This digital guide is a practical resource to help electric cooperatives address the unique challenges of integrating large loads. Based on candid interviews, market research and analysis, this guide shows how cooperatives are earning new business and delivering value to their communities—while adopting robust contract structures to protect members from bearing the costs of serving large loads.

knowledge exchange

The state of large load rate design: Insights from the DELTa database

Key points

- Decades after stranded assets bruised local communities, electricity utilities and regulators are revisiting how to interpret “cost responsibility” for new large loads.

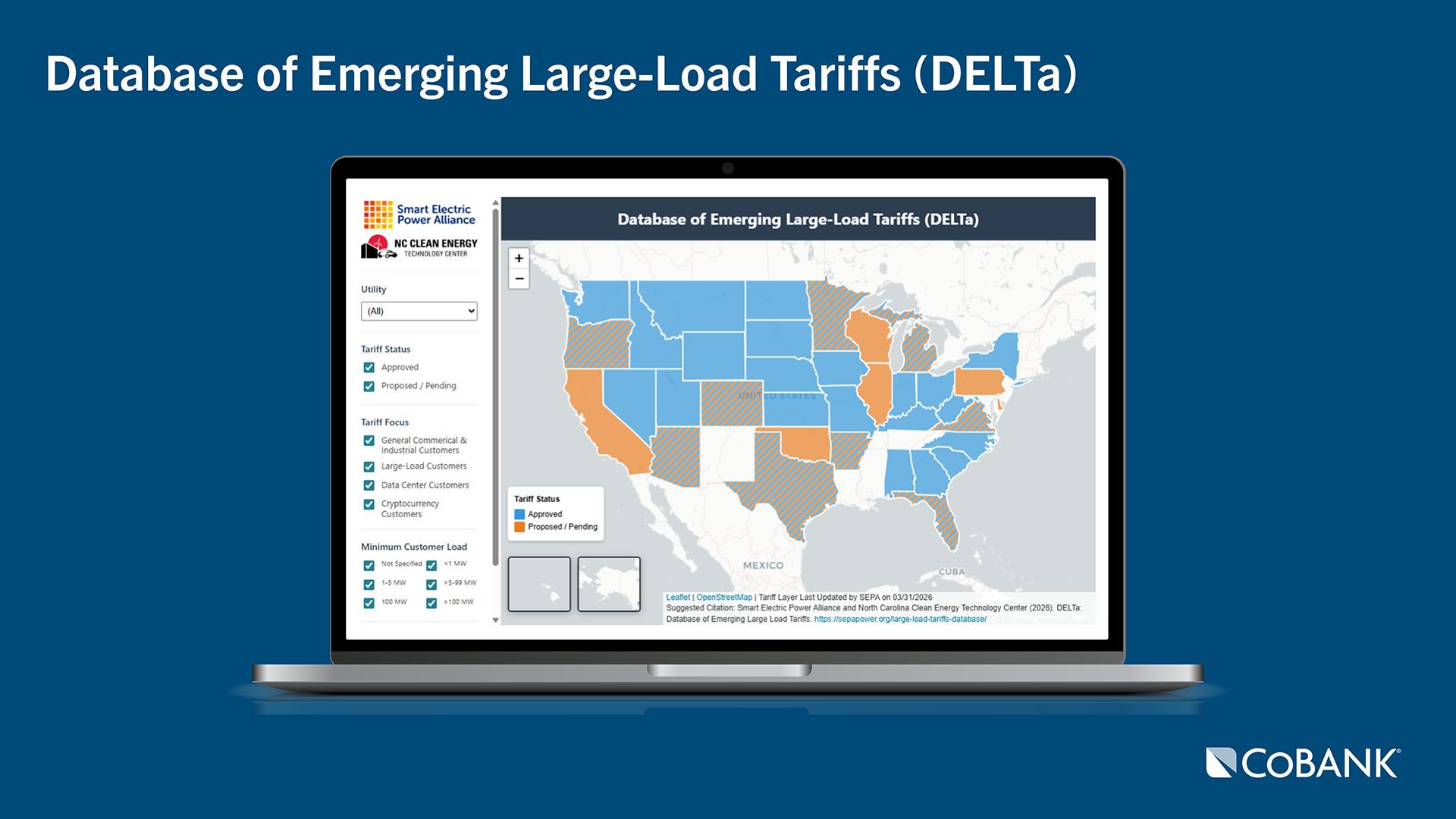

- To capture and assess emerging approaches to large-load electric service rates in the U.S., the Smart Electric Power Alliance and North Carolina Clean Energy Technology Center created the Database of Emerging Large-Load Tariffs (DELTa).

