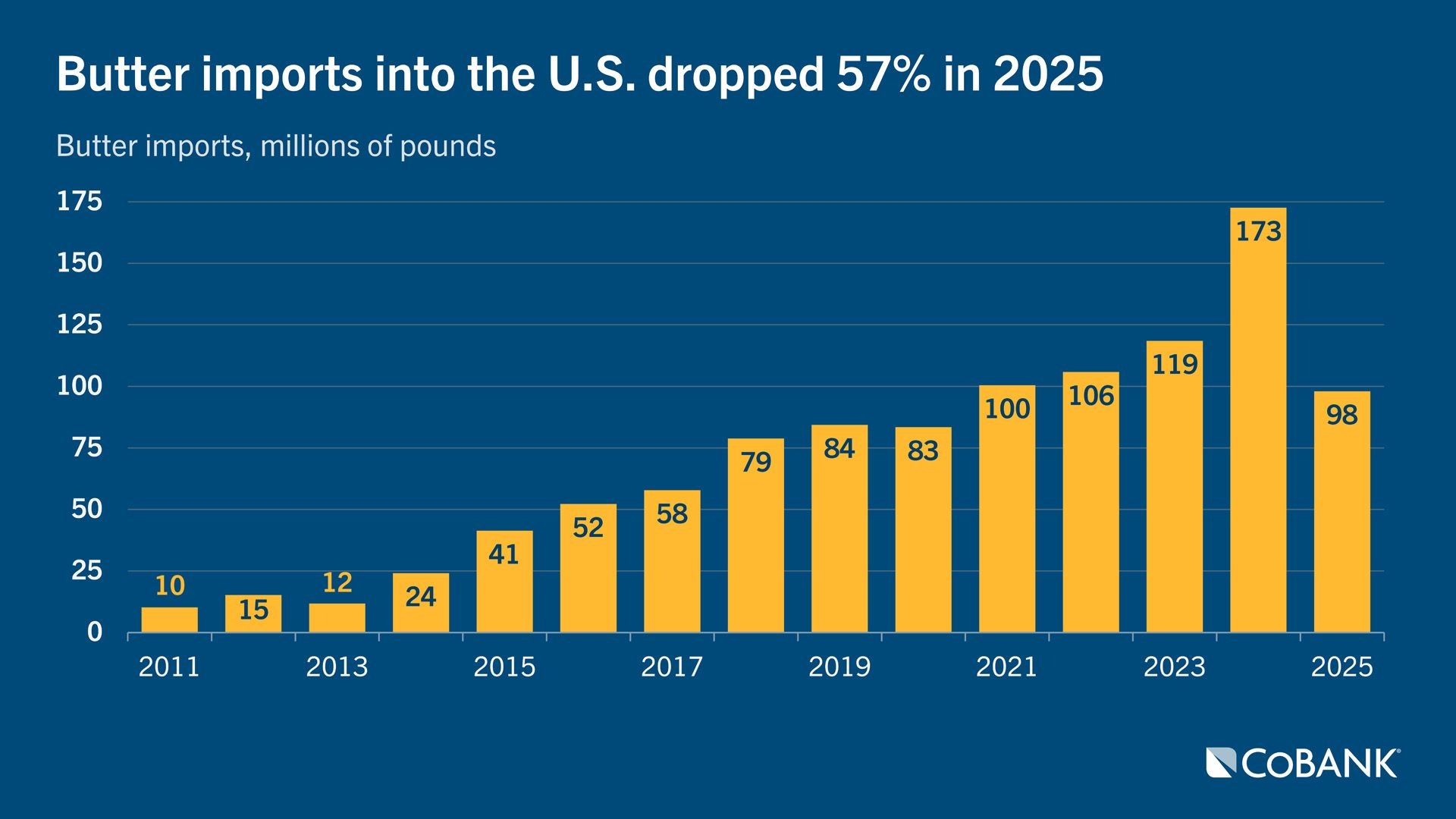

Not only were Americans buying domestic butterfat, but they also started buying more imported butter. In 2011, the U.S. imported 10 million pounds of butter. By 2021, butter imports grew 10-fold to reach 100 million pounds. With more demand from American consumers, butter imports grew another 72% to reach 173 million pounds of imported butter by 2024. With strong domestic butterfat production in 2025, butter imports fell 57% to 98 million pounds.

Along the way, U.S. multiple component pricing factors, via the Federal Milk Marketing Order system, gave stronger signals to produce more butterfat. As a result, butterfat percentages on farm went on a historic run, moving from 3.66% in 2010 to 4.29% in 2025. This growth stemmed from a combination of changes in feed rations and the influx of genetic change via artificial breeding programs and the new science of genomic predictions.

