Animal protein struggles to keep up with shifting tastes

Key points

- Animal protein markets are increasingly out of sync with consumer demand. Demand remains resilient, but supply responses vary sharply by species.

- Beef faces the clearest supply-demand mismatch: Consumers support record prices, while tight cattle supplies, poor pasture conditions and limited herd rebuilding limit availability.

- Pork is dealing with the opposite challenge. Modest production growth flanked by lackluster domestic interest increasingly favors export reliance, especially to Mexico.

- Chicken supply growth is pressuring white meat and wing values, even as demand improves through QSR channels, dark meat and broader per-capita consumption growth.

Consumers are searching for high-quality and affordable protein

Consumer demand drives the animal protein sector, but supply response often lags shifting consumer preferences. Beef offers the clearest example of this divergence: Limited cattle supplies are pressuring the beef market, yet consumer appetite for beef is uncompromised, even in the face of record or near-record prices. That demand strength is supportive for producers, but it also forces the market to rely more heavily on imported lean beef to meet ground beef supply needs.

Chicken and pork face the opposite issue. Chicken supplies remain abundant, particularly in food service and quick-service channels, where traffic has reportedly slowed this period amidst higher gas prices. Pork production is also expanding modestly, but demand is not growing at the same pace. That places more pressure on exports, especially as China continues to pull back from U.S. pork purchases and Mexico becomes even more important to the U.S. pork balance sheet.