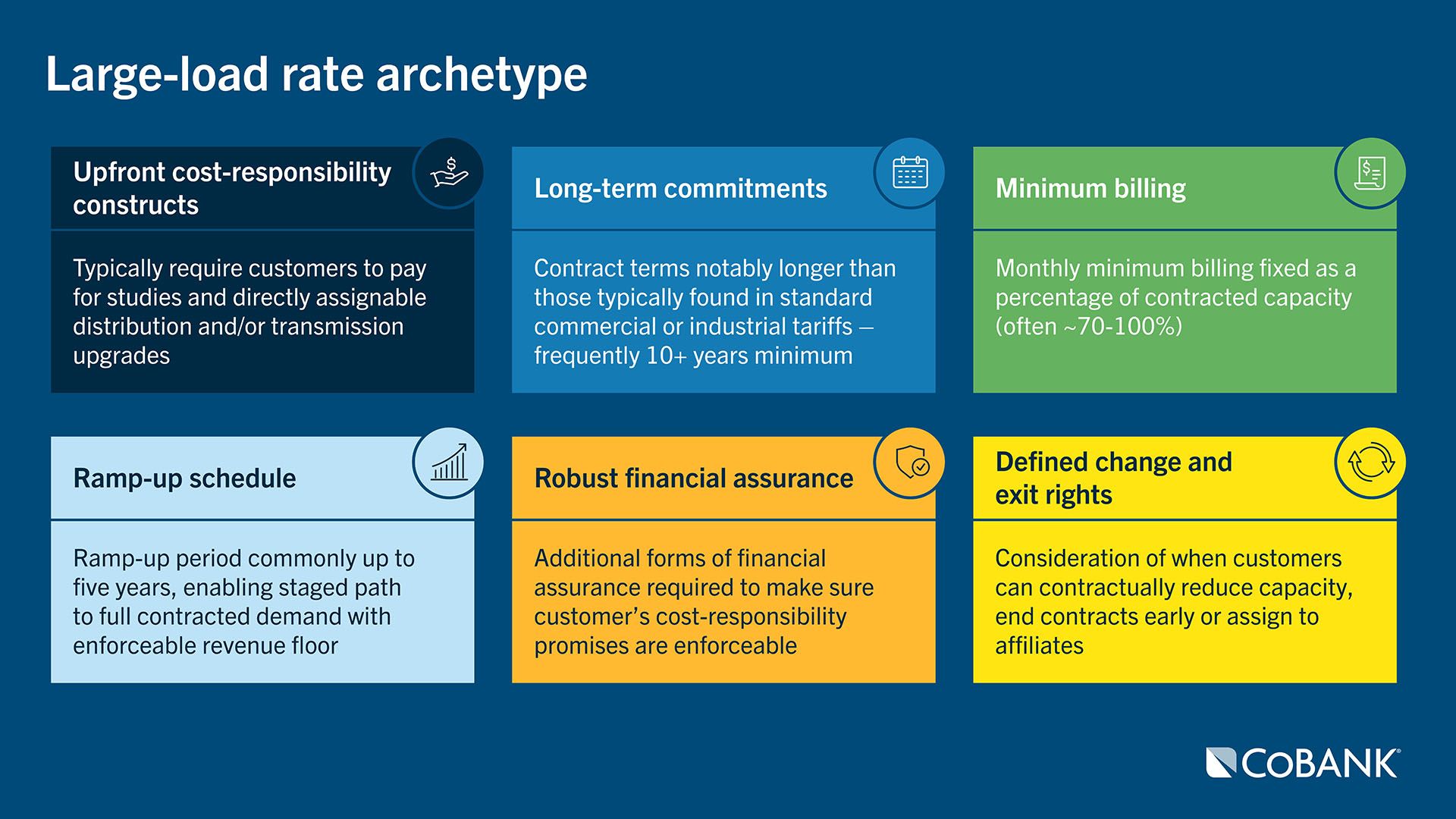

- A recognizable “large-load rate archetype” is emerging across recent filings captured in DELTa, providing a repeatable default blueprint for serving very large customers. They blend three core objectives: assign incremental costs to the requested load to prevent cost shifting, implement long contract terms and minimum bills to reduce stranded-asset exposure, and define credit, collateral, and change/exit rules to strengthen enforceability.

We extend our gratitude to Ann Collier of SEPA and Justin Lindemann of NCCETC for their continued dedication to creating the DELTa public resource and their thoughtful leadership illuminating utility rate-setting initiatives in this space.

