Why the AI capex cycle may just be beginning

Key points

- Hyperscaler AI-related capital expenditures (capex) are accelerating rapidly, growing from an estimated $235 billion in 2024 to a projected $700+ billion in 2026.

- Strong returns on invested capital, explosive AI application growth, and robust supply chain guidance suggest the AI infrastructure cycle may still be in its early stages.

- Early evidence suggests AI is already driving meaningful productivity gains across both hyperscalers and the broader economy, despite weak labor force growth.

- While risks exist due to market concentration and interdependent ecosystem relationships, today’s AI infrastructure market differs materially from the excess-capacity environment of the 2000 dot-com era.

Introduction

Capital expenditures related to artificial intelligence are reaching unthinkable levels as hyperscalers such as Amazon, Microsoft, Meta and Google race to build next-generation AI technologies that will profoundly impact how we live and work. For example, in 2024, U.S. hyperscalers spent an estimated $235 billion. In 2025, that figure climbed to $400 billion, with expectations of more than $700 billion in 2026.

AI-related capex is not only impacting U.S. GDP, but it is also a driving force behind the recent rise in stock prices. The highly concentrated nature of this capital spending — and the outsized impact it is having on financial markets — is fueling concerns that any slowdown in spending could burst the proverbial AI bubble. While this concern has merit, a closer look at the profitability of this spend, along with broad feedback from across the AI ecosystem, suggests this capex cycle has yet to fully play out.

AI ecosystem is surging

To gauge market conditions and assess whether spending is excessive, it helps to study the broader AI ecosystem — especially what key market players are saying, and more importantly, what they are doing.

The AI ecosystem largely consists of hyperscalers (who are the driving force behind this AI revolution), model developers, semiconductor manufacturers, memory-chip makers and networking companies.

Numerous model developers, and even some hyperscalers, are developing their own models. However, the market is largely centered around OpenAI (ChatGPT) for the consumer market and Anthropic (Claude) for the enterprise market. Other notable players include xAI (Grok), Google (Gemini) and Meta (Llama).

On the semiconductor side we find NVIDIA, whose GPU technology underpins the entire AI revolution; Broadcom, which develops application-specific semiconductors; and TSMC, the most advanced semiconductor manufacturer in the world which is building the lion’s share of AI chipsets. Lastly are the memory manufacturers, which include Samsung, SK Hynix, and Micron Technology.

Examining the broader AI infrastructure ecosystem suggests spending levels should remain healthy for the foreseeable future. Take NVIDIA, for example. The company recently announced a line of sight to more than $1 trillion in cumulative revenue for its AI GPU chipset business through the end of 2027, a massive increase from the approximately $130 billion the company generated in fiscal year 2025.

One can also look at memory-chip maker Micron, whose products are integral to the AI capex cycle. The company recently reported second quarter revenue of $23 billion — a staggering 196% year-over-year increase and well above investor expectations — while guiding third quarter revenue to $33.5 billion. OpenAI reported earlier this year that its revenue had reached $2 billion per month, up from the estimated $2 billion it delivered in all of 2023.

