Inflation, federal debt and AI buildout drive interest rates higher for longer

Key points

- Rates have reset higher as inflation, debt issuance and deficit concerns converge.

- The Fed is unlikely to cut rates while inflation remains above target and growth stays firm.

- The Fed’s posture has also unexpectedly become more hawkish under Chair Warsh, raising risks that long-term yields stay elevated.

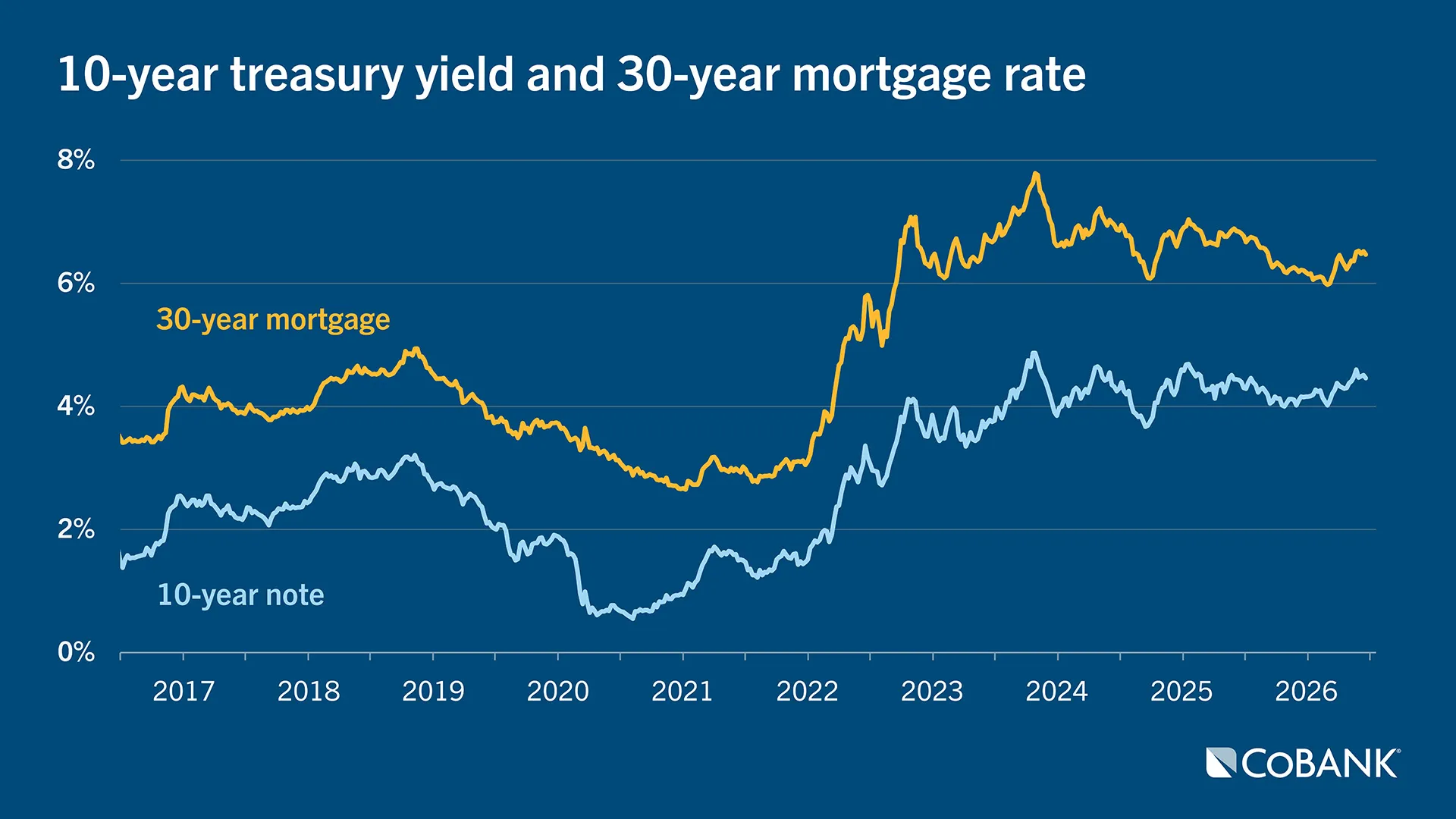

Interest rates, along with forward rate expectations, have moved meaningfully higher since early March, reflecting a convergence of inflationary pressures, geopolitical shocks, expanding corporate debt issuance, worsening federal deficits and shifting views on Federal Reserve priorities. When the year began, the consensus expectation was for a “gradual easing.” That has evolved into a collective “higher-for-longer” view.

The initial trigger was the outbreak of the Iran war in late February: It disrupted global oil supply chains and pushed crude and gasoline prices sharply higher, which fed directly into U.S. inflation metrics. But more recent inflation reports are showing broad-based price pressures, not just in energy, but in services and housing, suggesting inflation is more entrenched than policymakers had thought. Conservative estimates put the war and supply replenishment costs at around $100 billion. That will have to come through increased deficit spending, which will increase the supply of debt on the market.