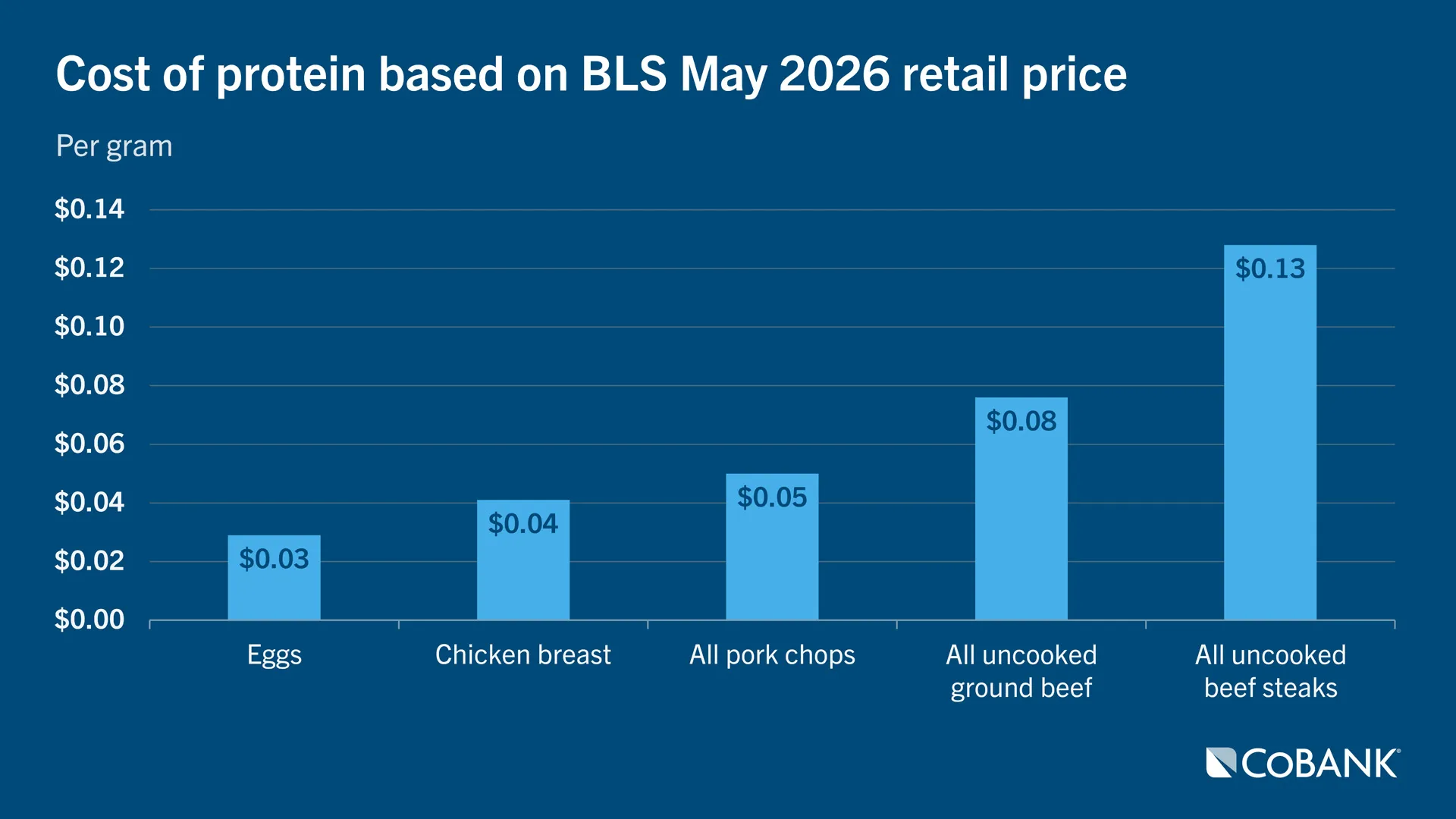

The result is an animal protein complex that is out of sync with consumers. Consumers are signaling willingness to pay for beef despite limited supply, while lower-cost pork and chicken alternatives have not fully absorbed the available production. Comparing the per-gram cost of protein may help explain the tension. If pork, chicken or eggs are more affordable protein options, the key question is why consumers are not shifting more aggressively toward those products. The answer likely reflects more than price alone, including taste, quality perceptions, meal preferences, convenience and food service menu dynamics.

For producers and processors, adapting to those choices will take time. Supply chains cannot pivot overnight, but the direction of consumer demand will increasingly determine which proteins carry pricing power and which must rely on exports or promotions to clear product.

