Chocolate lovers shift to premium brands as cocoa prices swing

Key points

- Prices for cocoa futures plummeted from the first of the year, dropping to almost half their New Year’s Eve level.

- The chocolate manufacturers who opted against hedging at higher prices in the fall have greater pricing flexibility now.

- Retail chocolate prices are not guaranteed to drop, however. Manufacturers appear to be investing in alternatives to avoid supply challenges that prompted the rise in cocoa prices.

- Double-digit chocolate price increases over the past year have dented retail sales volumes. However, consumers of premium chocolate varieties in particular, are showing resilience when it comes to their chocolate purchases.

Futures prices of cocoa have dropped by almost half since the first of the year. But retail pricing of chocolate brands continues to be elevated, as cocoa prices outpace traditional levels posted two-plus years ago.

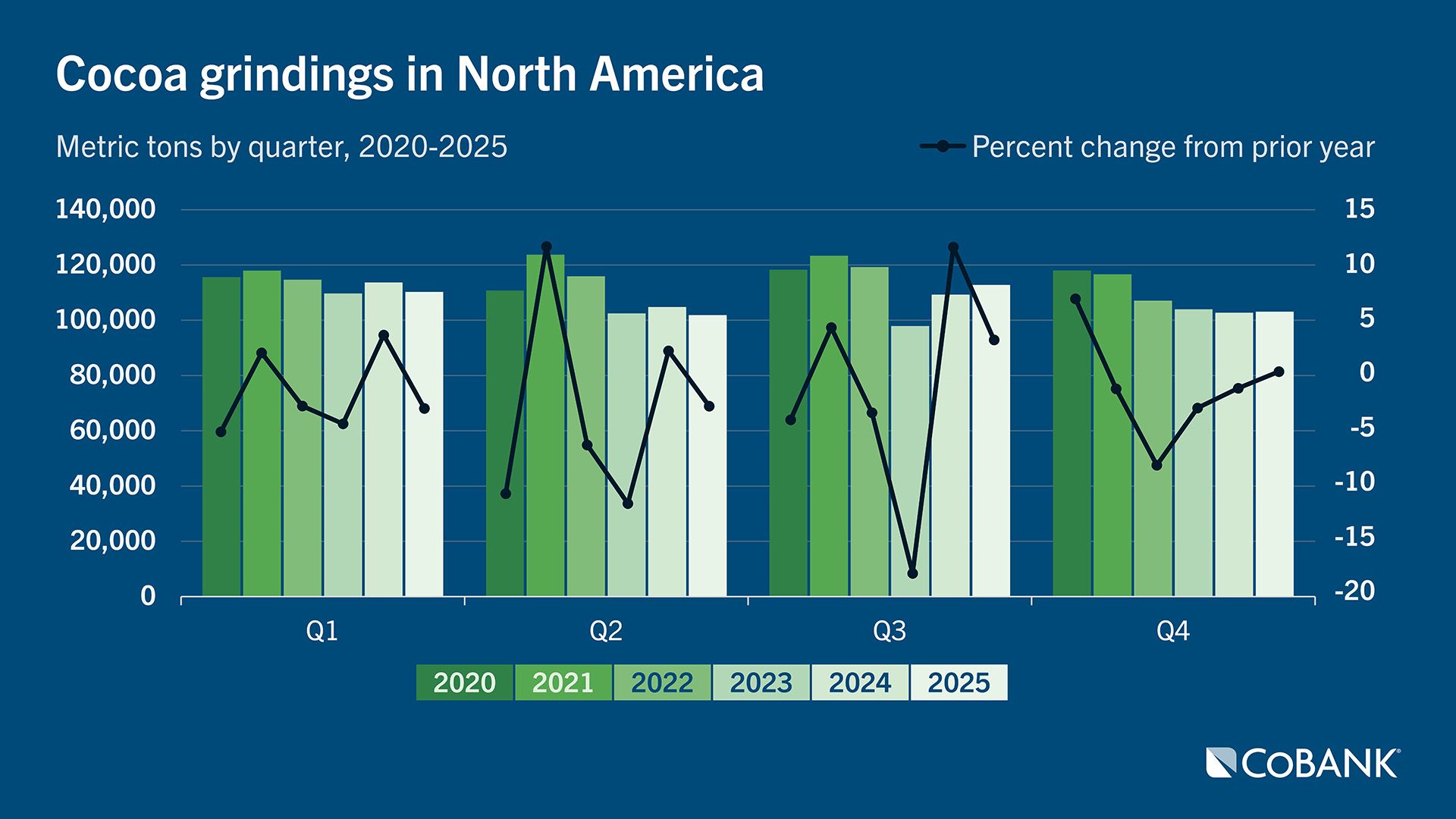

Despite challenges for the world’s cocoa growers, cocoa grinding levels have been relatively stable in recent quarters. (The grinding process turns roasted cocoa beans into cocoa liquor, the essential base for all chocolate products.) According to the National Confectioners Association Chocolate Council, grindings volume has steadily held above 100,000 metric tons since the dramatic year-over-year drop in the third quarter of 2023.

Yet the story and concerns surrounding cocoa have been in its futures pricing. In January 2025, futures were well above $10,000 per metric ton and were even near $10,000 by May. Futures prices then started to steadily decline but were over $6,000 even as recently as New Year’s Eve. Prices have fallen dramatically in the weeks since, to roughly $3,100 in March 2026.

Pricing impact

The recent decline in cocoa prices will not likely correlate with a similar drop in chocolate candy retail prices. Last fall, a number of chocolate manufacturers hedged at around the $6,000 mark, half the all-time high set in late 2024. That hedge, though high in retrospect, leaves companies little room to take pricing measures, and even those that did not hedge appear unwilling to reduce retail prices.