Why “large-load loss” risk is back on the table

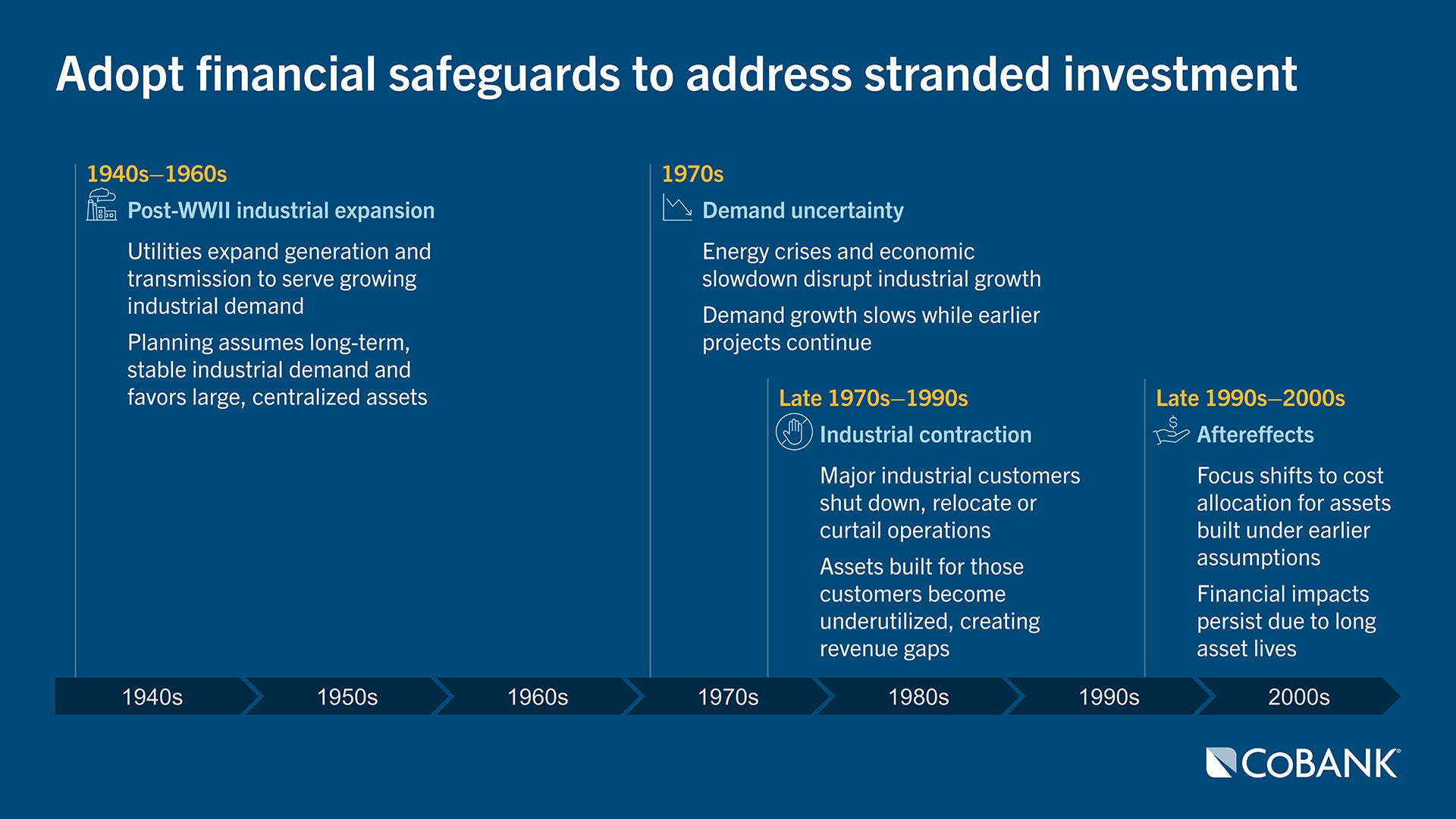

Utilities have long understood that a single large commercial or industrial facility can materially shape a local grid’s cost structure. Historically, when large manufacturers expanded, utilities often built dedicated substations, line extensions, and upstream capacity sized to a single customer’s forecasted demand. These large loads did not often make upfront grid investments, rather the utilities made the investments in anticipation of load growth, with costs recovered through volumetric-based rates. Following the wave of post-World War II development, however, major industrial customers shut down or relocated in the 1970s, 80s and 90s, leaving utilities with underutilized “single purpose” assets and multi-year revenue gaps. Those stranded costs were frequently socialized through general rates, shifting the burden onto remaining customers which were often residential and small-business consumers.

Every region of the country has examples — paper and pulp mill contractions in the Pacific Northwest, automotive plant closures across parts of the Midwest, and textile industry offshoring in the Southeast. In each case, the combination of large, discrete load losses and long-lived grid investments created utility write-offs and difficult cost-allocation debates. In the early 1990s, rate design shifted more explicitly toward cost-causation largely in response to this dilemma. It was felt that customers, or rather customer classes, should pay in proportion to the costs they create and/or the benefits they receive. This shift in the collective utility mindset was driven by concerns that older allocation methods were cross-subsidizing certain classes, often leaving residential and small commercial customers paying more than their “fair share.”

A concrete marker of that advancement was the 1992 publication of Electric Utility Cost Allocation Manual by the National Association of Regulatory Utility Commissioners, which established guidelines for allocating costs based on how they were incurred and who benefited. It is safe to say that the precursor Bonbright Principles provided the enduring North Star for ratemaking — fairness, avoidance of undue discrimination, and practical workability — while NARUC’s work translated those goals into a more explicit cost-causation framework for assigning utility costs to the customers who drive them. Now, as new large loads re-emerge, utilities and regulators are increasingly revisiting how to interpret “cost responsibility.”