Beef

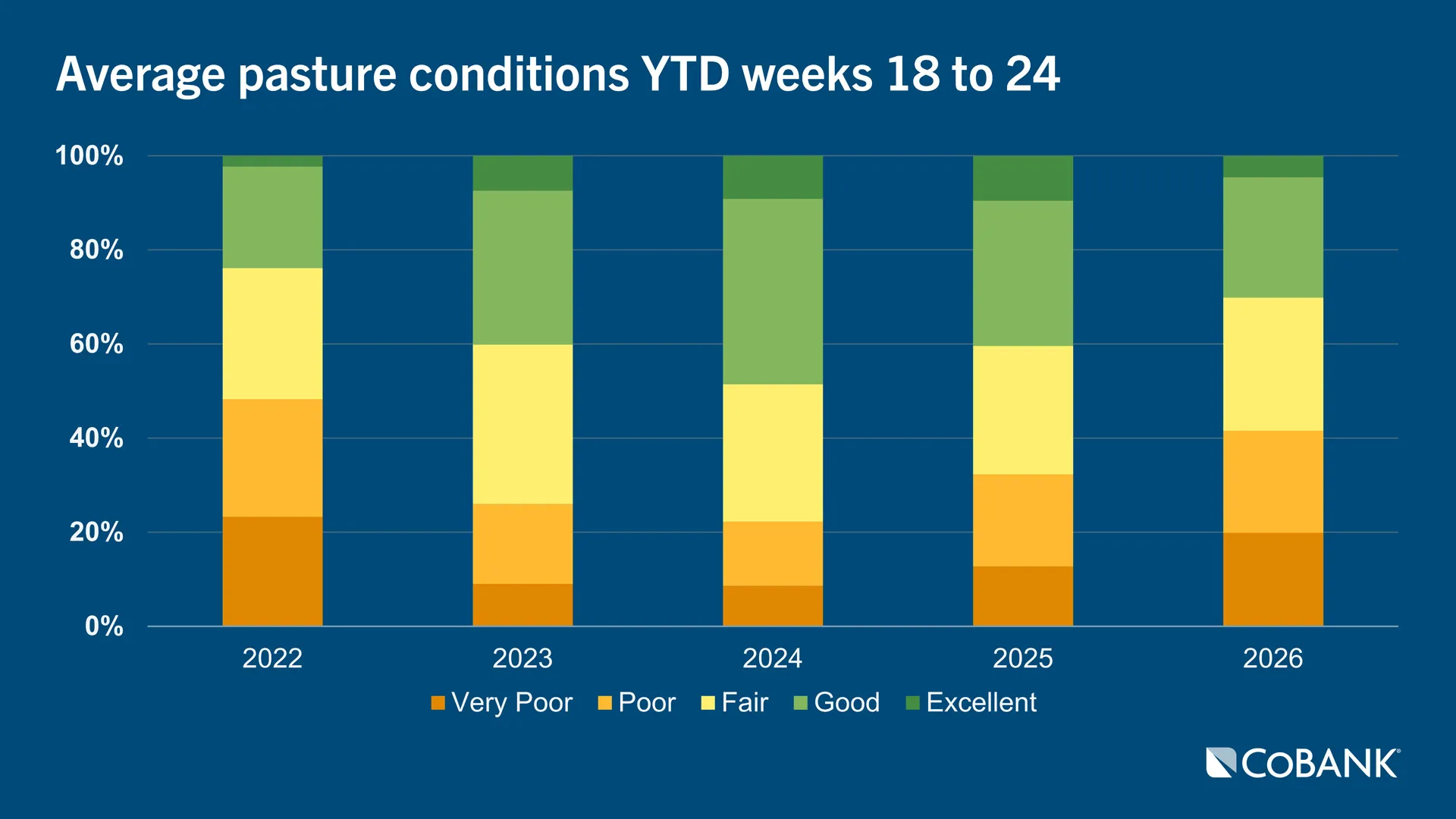

The beef sector is defined by a difficult imbalance: Consumer demand remains exceptionally strong, but the industry has limited ability to expand supplies quickly. Pasture conditions are the weakest since 2022 with an average 42% of pasture rated poor or very poor through the first seven weeks of reports. That matters because adequate forage is foundational to herd rebuilding. Without reliable pasture and feed resources, producers are less likely to retain heifers, slowing the industry’s ability to rebuild the cow herd after several years of liquidation.