This rapid growth in butterfat eventually pushed the production pendulum in the opposite direction mid-year 2025 — long on butterfat and short on protein. Not only did production of products like cottage cheese, dairy nutritional shakes and Greek yogurt demand more protein and less fat, but butterfat production on a pounds basis also began growing by 5% to 6% in any given month by mid-year. That strong growth began outstripping domestic market demand to absorb farmgate butterfat production.

As a result, butter prices on the CME began to drop from $2.44 per pound on Aug. 1, 2025, to $1.50 per pound by mid-November just when butter sales typically would peak as the holiday season approached.

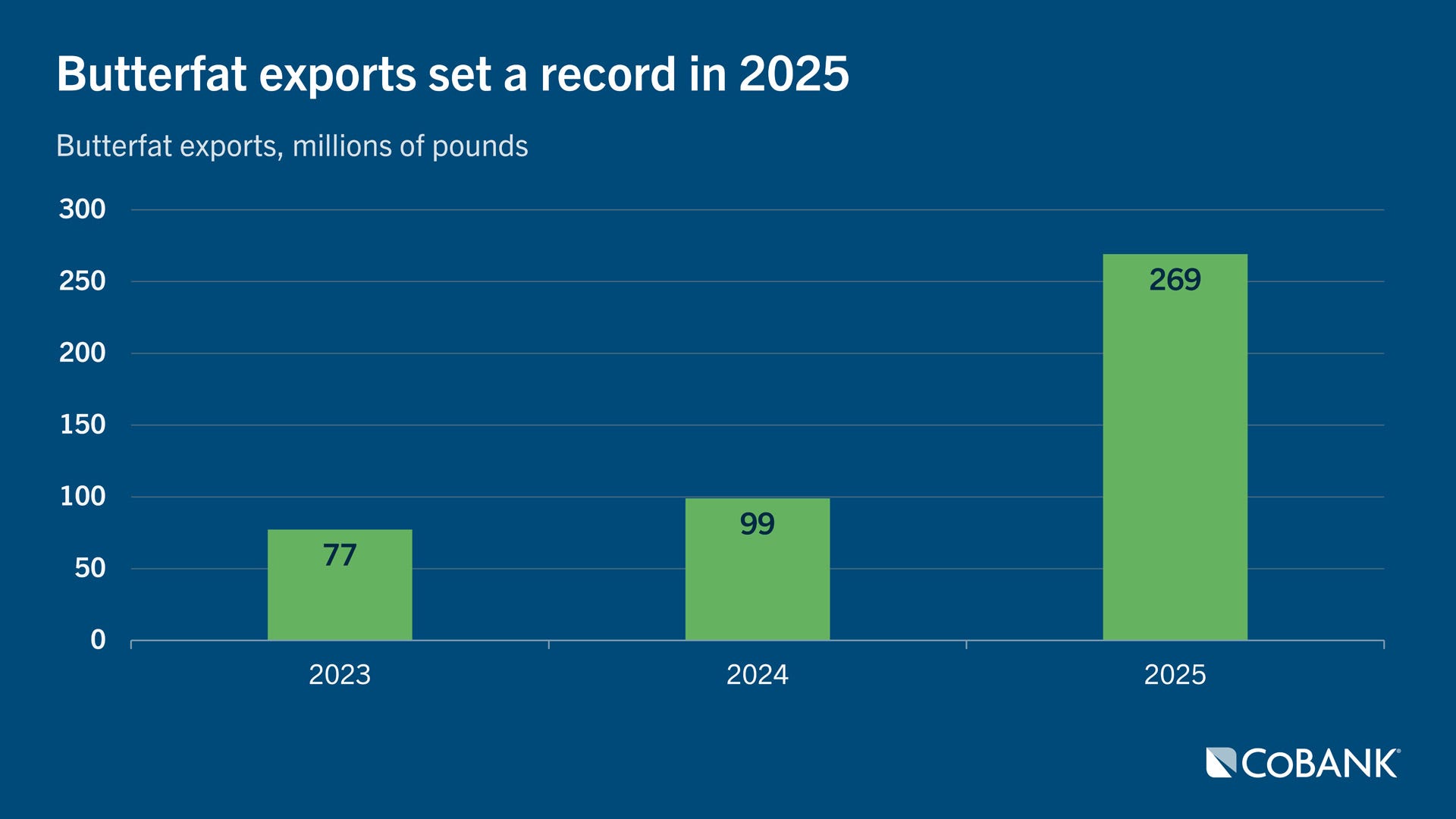

Spot butter prices have since improved to the $1.75 to $2 per pound range. Domestic market demand didn’t improve spot prices; export markets did. The U.S. exported an impressive 269 million pounds of butterfat and anhydrous milkfat in 2025, boosting total export volume 271% from the previous year. More importantly to balancing markets, 60% of those 269 million pounds of butterfat were exported in the second half of the year when the U.S. needed to move inventory.