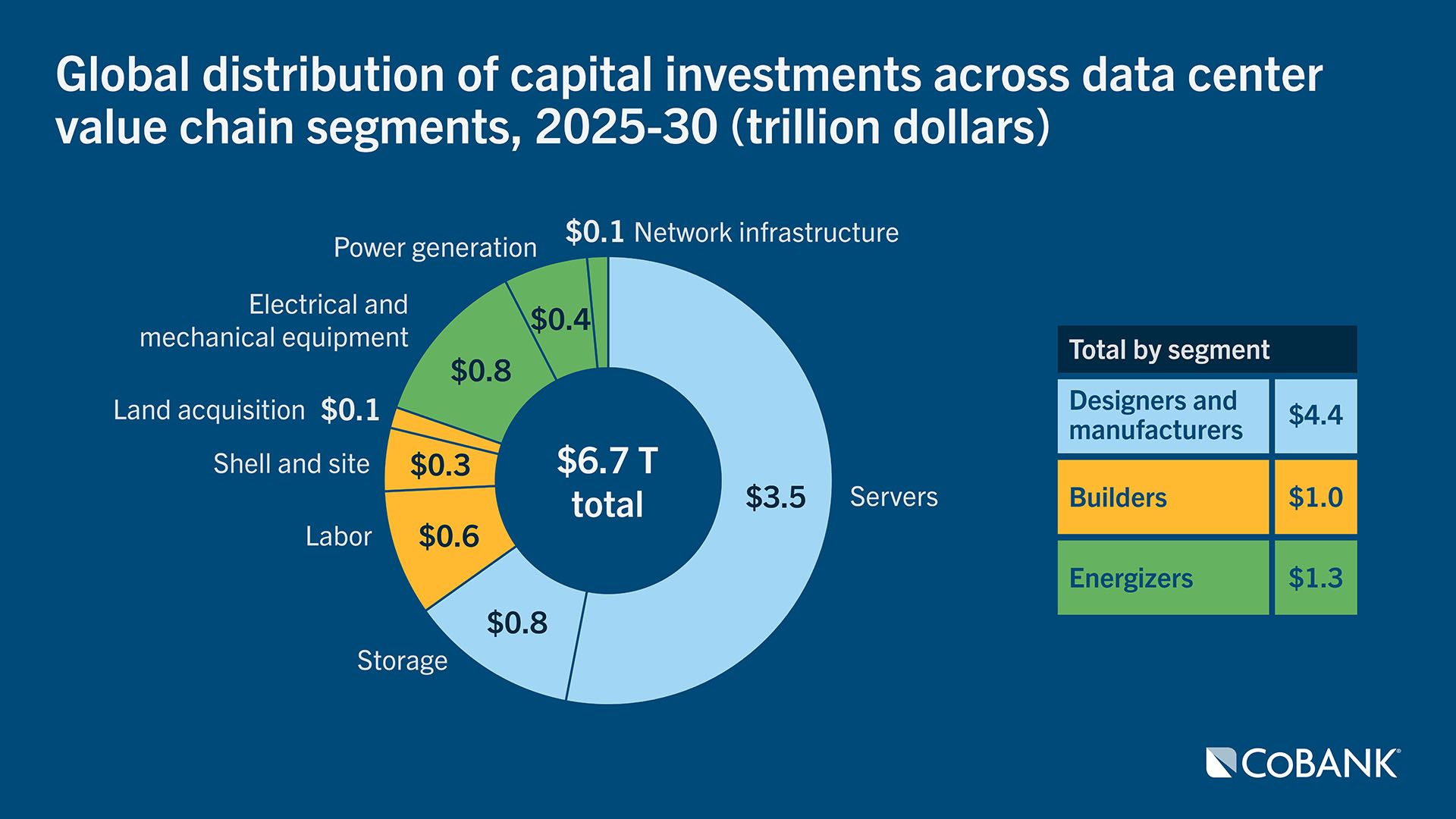

Significant community advantages may arise from load growth and investments in the grid, potentially stabilizing or even reducing current electricity bills. However, achieving these outcomes requires careful cost allocation and thoughtfully designed rate structures. Additionally, concerns regarding the potential loss of these loads are well-founded. According to McKinsey, nearly $7 trillion will be invested globally in data center infrastructure by 2030, with approximately 65% allocated to servers and storage, or equipment that can be readily relocated should market conditions decline or industry consolidation occur. Consequently, the rapid deployment and “optionality” or mobility of that investment speaks volumes about the importance of this discussion.

Based on our analysis, we can see an archetype for large load rates emerge as stakeholders are increasingly focused on designing tariffs and contract frameworks that (1) align infrastructure and power-supply costs with the customers that cause them, (2) ensure adequate credit support for multi-year obligations, and (3) define clear exit and change rules to prevent repeat episodes of stranded investment.

In other words, these policies ensure loads are integrated into the system in a manner that is operationally feasible, financially sustainable, and equitable for all customers.

Beyond the current prototype, significant advancements are emerging that are poised to influence the future of large load design. Many of these rate innovations target upstream cost allocation, which until now has largely been socialized amongst ratepayers. Accordingly, it will be valuable to review this subject periodically as more refined policy approaches are introduced.

DELTa: What it is and why it was created

DELTa (the Database of Emerging Large-Load Tariffs) is a public resource maintained by the Smart Electric Power Alliance (SEPA) and North Carolina Clean Energy Technology Center (NCCETC) that aggregates and summarizes pending, approved and effective utility tariffs and related rules designed for large-load customers. DELTa is intended to make it easier for stakeholders to compare how electric utilities are defining “large load,” what financial protections are being adopted to prevent cost-shifting and which mechanisms are being tested to manage “speed to power” and operational risks. The database now tracks a sharp rise in large load tariffs, with 20 approved in 2024 and 53 proposed or approved for 2025 — up from just 14 between 2018 and 2024. This reflects a significant inflection point in utility rate design amidst the data center boom.

The database records key “guardrail” elements for consideration, including minimum contract and revenue requirements along with other financial assurances. It also includes standardized provisions that regulate contract modification, exit procedures and security release. In practice, these provisions can be as consequential as the rate level itself because they determine who bears the risk of project delay, downsizing or early departure.

The emerging large-load rate archetype

Across recent filings captured in DELTa, a recognizable “large-load rate archetype” is emerging. While specific provisions vary by state and utility, many new tariffs and service rules blend three core objectives: (1) prevent cost shifting or socialized cost structures by assigning incremental costs to the requesting load, (2) reduce stranded-asset exposure through long contract terms and minimum bills, and (3) strengthen enforceability through credit, collateral and defined change/exit rules.

Many recent rate proposals are driven by new data centers, which require large, reliable and quickly scalable power. Meeting these needs often demands specialized infrastructure and significant upgrades, which can become difficult to repurpose should demand fall or shift unexpectedly. In response, utilities have established distinct customer classes and tailored tariffs to more accurately allocate costs to these high-density loads.