Speaking at the February meeting of the Consumer Analyst Group of New York (CAGNY), Mondelez CEO Dirk Van de Put said his company did not hedge on cocoa last fall. And unless and until cocoa dipped below $3,000 per metric ton, he also did not expect to make any pricing adjustment on its brands (which include Cadbury, Toblerone and Milka). For other brands, higher retail prices are helping cover their costs but at the expense of volume sales:

- Hershey reported a net income drop of 59.9% in the fourth quarter of 2025, citing volatility in the cocoa market as one of the most significant headwinds.

- In its most recent earnings call, Nestle noted the possibility of continued pricing adjustments stemming from hedged volumes, noting they “expect pricing to likely be higher.”

- Similarly, Swiss chocolatier Lindt & Sprüngli took its highest-ever pricing last year. And while organic growth was 12.4% in 2025, volume/mix fell 6.6%, with further volume declines expected this fiscal year.

Primed for premium

The largest beneficiary of the drama surrounding cocoa, ironically, may be premium options, whose entire reputation is built on cocoa content. Indeed, as internal Lindt research has found, even users of weight-loss drugs are eating more, not less, chocolate. However, they are upgrading to smaller, premium offerings. Circana data confirm the power of premium: Premium chocolate sales among U.S. GLP-1 users rose 17% in 2025, compared with 6.5% among non-users.

This suggests that consumers on these medications are not simply dismissing indulgences but making them less of an impulse purchase and more of a mindful experience — one built less around habit and ease and more of a selective indulgence. Candy brands have long positioned themselves around the point-of-sale locations in the supermarket, as an easy treat selected while checking out without much consideration. These shoppers (certainly current GLP-1 users, but potentially those who begin using the drugs and even those who cycle off of them) have shown a tendency to be more selective in their chocolate experience.

Noting consumer demand for cleaner labels and quality offerings, Grand View Research projects the premium chocolate market will grow at a 4.3% compound annual growth rate through 2030. In fact, a Cargill study finds a sizable portion of consumers willing to pay more for higher-quality chocolate. The supplier found 58% of consumers would pay 10% more for premium ingredients such as dark chocolate. The long-term consequence for the chocolate category could well be further opportunities beyond that impulse-driven role. This includes its maturation as a premium experience smaller in size but carefully chosen for flavor, experience and potentially even healthy attributes associated with higher cocoa content, namely cardiovascular health, antioxidants and satiety, the latter already a key area of interest for GLP-1 users.

Impact on producers and manufacturers

Ghana and Ivory Coast, which account for roughly two thirds of the world’s cocoa production, did not expect the sharp drop in global prices, despite reporting increases in their crop yields. The thinking was that the largest global cocoa deficit in 60 years — a supply half a million tons short of demand — would keep prices higher. Ghana’s cocoa sector was so confident of this scenario that it adjusted the producer price for its farmers just weeks prior to the drop, creating considerable financial challenges once futures dipped on those increased yields. The price slump meant government-contracted cocoa could only be sold at a significant loss, as much as $3,000 per metric ton by some estimates, ultimately putting the government’s losses at $2 billion.

Compounding difficulties for cocoa producers have been tariffs. Cocoa is one of the few agricultural products that had tariffs removed in November 2025, but prior to that, Ivory Coast and Ghana faced a 15% rate, leading a number of manufacturers to turn to alternative sources. This, along with the challenges surrounding cocoa production in recent years, has furthered interest in cocoa extenders and alternatives from ingredient manufacturers.

Chocolate manufacturers, meanwhile, are looking for ways to decrease the impact of supply challenges, quality fluctuations and volatile cocoa pricing. Such moves have not been without their controversies, whether from taste alterations resulting from reformulations or the negative public opinion of “shrinkflation”:

- Hershey found itself the target of criticism from a descendent of the inventor of the Reese’s peanut butter cup, who alleged the company had switched the milk chocolate from the original recipe to a compound coating.

- Toblerone took a different route, adjusting the design of its iconic chocolate peaks, increasing the gaps in the product to reduce the amount.

- Cadbury Dairy Milk reformulated some items in its line with up to 5% non-cocoa vegetable fats such as palm and shea oils with cocoa butter.

Other companies have opted for ingredient innovation. Mondelez invested in Celleste Bio, an Israeli startup developing lab-grown cocoa butter, participating in a $4.5 million seed funding round for the company to scale production. It is Mondelez’s second investment in the company, as Mondelez indicates it is looking for sustainable alternatives to the volatile harvests that now come with conventional farming - and its associated reputation around deforestation.

Similarly, Puratos has partnered with California Cultured to craft a commercially viable lab-cultured chocolate. The Belgian ingredients firm anticipates availability by the end of 2026. Numerous companies envision lab-grown cocoa yet face distinct barriers in cost, regulation and, ultimately, consumer acceptance. Costs, presumably, can be mitigated with scale, and regulatory approval could be a challenge in and of itself, as the U.S. Food and Drug Administration is reconsidering Generally Recognized as Safe (GRAS) standards.

The principal concern will be consumer reaction to the resulting flavor alterations, even if such innovations presumably lead to lower prices. Chocolate prices on U.S. store shelves continued to surge into early 2026, with Datasembly reporting a 14.4% increase in the year’s early weeks compared to the same period in 2025.

Nevertheless, consumer demand for chocolate has remained largely unchanged. As trade journal Bakery & Snacks observed about chocolate consumption, “People notice what’s happening. They complain about smaller packs. They grumble about price. Then they buy anyway.”