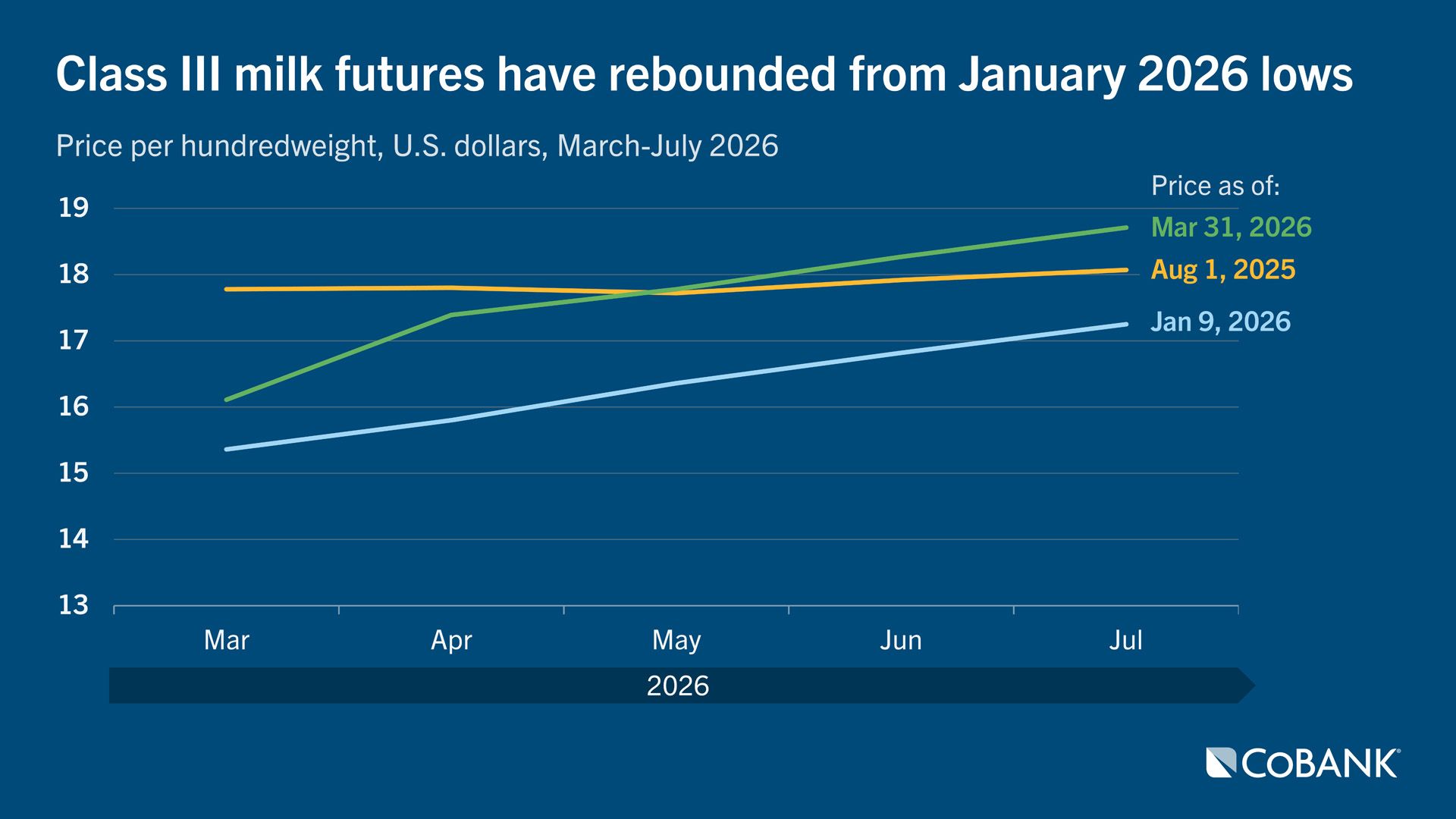

This huge increase in domestic butterfat production has created significant volatility in Class III cheese and whey markets, and an even greater downturn in Class IV butter and powder markets. In August 2025, Class III contracts for March 2026 to July 2026 milk traded between $17 to $18. In January, due to market pressures from butterfat, those same contracts traded between $15 and $17. Then with strong butterfat exports and other factors, March 31 CME futures nearly rebounded to pre-August levels with stronger prices seen in later months’ contracts.