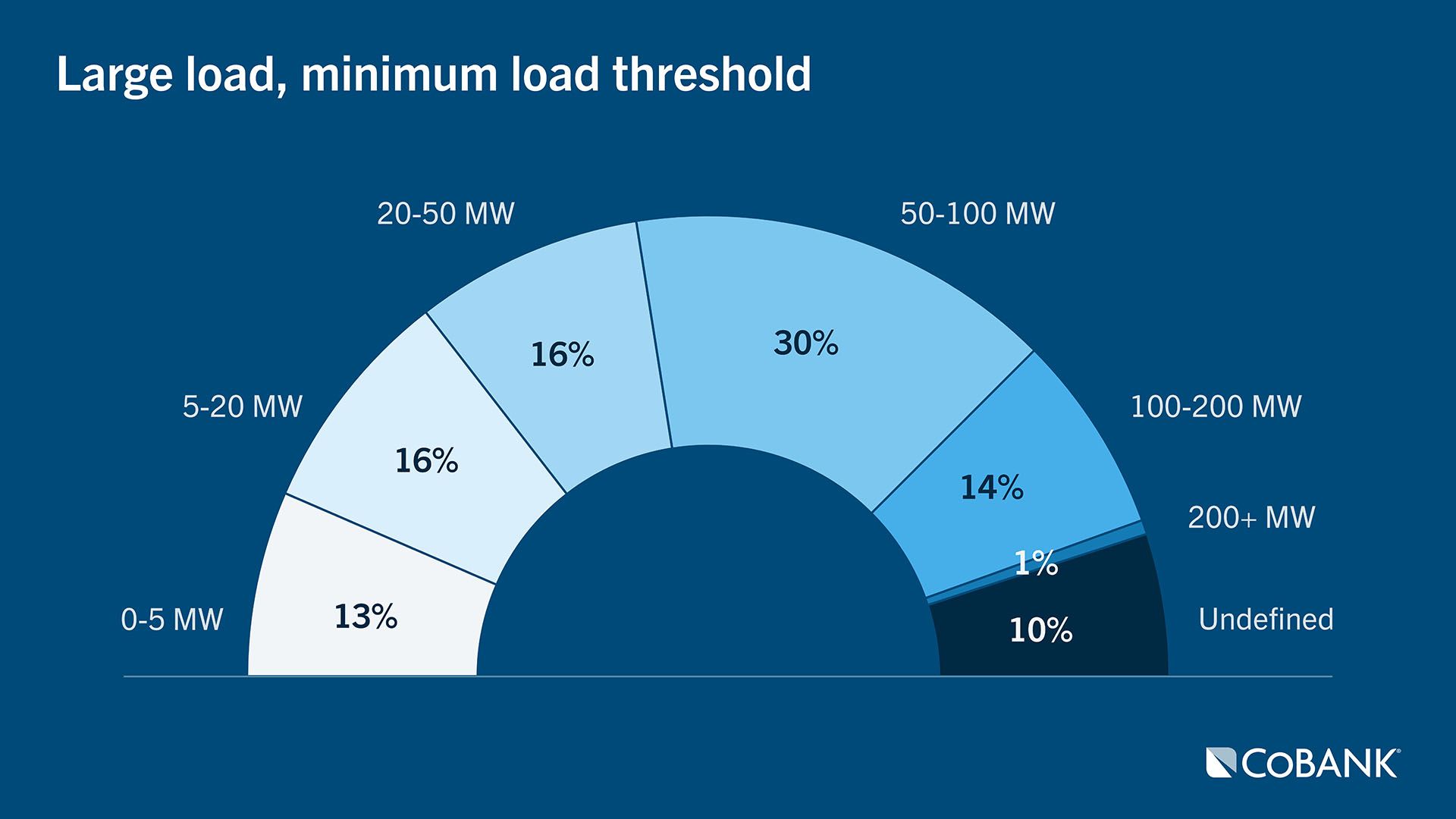

As a starting point, the defining feature of the emerging large-load rate archetype is the use of eligibility screens based on objective, quantifiable criteria. Utilities typically establish minimum demand thresholds — often ranging from 1 megawatt to as high as 500 MW, with an average around 50 MW, with nearly three-quarters of the tariffs targeting customers with loads above 20 MW. These thresholds are set with consideration for the size of anticipated loads relative to existing customers, aggregate impacts on system peak demand and the unique risk profiles.

In its petition to the Illinois Commerce Commission, Commonwealth Edison Company justified threshold criteria of 50 MW highlighting, “generally, loads below 50 MW can be served through the extension of multiple distribution circuits at 12 kV or 34 kV. Loads of 50 MW or more are generally served at high voltage – 138 kV or greater. These loads, whether the equipment serving them is functionalized as high voltage distribution or transmission, require specific evaluation to understand the impact on the transmission system. Therefore, ComEd proposes to set 50 MW as the delineation for when a project is studied in the cluster approach.”

While some proposals have experimented with industry-specific classifications, such as for mobile data centers or cryptocurrency mining, most approved tariffs remain “industry-neutral” to ensure compliance with state statutes and to avoid concerns over undue discrimination.

In about 15%-20% of filed tariffs, large loads must also meet a high-density requirement, typically with a minimum load factor of 75%-85%. The addition of a high load-factor screen helps utilities and regulatory commissions distinguish steady, “always-on” loads from more peaky or variable loads. This in turn helps establish a benchmark for reserve capacity.

Tariff language serves as the fundamental tool through which utility governance is established, essential service objectives are realized, and cost-allocation fairness is achieved. By articulating precise criteria and requirements, these provisions shape the structure of large-load rates, guiding how costs are assigned, risks managed, and operational responsibilities enforced.

Among DELTa records, the following large-load rate archetype is emerging:

- Cost-of-service studies, CIAC and other upfront cost-responsibility constructs: These provisions typically require customers to pay for upfront administrative expenses, cost-of-service studies and directly assignable distribution and/or transmission upgrades. From a strategic perspective, these initial, upfront financial responsibilities have significantly altered the nature of low barriers to entry and the “first-come, first-served” approach by introducing specific criteria that govern access. About 40% of DELTa-tracked large-load tariffs explicitly require the customer to pay utility study costs and reference of Contribution in Aid of Construction (CIAC) or upfront payments for infrastructure upgrades. Examples include Rappahannock Electric Cooperative and the New York Municipal Power Agency (page 97). For the New York Municipal Power Agency, the “reasonable costs of conducting the feasibility study and the entire cost of any new facilities necessary to supply the requested service will be paid by the customer. At the end of each full year of service, for the first ten years, the customer will receive a refund equal to the lesser of the annual non-supply-related revenues from the customer, or one-tenth of the cost contribution paid by the customer.” Yet, refunds of CIAC payments for large load substations and equipment are not common and are generally non-refundable under standard utility policies unless specific, rigorous criteria regarding future usage or regulatory intervention are met. Further, utilities rarely specify a fixed dollar amount for cost-of-service study fees in their tariff language. Instead they commonly require the customer to reimburse the utility for the study’s actual costs (often with amounts later set through a separate agreement), with a notable exception in AEP Ohio’s Data Center Tariff settlement, which specifies tiered study fees of $10,000 / $50,000 / $100,000 based on the size of the capacity request.

- Long-term commitments: These contract terms for large-load customers are notably longer than those typically found in standard commercial or industrial tariffs. While traditional commercial and industrial agreements often range from one to three years, the emerging large-load rate archetype frequently requires minimum terms of 10 years or longer, such as PPL Utilities’ Schedule LP-6with a 10-year minimum term and Xcel Energy with a 15-year term. The longest minimum contract term in the DELTa-tracked large-load tariffs is 20 years, used by Florida Power & Light (FPL) and also by Kentucky Power. We observed that Georgia Power was granted the flexibility of imposing longer contract terms than are stated in the large-load customer's applicable tariff at its discretion. Extended contract durations in large load tariffs help reduce stranded asset risks by directly aligning contract terms with the life of infrastructure assets (power plants, transmission and substations) and support cost recovery for major infrastructure investments in high-density loads.