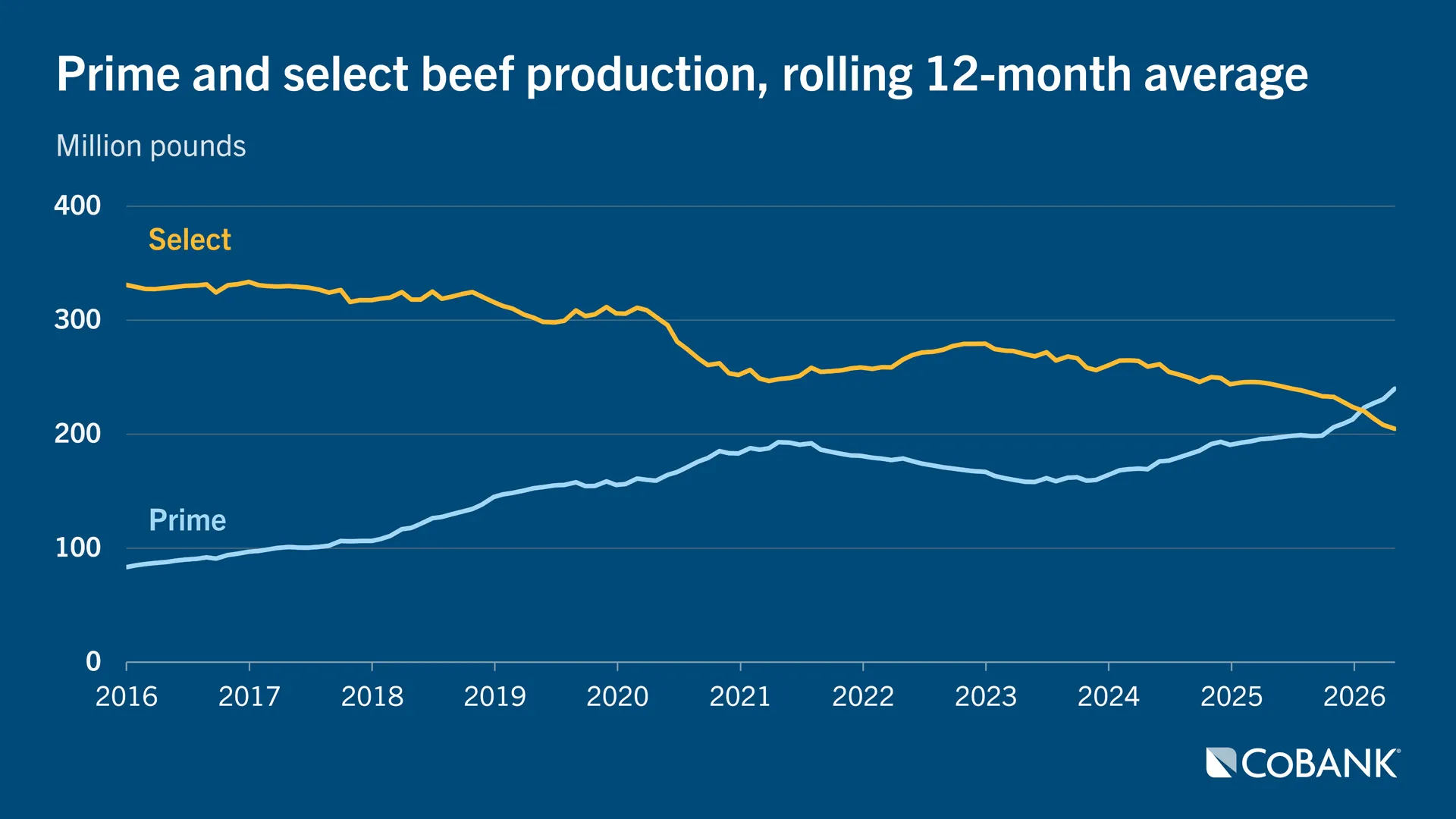

At the same time, consumers are receiving a higher-quality beef product than in prior cycles. The share of beef grading Prime, the highest grade, has climbed sharply over the past decade, while Select has declined. In early 2025, Prime beef production exceeded Select for the first time since 1988. The trend has continued for six consecutive months since November 2025 with 94 million more pounds of Prime production over Select, and the 12-month rolling average puts Prime availability now firmly above Select. The Choice cutout flirted with $4 per pound in June, up about 5% YoY, and the spread to Select has been widening the split demand signal. Even as beef prices remain elevated, consumers’ willingness to pay a premium reveals their preference for quality.

Tight domestic supplies are showing up in slaughter data. Federally inspected cattle slaughter is running about 1 million head below last year through early June and 2.3 million head below the 2022-2024 average. Fewer cattle moving through the system increases the need for imported lean beef, especially to support ground beef demand via dairy and beef cows as opposed to traditional cattle on feed.

Disease is always a risk in the livestock industry, regardless of species. Now that the U.S. has confirmed cases of New World Screwworm, it remains a risk to monitor. However, current fundamentals including pasture conditions, herd demographics, slaughter availability and strong consumer demand remain the more important drivers of the U.S. cattle outlook.