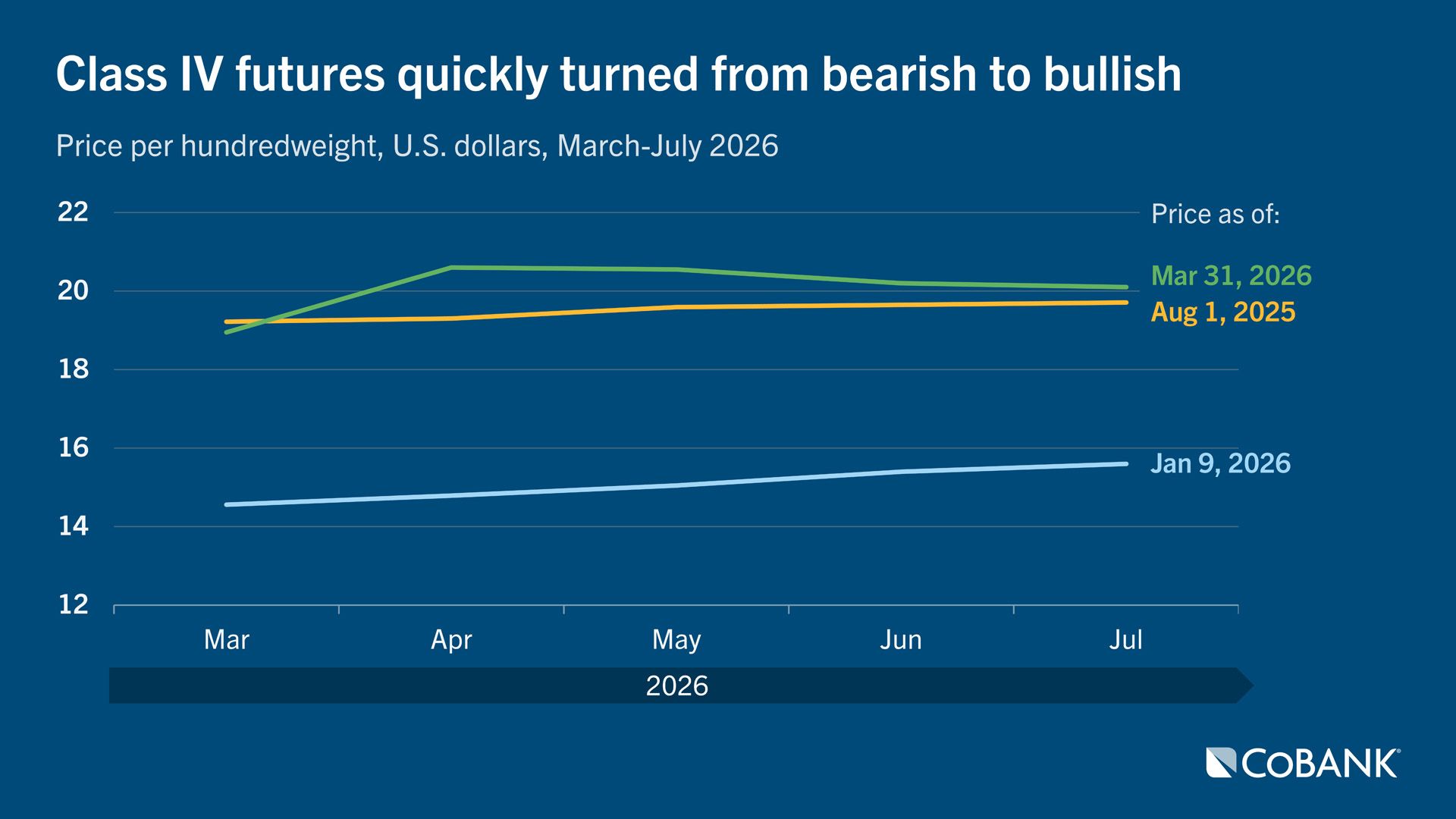

The situation was more dramatic in the Class IV space. In August 2025, all contracts for the March 2026 to July 2026 window traded above $19 per hundredweight. By Jan. 9, 2026, those same contracts dropped to the $14 to $15 range. After the impact of strong butterfat exports and a tightening nonfat dry milk market were realized in the marketplace, March to July 2026 CME Class IV futures climbed to pre-August 2025 trading levels and in some months those contracts traded close to $20.

Dairy markets are not out of the proverbial woods. The 2025 export year might been even better had there not been geopolitical issues and tariffs making an impact. The largest catalyst supporting U.S. sales growth was lower cheese and butter prices compared to the world’s top two dairy exporters — the EU and New Zealand. Given this situation, dairy farmers and processors alike should consider hedging opportunities when market prices look favorable and cover expenses because small product movements could significantly move prices.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.