- Minimum billing: Commonly minimum-billing or “take‑or‑pay” provisions are showing up in large load tariffs, with the customer’s monthly billing fixed as a percentage of contracted load (often ~70–100%) regardless of actual usage. These requirements establish a predictable revenue floor for the utility. In the DELTa March 31, 2026, public update, 33 of 77 filings had numeric minimum-bill requirements, with the average term ~80% of contracted capacity. Lesser used alternatives include establishing the minimum based on the customer’s historical peak or a fixed floor. Examples include: Michigan’s Consumers Energy, which sets a minimum monthly billing demand at 80% of contract capacity for large loads, and Kentucky Power, which requires at least 90% of the customer’s contract or peak demand benchmark. Indiana Michigan Power’s tariff is somewhat of a hybrid, setting the minimum monthly billing demand as the greater of 80% of the capacity contracted by the customer, or 80% of the customer’s highest monthly demand over the prior 11 months. Tri-State establishes both a minimum demand as well as a minimum energy billing component, to “cover expenses associated with the resource and transmission builds or procurements.”

- Ramp-up schedule: Ramp-up periods are common for large load customers because these facilities typically increase their demand in phases, and accommodating this gradual growth in utility planning ensures that infrastructure investments and resource allocations align with the actual pace of customer expansion, reducing the risk of overbuilding or underutilizing assets. The most common ramp-up period specified in large-load tariffs is up to five years (often framed as “up to 5 years” or “5 years max”) and enables utilities to have a staged path to full contracted demand while still providing an enforceable revenue floor (often through step-down or step-up minimum billing demand terms). An example is Pennsylvania’s PPL Utilities’ Schedule LP-6(see page 28) where the first five years of the 10-year contract term allow the load to ramp up to full capacity. PPL’s tariff stipulates that until the costs of system upgrades needed to serve the customer are satisfied, the customer shall pay applicable rates based on the greater of actual peak demand values or 80% of the load provided in the load ramp schedule. Tri-State took a very different approach for its first Federal Energy Regulatory Commission (FERC) tariff filing by requiring the initial load projections to stay within a 5% tolerance for each of the next three years, ensuring better resource planning accuracy. The ramp-up schedule may be integrated into the three-year projections, with strict adherence to defined tolerance bands. A significant deviation in load requirements would result in a financial responsibility for the customer.

- Robust financial assurance (letters of credit, parent guarantees, deposits, collateral “true-ups,” and security release provisions): Large-load tariffs increasingly require additional forms of financial assurance to make sure the customer’s cost-responsibility promises are enforceable. In fact, 44 of the 77 filings include additional collateral requirements. In testimony provided by Dominion to its state regulatory authority, the first goal of developing a large load tariff is to ensure that the customer pays rates that align their cost causation. The second goal is to mitigate the risk of unrecovered costs. Dominion requires customers to post $1.5 million per megawatt in collateral for the 14-year contract. Those with an acceptable credit rating, or a parental guarantee from a qualified affiliate, can be exempt from up to 70% of this requirement. The form of collateral may be in the form of a parental guaranty, irrevocable letter of credit, surety bond or cash.

- Defined change/exit rights: Regulators frequently consider when large load customers can contractually reduce capacity, end contracts early or assign them to affiliates. These rules are vital for limiting stranded-asset risk and ensuring utilities can recover costs when customers’ needs change. In approving Consumer Energy’s application to amend the terms and conditions under which it serves data centers, Michigan Public Service Commission specifically required, “a default collateral requirement that’s equal to half of a large-load customer’s exit fee, to ensure that the customer can and will pay the exit fee. The collateral requirement will be reduced over the course of the large-load user’s contract.” DELTa notes many filings now include a “change band” (often about 20% of contracted demand), allowing load reduction with notice before exit fees apply. If reductions exceed this band, customers may face fees covering unrecovered fixed costs and minimum-bill obligations. For example, in West Virginia, Appalachian Power and Wheeling Power allow customers to reduce their contract capacity by up to 20% after an initial period with proper notice; however, larger reductions or contract terminations require both advanced notice and the payment of exit fees. Similarly, Indiana Michigan Power in Indiana requires contracts to be at least 12 years in length with collateral, permitting reductions above specified thresholds only if commission-approved exit fees are paid. In Pennsylvania, PPL Utilities links exit fees to minimum-load and security obligations, ensuring that termination charges are directly tied to risk mitigation measures. Assignability is less formalized, often managed in service agreements and requiring utility approval, credit checks, and assumption of payment obligations. Strong assignment provisions help manage stranded-cost risks by facilitating contract transfers while maintaining utility protections.

Latest “guardrail” rate design trends

In addition to the more common features now found in large load tariffs and identified in DELTa’s “Select Tariff Characteristics,” some utilities are also testing new approaches that tie large-load billing more closely to marginal system costs and reliability requirements. Three notable, emerging themes are (1) separating and passing through power-supply and transmission costs that are driven by the large load (sometimes through a "bring your own generation" provision), (2) charging a marginal cost adder and (3) integrating curtailment or interruptibility so that certain loads can be reduced during stressed grid conditions, potentially enabling faster interconnection or reducing the need for some upstream investment.

At their core these new developments are structured in a manner that will ensure large-load customers bear incremental costs, with the intention of stabilizing or reducing the future financial burden for existing customers:

- Creating pass-through structures for upstream costs: At present, distribution utilities in deregulated markets are electing to allocate upstream transmission and generation costs by passing these costs directly to large loads either by creating stand-alone supply entities or soon by leveraging new regional pricing transfer mechanisms. For instance, Rappahannock Electric Cooperative’s data center agreements (see the REC case study) secure capacity and energy through an unbundled PJM market-based rate in a separate power supply agreement, rather than using a portfolio or embedded supply approach. Similarly, Southwest Arkansas Electric Cooperative Corporation’s (SWAECC) proposed tariff requires its own cost of energy rider, so that “any change in the price of energy paid by SWAECC will be passed through at the correct rate to the members taking service under this tariff.” Upcoming upstream cost mechanisms could simplify this process with several Independent System Operators and Regional Transmission Organizations currently refining their commercial pricing and interconnection frameworks to isolate the costs of large loads. For instance, MISO is evaluating the creation of biddable pricing points at large load interconnections to allow for better hedging of congestion impacts, while PJM has established an Expedited Interconnection Track to integrate generation paired with rapid data center growth. Similarly, SPP and CAISO have launched specialized initiatives like the High Impact Large Load process to enhance price signals and address the specific network upgrades triggered by these facilities. ERCOT is also revising its nodal-based interconnection studies to manage a massive queue driven primarily by the tech sector. These developments aim to isolate infrastructure costs, manage shifting congestion through Locational Marginal Pricing, and mitigate the risk of stranded assets. This regional movement is further supported by recent federal action, such as the FERC Advance Notice of Proposed Rulemaking issued in January 2026, which seeks to standardize how these interconnections and their associated costs are handled across the national transmission system.