Pork

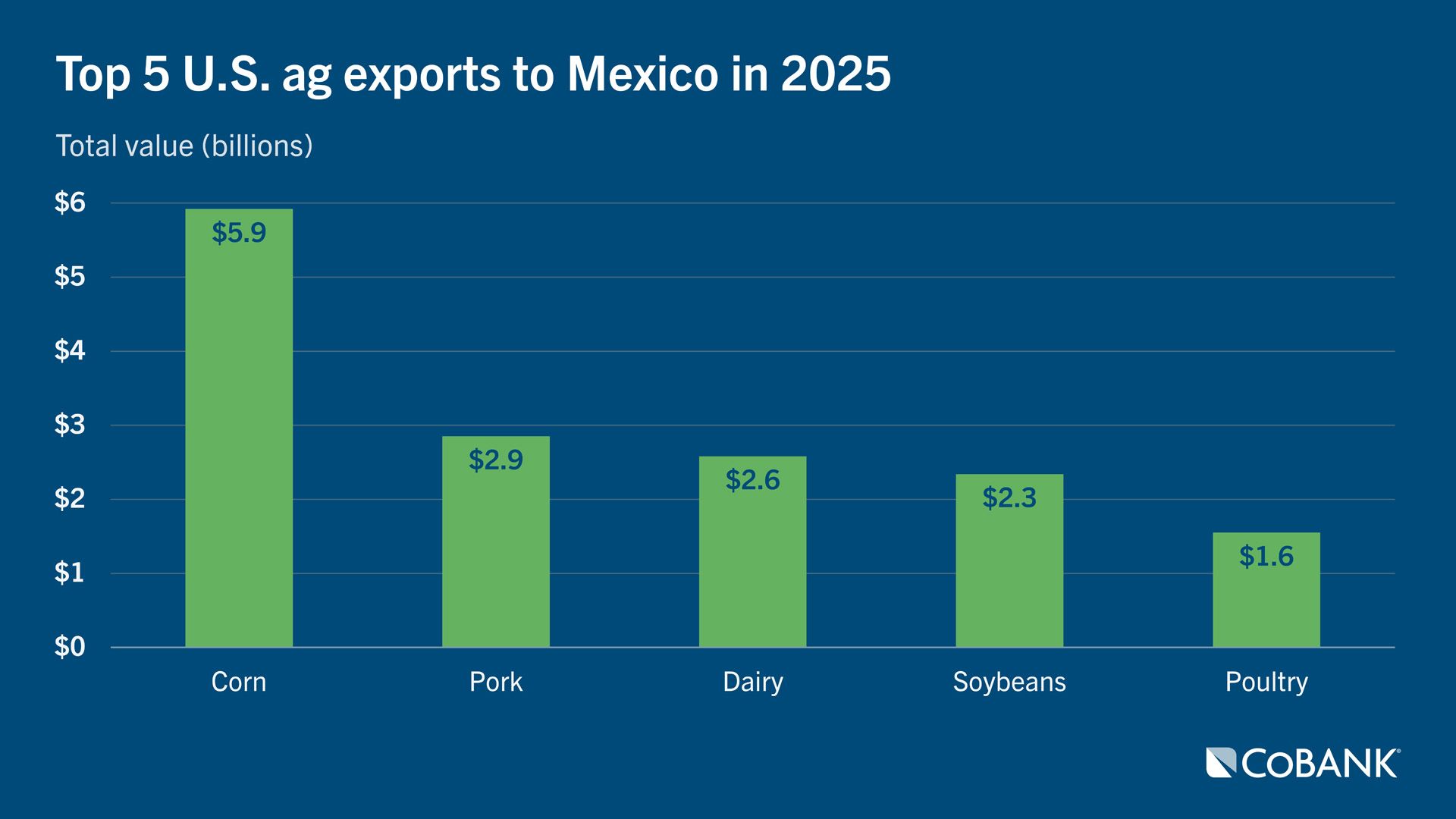

Entering the second half of the year, pork supplies appear ample; production is edging higher and exports will play a critical role in maintaining balance. U.S. pork remains highly competitive in global markets, with roughly 30% of production exported. Mexico is the largest buyer and remains especially important for hams, making the discussions around the U.S.-Mexico-Canada trade agreement a key watch item. Any disruption around market access would have immediate impact because Mexico absorbs a meaningful share of U.S. pork movement.

Domestic markets fell short on delivering the seasonal rally strength typically expected heading into summer for grilling season. The pork carcass cutout has hovered near the $100 per hundredweight level and remains below year-ago and longer-term averages. Prices for loin and ham primals, which each represent about one-quarter of carcass value each, have been relatively stable. Price-competitive U.S. ham has helped support export movement to Mexico. But that also raises questions for later in the year of how long that pace can continue and will there be adequate hams (amidst lower beef and turkey inventory) available as holiday demand builds?