Strong growth and AI investment reduce odds of Fed cuts

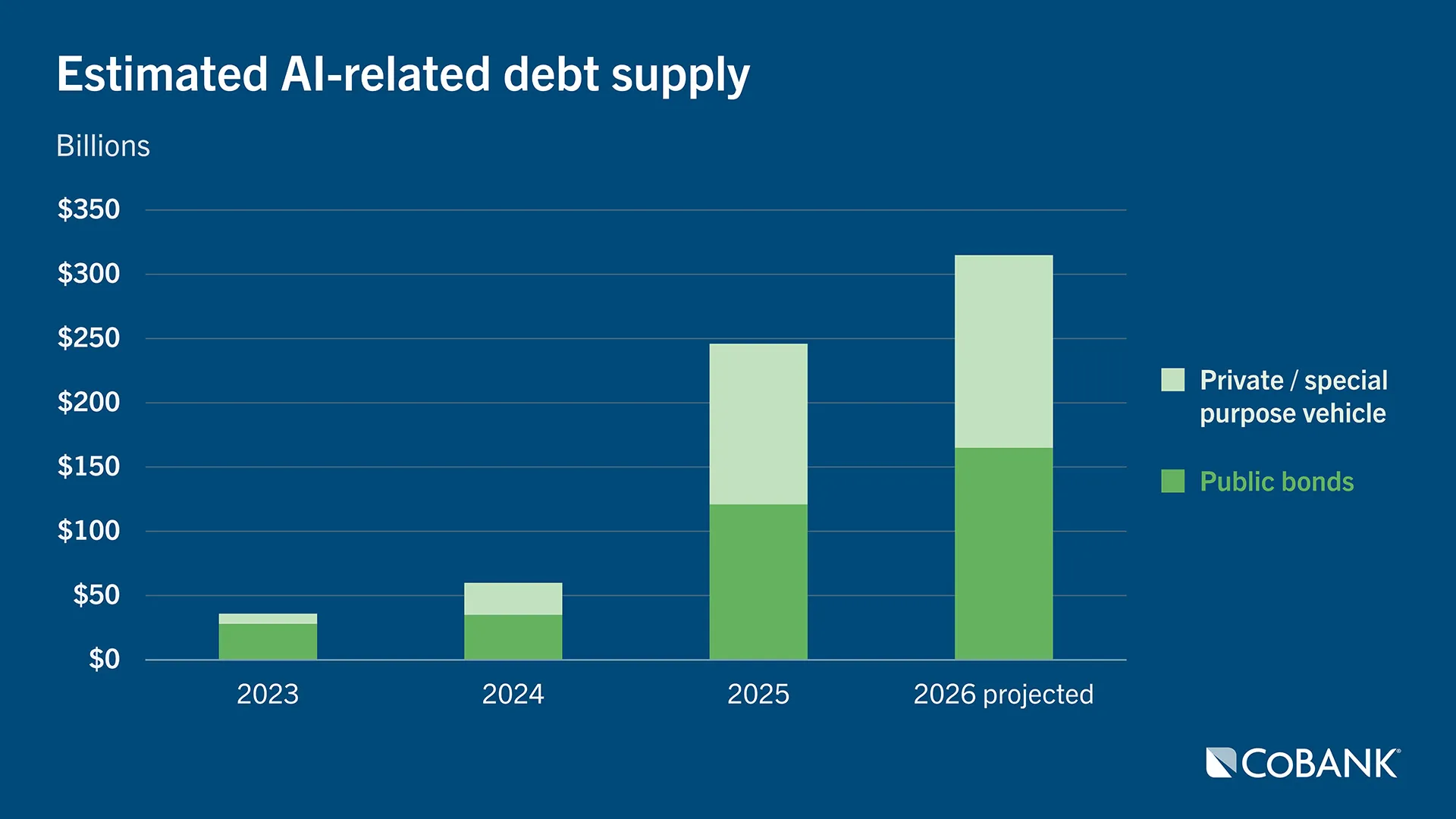

Concurrently to the war, other economic data has surprised to the upside over the past three months, particularly consumer spending, payroll additions, and non-residential investment (primarily AI/technology related). AI-related debt (public and private) has exploded to an estimated $315 billion in 2026 from only $60 billion two years ago. While it is not our view, some suggest that the economy could be at risk of overheating. Combine all the above with general unemployment steady at 4.2% and inflation over 3%, and it is very unlikely the Fed would cut rates this year.

The Fed’s reaction function turns more hawkish

In recent weeks there has also been a big shift in how the market is interpreting the Fed’s willingness to administer rate hikes and accept the corresponding economic damage needed to get inflation under control (the Fed’s monetary policy “reaction function” in economics parlance). Members of the Federal Open Market Committee who earlier signaled a bias toward easing have recently pivoted to a more hawkish stance; a majority now see the possibility of renewed rate hikes if inflation remains unabated. The official statement from June’s meeting erased outstanding questions about the Fed’s view on inflation under Chairman Warsh: “Inflation remains elevated relative to the Committee’s 2 percent goal, in part reflecting supply shocks that have driven price increases in certain sectors, including energy. The Committee will deliver price stability.”

Warsh added in his post-meeting press conference, “we’ve missed for five years, and we’re going to fix that.” A less immediate but still relevant factor for longer-term rates is the fact that Warsh has been a long-time critic of quantitative easing and its corresponding mountain of assets on the Fed’s balance sheet. The Fed paused the partial “run off” of assets (quantitative tightening) back in December 2025, but $6.7 trillion worth of treasuries, mortgage-backed securities, and other debt remain. Warsh announced he is setting up a task force to provide policy recommendations on what to do with the balance sheet. As Fed Chair he alone chooses who sits on the task force.

In our view, a survey of the economic landscape strongly suggests a continuation of the “higher-for-longer” policy regime. Even if headline inflation moderates, the Fed is likely to proceed cautiously, wary of repeating the stop-and-go mistakes of the 1970s and the “transitory” miscalculation during the COVID pandemic. Longer-term yields, which the Fed has minimal control over, will likely remain elevated due to the strong economy and its corresponding inflation risks, combined with ever-increasing global government debt spending and surging corporate debt issuance.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.