- Leaning into vertical integration to assign upstream costs: Dominion Energy Virginia will implement the GS-5 rate class, a specialized tariff approved by the Virginia State Corporation Commission to take effect in January 2027 to assign upstream costs directly to large loads (≥25 MW) through a “take-or-pay” mechanism that requires customers to pay for a minimum of 85% of their contracted transmission and distribution capacity and 60% of their generation demand, regardless of actual usage. FPL’s introduction of a new charge — the Incremental Generation Charge — designed to ensure that the costs for the incremental generation necessary to serve these new large loads are recovered from the data center customer and not from FPL’s general body of customers. Likewise, Entergy Louisiana uses an Additional Facilities Charge to recover infrastructure costs for large-load customers, including data centers.

- Inter-service territory or zonal rate structure: Acknowledging that different areas of their service territory impose very different delivery costs upon the utility, FPL has introduced a two-part tariff for large loads. The LLCS-1 tariff allows for up to 3 gigawatts of combined load (cap); limits service to three areas (St. Lucie, Martin, and Palm Beach counties) chosen for their proximity to FPL’s 500 kW transmission lines and suitability for incremental generation; and contains an incremental generation charge, which is based on the annual revenue requirement for the incremental generation capacity that can serve 3 GW of additional load. The LLCS-2 tariff is available to customers outside the three designated LLCS-1 zones, contains no 3 GW load cap, and contains a revenue requirement formula for the incremental generation/transmission capacity charge.

- BYOG becomes mainstream: Utilities are increasingly adopting “bring your own generation” or “clean transition” frameworks within large load tariffs to accommodate the massive power needs of data centers while protecting other ratepayers from infrastructure costs. These mechanisms allow large-scale users to directly fund or contract for specific system resources that operate alongside standard utility planning to accelerate interconnection. Earlier development of customer clean energy self-supply programs has bridged the gap between utility capacity constraints and corporate sustainability goals by shifting the financial and operational responsibility of new power generation onto the customer. These programs allow large loads to bypass traditional utility “all-requirements” structures. For example, Georgia Power allows large loads to identify and commit to paying for their own power supply projects, through a new customer-identified resource provision (CIR). Georgia Power customers who submit a CIR through the utility’s Clean And Renewable Energy Subscription program negotiate directly with a project developer to submit a bid that provides the same or better total net benefits as the initial portfolio average. Tri-State launched the Bring Your Own Resources program before its large load rate design initiative, providing a route for self-supply options for large loads.

- Marginal-cost capacity pricing: Evergy’s Large Load Power Service tariff includes a marginal cost adder designed to ensure that the high incremental costs of serving new or expanding loads of 75 MW or more are not shifted to existing customers. This mechanism requires large-scale users to pay for capacity based on the cost of new infrastructure rather than lower, system-wide average costs, aiming to provide a net benefit to the grid. Kansas Corporation Commission staff estimates that customers using the large load rate will pay 7% to 10% more than existing industrial customers, according to the commission’s order.

- Interruptible service provisions: From a system-planning perspective, interruptible or “curtailment-enabled” large loads can create planning headroom. The tradeoff is that these structures require clear measurement and enforcement (including penalties for failure to curtail), and they may be better suited to loads whose processes can tolerate interruption (or that can self-supply behind the meter) than to fully firm, mission-critical operations. Utilities are increasingly embedding interruptible provisions into large load tariffs, using diverse mechanisms to ensure grid stability. Idaho Power employs a prescriptive model, allowing remote disconnection for up to 225 hours during summer peaks. AEP Ohio implements a technical contingency, mandating that large loads with onsite generation provide instantaneous curtailment synced to their local power output. Entergy Arkansas requires Large Power High Load Density customers to enter into a customer service agreement for interruptible service as part of the tariff. Maximum interruptions range from 10-20 events per year depending on curtailment notice time. Whereas Chelan County PUD’s Rate Schedule 36 pairs service-interruption provisions with broader operational controls.

Taken together, these emerging practices underscore that the utility framework for large-load tariffs is still evolving, as regulators and utilities iterate toward clearer alignment between total cost causation and enforceable risk allocation. Readers should expect the next wave of filings to further standardize “failure-to-perform” protections—such as tighter milestone and in-service deadlines, more explicit ramp and change-band rules, and increasingly formulaic exit-fee and security-release schedules. We also anticipate broader use of upstream cost pass-throughs (including component-level minimum bills), curtailment-for-speed-to-power options, and BYOG-style constructs that require customers to procure or fund incremental generation and transmission solutions outside of the utility’s embedded portfolio.

Rate-making becomes crowded as regulators increase oversight

Amidst a relatively contentious and prolonged large-load tariff proceeding — in which “dueling settlements” were filed just weeks apart — an executive at AEP Ohio felt the need to remind the industry that utilities have traditionally “owned” the ratemaking process as part of the well-worn regulatory compact. The rise of hyperscale data centers, however, might be disrupting that convention. These large customers have made their expectations explicit — especially regarding pricing and expedited service — shifting leverage toward a small group of high-demand users and attracting heightened regulatory scrutiny.

At the same time, governments are stepping in to address perceived gaps, particularly around affordability, flexibility and energy sourcing. These interventions reflect different institutional priorities and have introduced measures such as new customer classes, “good neighbor” provisions that channel economic benefits to low-income communities or other rate classes, and standardized or model tariffs that may override existing utility frameworks. This growing involvement reflects a broader policy lens. Regulators are focusing on issues utilities may not prioritize, including consumer protections, clean energy targets, and system flexibility. States like Texas, Virginia, Minnesota, and Pennsylvania are leading this shift with clearer cost-allocation rules. The result is an increasingly fragmented landscape, ranging from local ordinances that impose stricter requirements on large loads like data centers, to broader policy efforts that frame impacts in terms of household costs rather than traditional ratepayer metrics.