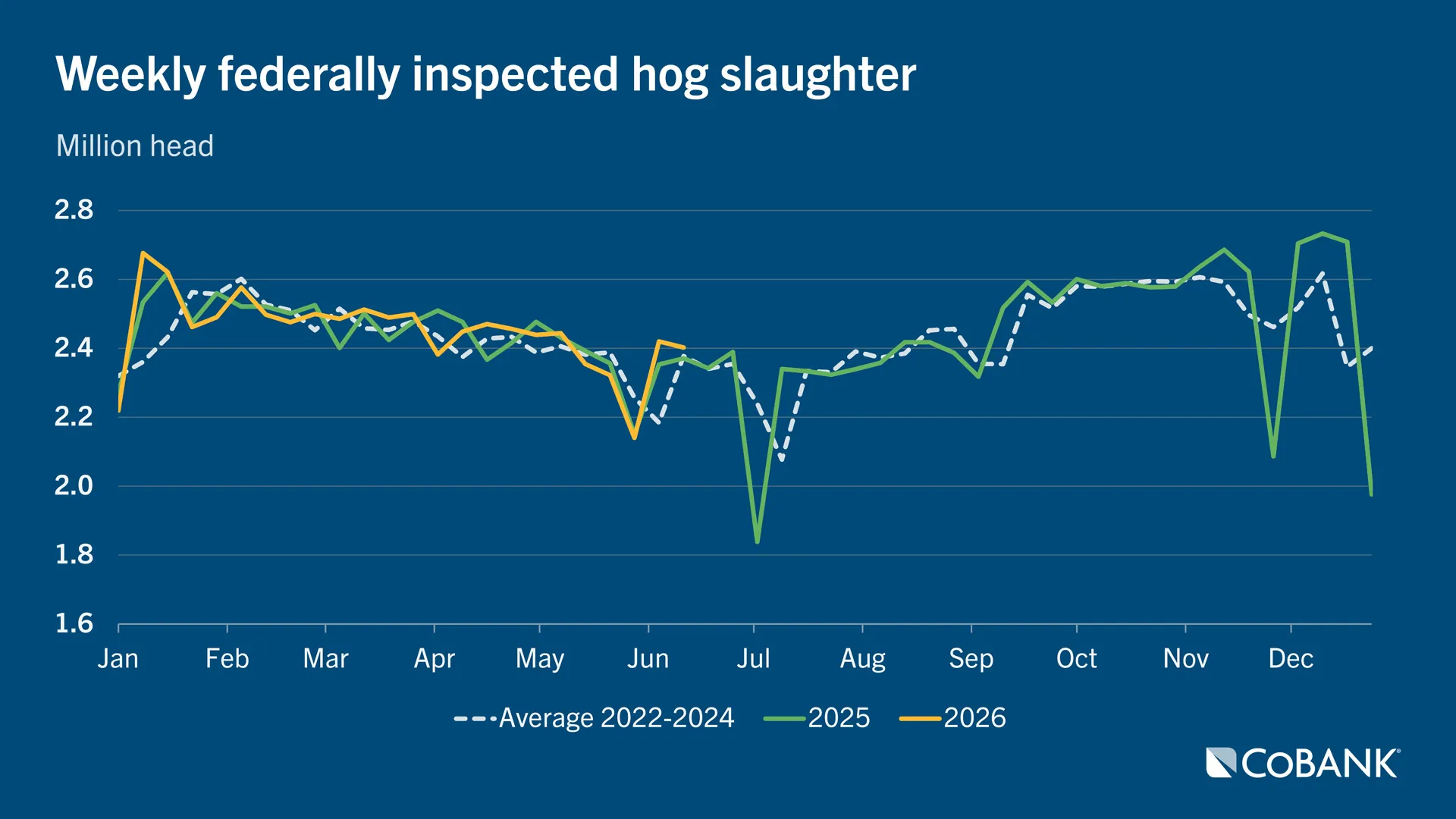

Production fundamentals also point to more pork on the market. Weekly federally inspected hog slaughter is running marginally above year-ago levels by 0.2%, while dressed weights are 2 pounds heavier on the year-over-year average. Together, those gains over time are adding meaningful tonnage, with monthly pork production running 1.1% above last year despite weather-related disruptions early in 2026.

The larger strategic question is where to send incremental pork production. China has steadily reduced its reliance on imported pork following African Swine Fever eight years ago, and consumer preferences are shifting, particularly among younger consumers. With global pork consumption still significant but China less dependable as a demand outlet, U.S. pork profitability will hinge on maintaining export competitiveness while navigating stable domestic demand and rising supplies.