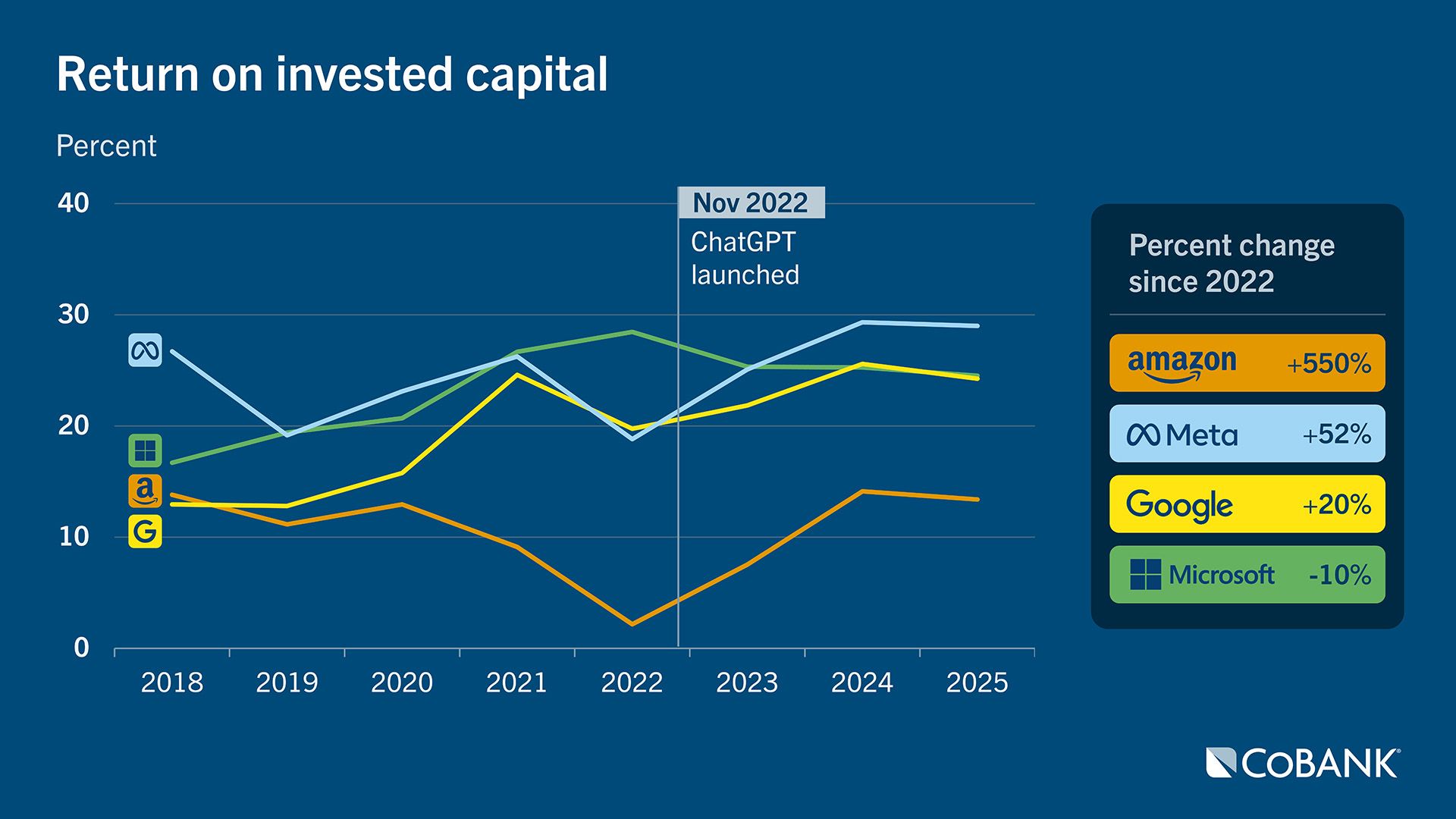

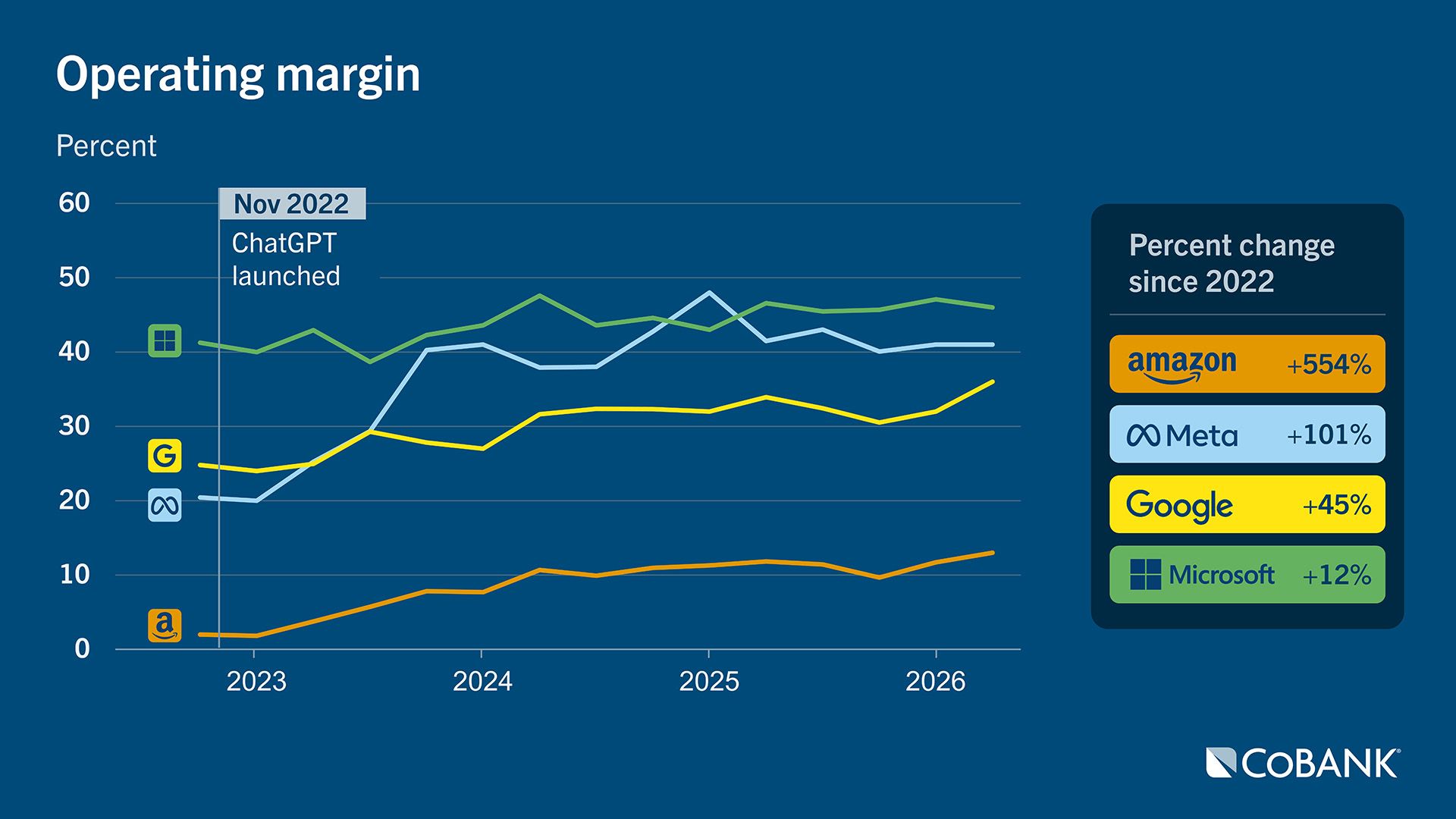

Another way to think about capex sustainability is to ask whether this level of capex is actually creating value for shareholders.

One answer is to look at hyperscalers’ return on invested capital. If ROIC is rising alongside increased capex, then the answer is yes, these investments are creating shareholder value. That is exactly what is happening today. Given that, along with the red-hot AI ecosystem, one can reasonably conclude this capex cycle may not be over.

How hyperscalers monetize their capex

In its most basic form, hyperscalers make money in AI by “selling” tokens, which are fundamental units of data that convert text or images into numerical sequences that AI models can understand. Every chatbot request, image generation, coding request, and AI query produces tokens. Think of tokens as digital electricity for AI. And as AI evolves, demand for tokens is exploding.

To quote Jensen Huang, CEO of NVIDIA, “Compute is revenue. Without compute, there is no way to generate tokens. Without tokens, there’s no way to generate revenue… If the new software requires tokens to be generated and the tokens are monetized, then it stands to reason that their data center build-out directly drives their revenues.”

The last few years of AI investment has been building the infrastructure foundation and large language models that will support the next phase of AI: inference.

Inference is where application developers create AI applications for end users by leveraging large language models. And these new applications are quickly evolving into AI agents that perform tasks and take actions versus just answering questions like the early AI chatbots. These new AI agent-based applications are generating 10–100 times more tokens than traditional chat-based AI applications, according to some estimates. Considering that within the next two years the average Fortune 500 enterprise is expected to run more than 150,000 AI agents, token generation is poised to explode.

To get a sense of how much revenue growth AI applications are generating, one needs to look no further than Anthropic. Anthropic develops AI applications for the enterprise market, and its revenue growth has been nothing short of parabolic.

Founded in 2021, Anthropic is now valued at approximately $900 billion. Its revenue run rate (a figure used to estimate annual revenue based on short-term sales) is expected to reach $50 billion by the end of June, up from $30 billion in April and $9 billion at the end of 2025.