Pennsylvania, for example, has a model tariff for customers at or over 50 MW individually or 100 MW in the aggregate (“large load customer”), which serves as a template framework for how an electric distribution company could structure eligibility, cost-responsibility and risk-mitigation terms for very large new loads. In practice, the model tariff signals a policy preference for (1) assigning directly attributable distribution upgrades, interconnection and study costs to the large-load customer, (2) requiring enforceable long-term commitments (often paired with minimum-bill or take-or-pay constructs) to limit stranded-asset exposure, and (3) establishing clear credit and security requirements and defined change/exit rules before service is initiated.

The model also includes a “good neighbor” requirement that large load customers make an annual contribution to the applicable utility's hardship fund — supporting grants to help customers pay their utility bills — based on peak demand, with contributions ranging from $250,000 for those with a peak demand of at least 25 MW but less than 75 MW, to $1 million for those with a peak demand of at least 500 MW. Customers who bring their own onsite generation and are not using their full interconnection limits may also be offered lower minimum demand and/or standby charges. While Pennsylvania utilities are not required to mirror the model in every detail, it can carry significant persuasive weight as a “regulatory safe harbor” when utilities evaluate tariff design options—i.e., provisions that align with the model may be viewed as more readily defensible on cost-causation and consumer-protection grounds, whereas departures may require stronger utility-specific justification in commission proceedings.

| State | Status | Legislation summary | Timing |

|---|---|---|---|

| Maryland | Passed | The Utility RELIEF Act requires data centers to pay for their own energy infrastructure upgrades and grid connections. It also incentivizes “Bring Your Own Clean Energy” policies, allowing data centers to jump ahead in the interconnection queue if they provide their own power. | Apr‑26 |

| Utah | Passed | S.B. 132 allows utilities to require facilities expected to reach 100 MW to seek their own energy supply if the utility cannot serve them without major, expensive system upgrades. | Mar‑25 |

| Oregon | Passed | The Oregon POWER Act forces data centers and large energy users (>20 MW) to pay for their own infrastructure upgrades and sets higher electric rates to protect consumers. It requires a new, separate customer class for these facilities and mandates 10‑year service contracts, limiting rate increases on households. | Jun‑25 |

| Texas | Passed | Texas SB 6 (2025) mandates that new large loads (≥75 MW) interconnected after December 31, 2025, comply with mandatory, ERCOT‑directed curtailment during emergency conditions. The law requires these customers to pay for transmission studies (min. $100k) and infrastructure upgrades, while establishing a voluntary, compensated demand-response program. | Jun‑25 |

| Georgia | Failed | Georgia Senate Bill 34 (SB 34), introduced in the 2026 session, aims to protect residential and small business customers from bearing the energy infrastructure costs associated with the rapid growth of data centers. It seeks to ensure that utilities cannot pass on expenses from data center power consumption, such as new power plant construction and transmission lines, to consumers. | Feb‑26 |

| Illinois | Pending | The Protecting Our Water, Energy, and Ratepayers (POWER) Act (SB4016/HB5513) aims to regulate Illinois data centers, requiring them to use renewable energy, pay for their own grid infrastructure and manage water usage. It forces "bring your own new clean energy" (BYONCCE) plans and protects consumers from rate hikes. | Feb‑26 |

| Oklahoma | Pending | Ratepayer Protection Act (HB 2992) aims to prevent residential and commercial ratepayers from subsidizing infrastructure costs for new high‑demand data centers, AI, and crypto‑mining facilities. It mandates that "large load" customers (75+ MW) pay for their own grid upgrades, creating dedicated, separate utility tariffs to protect existing consumer rates. | Mar‑26 |

| California | Pending | Senate Bill 886 (SB886), the "California Technology Innovation and Ratepayer Protection Act" aims to protect ratepayers from high energy costs and ensure environmental sustainability by requiring data centers to prefund energy infrastructure, use clean power, and follow stricter sustainability standards. | Apr‑26 |

| Pennsylvania | Proposed | Pennsylvania lawmakers are introducing legislation, specifically HB 1834 and SB 724 (Data Center Fair Share Act), to protect consumers from rising electricity costs, grid instability and environmental impacts caused by the surge of data centers. These initiatives aim to prevent utility companies from passing infrastructure costs onto residential ratepayers and require data centers to report energy/water usage. | Apr‑26 |

| Kentucky | Failed | HB 544: Attempted to mandate that shared facility costs result in zero adverse impact on other classes. | Apr‑26 |

At the federal level, oversight is also expanding. The Department of Energy’s Advanced Notice of Proposed Rulemaking (ANOPR) proposes extending federal authority over large-load interconnections—an area historically governed by states. The goal is to improve consistency and transparency, particularly for projects that cross state lines, and to clarify responsibilities for interconnection and network upgrade costs. This move reflects concerns that rapid large-load growth could create reliability risks and increase costs across regions. FERC is expected to take action on the ANOPR by June 2026, consistent with the federal timeline that DOE set for moving from concept to enforceable interconnection reforms. FERC’s action could include issuing a Notice of Proposed Rulemaking (NOPR) or an other order that advances a standardized set of procedures and cost-allocation rules for large-load interconnections.

Taken together, these developments mark a turning point where large loads are no longer viewed solely as engines of local economic development, but also as potential drivers of significant system costs and reliability risk. As a result, regulators are increasingly reframing large-load rate design as a consumer-protection and long-term planning exercise. In effect, the center of gravity is shifting from utility-led, deal-specific negotiation toward commission-designed default terms that establish baseline protections and allocate risk before projects move forward. That shift suggests future tariff structures may embed more direct regulatory oversight and control through standardized “guardrails” (e.g., prescribed cost-responsibility rules, minimum commitments, collateral and credit requirements, milestone enforcement, and formulaic exit provisions). These guardrails reduce the degree to which outcomes are set exclusively through utility-led filings or bespoke negotiations and make commissions a more active architect of the terms under which large loads connect and remain on the system.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.