Poultry

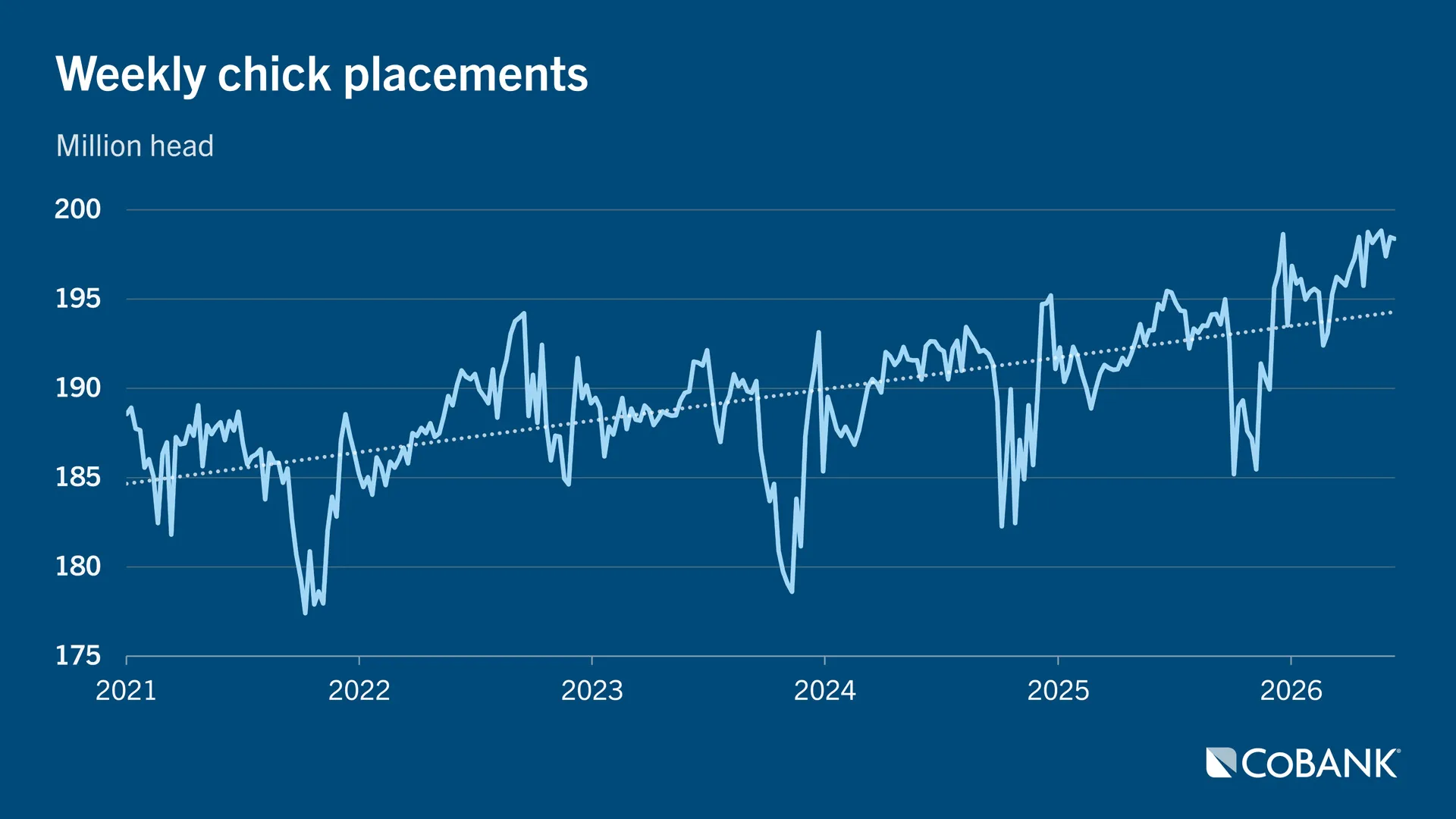

As consumers assess their protein consumption needs, they continue to favor chicken for its convenience and innovative product options. While the demand side of the equation has been strong and buyers want more chicken, expansion had been slow prior to 2026 because of lagging livability and hatchability rates.

During the fourth quarter of 2025, the U.S. broiler type hatching egg layer flock averaged a total of 59.87 million head, which was down nearly 2% YoY, and the lowest total since 2019. In the most recent Chickens and Eggs report, USDA estimated the broiler supply flock has grown to 61.34 million head. Adding to the flock supports broiler supply both in headcount and productivity rates. With the rebound in the layer flock, chick placements have been running above trendline growth in nearly all weeks of 2026.

