Surge in grid spending tests utility supply chains

Key points

- Efforts to replace aging infrastructure, harden the grid and meet rising load growth continue to push demand beyond supply.

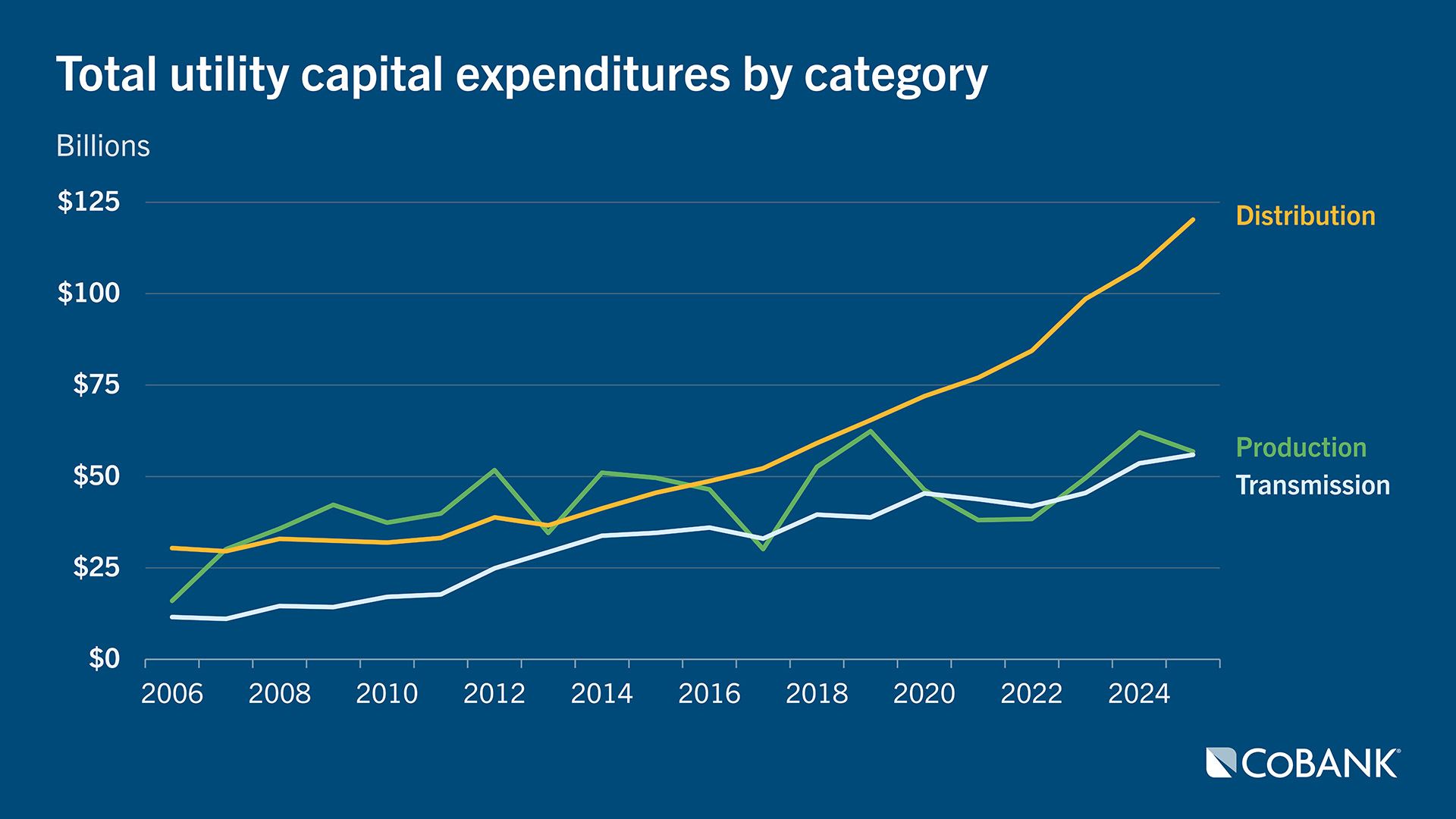

- Electric utility annual investment has surpassed $200 billion (up 42% since 2020), with capital spending for distribution far outpacing transmission and production.