As mind-blowing as these results are, they could have been even stronger with greater access to data center compute capacity. Anthropic is trying to ease its compute shortage through a recently announced partnership with Amazon, committing to spend over $100 billion on AWS technologies in return for 5 gigawatts of compute capacity.

The rise of AI agents is also changing the hyperscalers’ business model. Increasingly, hyperscalers are selling “digital labor” rather than simply storage, compute, and networking services like they did in the traditional cloud business.

As AI agents scale, become more advanced, and transcend industries, the resulting impact will be growing demand for data centers and tokens. For hyperscalers, the key challenge is determining how to cost-effectively support the rising demand for digital labor and token growth while continuing to invest heavily in AI infrastructure.

AI productivity impact

Much has been made about the productivity impact AI will have on the broader economy, and for good reasons.

To grow an economy, you need two basic elements:

- Growth in the size of the workforce

- Productivity improvements through technological advancement

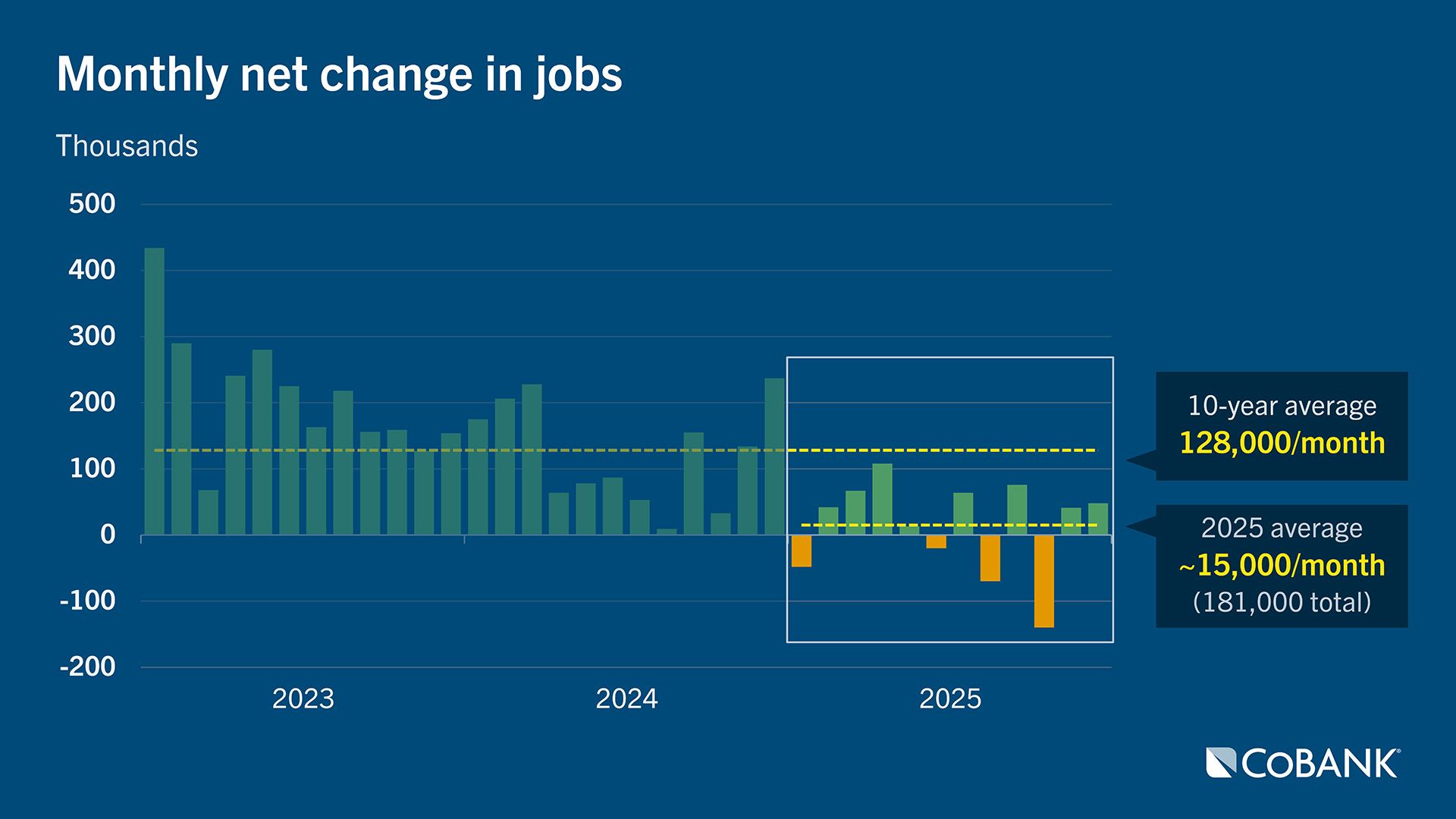

The fact that job growth in 2025 was anemic while the economy still grew at 2.1% suggests technology improvements had an outsized impact on GDP growth.