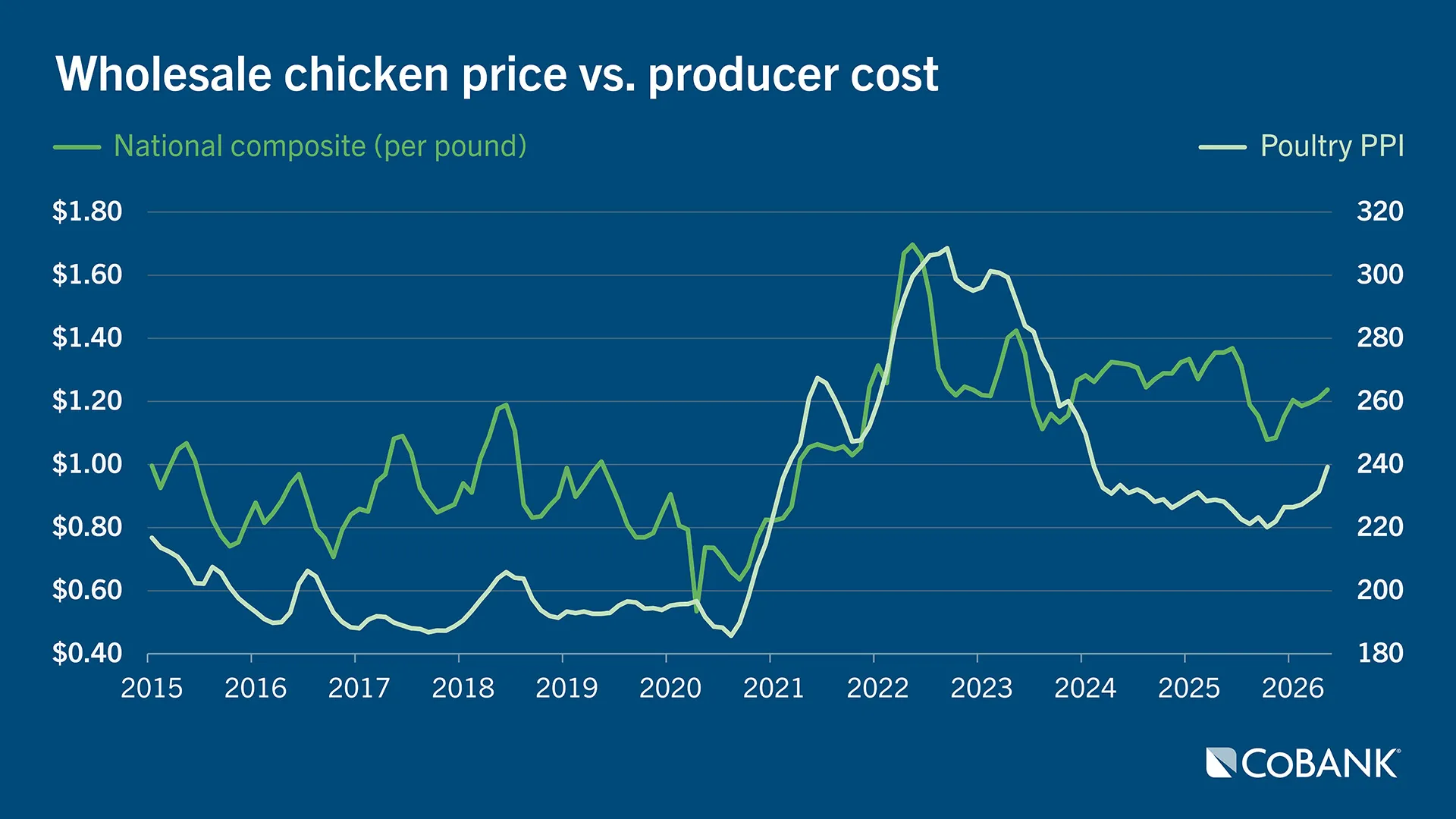

Broiler production rose more than 3% YoY during the first quarter, burdening market values, but the second quarter should be about 2%, a historically more comfortable growth rate for markets. While prices for the front half of the bird have been under pressure, cold storage inventories do not necessarily reflect that weakness. Breast meat inventories were down 4% YoY at the end of April and leg quarters in cold storage were down 9% despite trade uncertainties. Of note, rising domestic interest in dark meat is showing up in higher prices this year. Breast meat values were about even with thigh meat a year ago, however breast meat is trading at a discount of about $1.30 per pound YoY, while boneless/skinless thigh meat is down just $0.40 per pound. Overall, the broiler composite has been in the low $1.20s during the second quarter, down about 10% YoY.

Despite elevated production costs, feed costs remain subdued. Although chicken values have come under pressure and are crimping margins, broiler integrators are well positioned to remain profitable and also grow share of plate this year. USDA is currently projecting annual U.S. per capita chicken consumption will grow by more than 3 pounds during 2026.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.