We recognize that other factors, such as AI infrastructure investments, could also explain GDP growth despite weak job creation. That is why we attempted to isolate AI’s impact on productivity by analyzing hyperscalers’ profitability since ChatGPT was launched.

Our assumption is that hyperscalers were likely among the first major companies to deploy AI internally, given their early insight into and development of frontier models. As such, they may serve as a proxy for how AI could/is impacting the broader economy.

Meta has been leveraging AI to optimize its advertising business. For example, generative AI tools allow advertisers to automatically generate images, backgrounds, and ad copy — significantly reducing the time and expense for small business marketing budgets. And the benefits are not just cost-related. Businesses using these tools reportedly saw a 7% increase in conversions compared to non-AI-generated content.

Another example is Meta’s Andromeda system, where before an ad auction begins, an AI model scans millions of ads, user behavior patterns, and engagement histories to determine which ads are most relevant to enter the auction, all within milliseconds. This reportedly drove a 22% increase in return on ad spend.

Amazon has also been aggressive in deploying AI via warehouse robotics and predictive models that determine what customers will buy, where they will buy it, and when. This has improved inventory management and reduced logistics costs. Last year, the company reduced package travel distances by 12%, while handling touches fell 15%.

Stepping back and examining hyperscalers’ profitability since ChatGPT launched shows very impressive profitability gains. Therefore, if AI played a meaningful role in these gains — which seems logical — then it bodes well for the positive productivity impact AI could or is having across the broader economy.

This also sets the stage for hyperscalers’ continued investment to support increased AI usage and token generation.

Where are the risks?

On the risk side, comparisons have been made between today’s environment and the 2000 dot-com recession. We do not believe that is a fair comparison.

In 2000, excess capacity in the form of dark fiber networks was a primary culprit behind the market collapse; today, there is no comparable excess capacity in the AI infrastructure market.

Additionally, valuations were generally higher during the dot-com era, and today’s AI companies have significantly healthier cash flows and more established revenue streams than many technology companies did in 2000.

One area of concern, however, is the increasingly circular nature of deals between major AI ecosystem participants. These companies are becoming more interdependent, raising the concern that the failure of one company to meet its obligations could trigger a broader contagion event across the market. That scenario is possible, but for now it appears more likely that one company’s failures would result in isolated disruptions rather than systemic risk.

And of course, the growing energy supply/demand imbalance puts the timing of new projects at risk. The industry is facing significant energy challenges given the surge in demand for electrons, the underinvestment in the grid and the extended lead times for natural gas turbines and other energy related infrastructure.

The supply chain challenges are not limited to energy infrastructure. Demand for high-bandwidth memory is so strong that current bottlenecks could persist through 2030, according to memory-chip maker SK Hynix. Demand for optical equipment and fiber is also at levels not seen before with lead-times stretching to 12 months for some products. And of course, with strong demand and tight supply, prices are shooting up. Fiber pricing has increased 50% since January and many expect it to keep rising. And then there is the growing community pushback over AI data centers, putting many new projects at risk of not being approved.

While the AI ecosystem faces many risks, it’s important to remember that most of these risks are not indicative of a bubble but rather represent execution and timing risk. The market demand remains very healthy.

Conclusion

Despite an unprecedented amount of capital being deployed by hyperscalers, and the inherent risks associated with a high degree of market concentration, numerous signs suggest AI infrastructure spending has a long way to go.

The supply chain is guiding toward enormous growth, hyperscalers are reporting strong and rising returns on invested capital, the economy continues to grow despite weak job creation, and pure-play AI companies such as Anthropic are delivering parabolic revenue growth as enterprises rapidly adopt AI.

The interconnected nature of the AI ecosystem and the circular relationships between participants do present risks, but at this point those risks appear isolated rather than systemic.

The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.