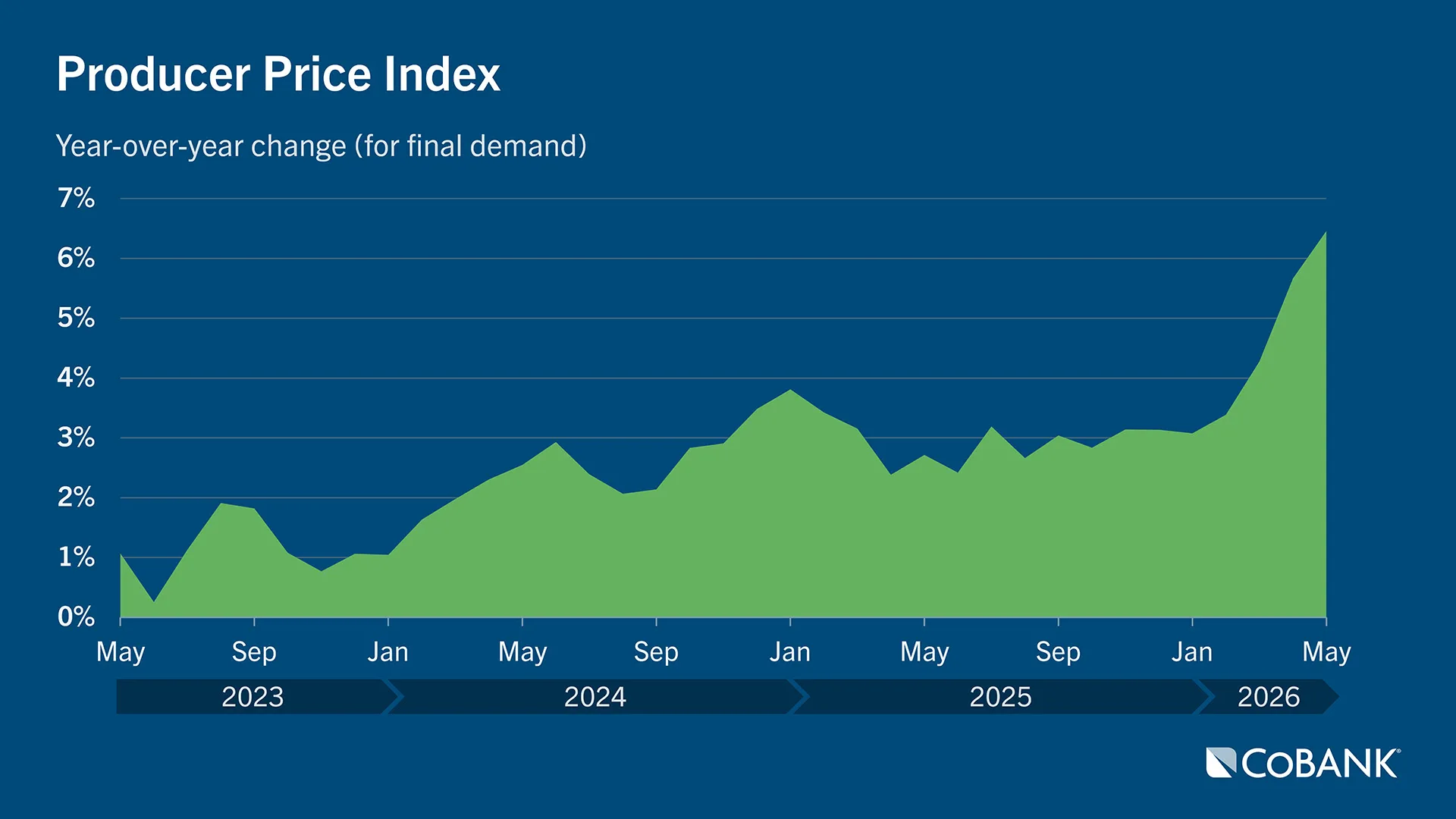

- Elevated lead times, costs and inflation continue to challenge the industry, with the May 2026 headline PPI up 6.5% year‑over‑year.

Over the past five years, electric utilities have invested unprecedented amounts of capital in infrastructure. The compounding factors of aging infrastructure, an increasing focus on grid hardening and rising load growth has driven annual investment over $200 billion (up 42% since 2020). Alongside this surge in spending, supply chain constraints have intensified, as demand for critical materials has outstripped supply resulting in longer lead times, rising costs and ongoing labor shortages.

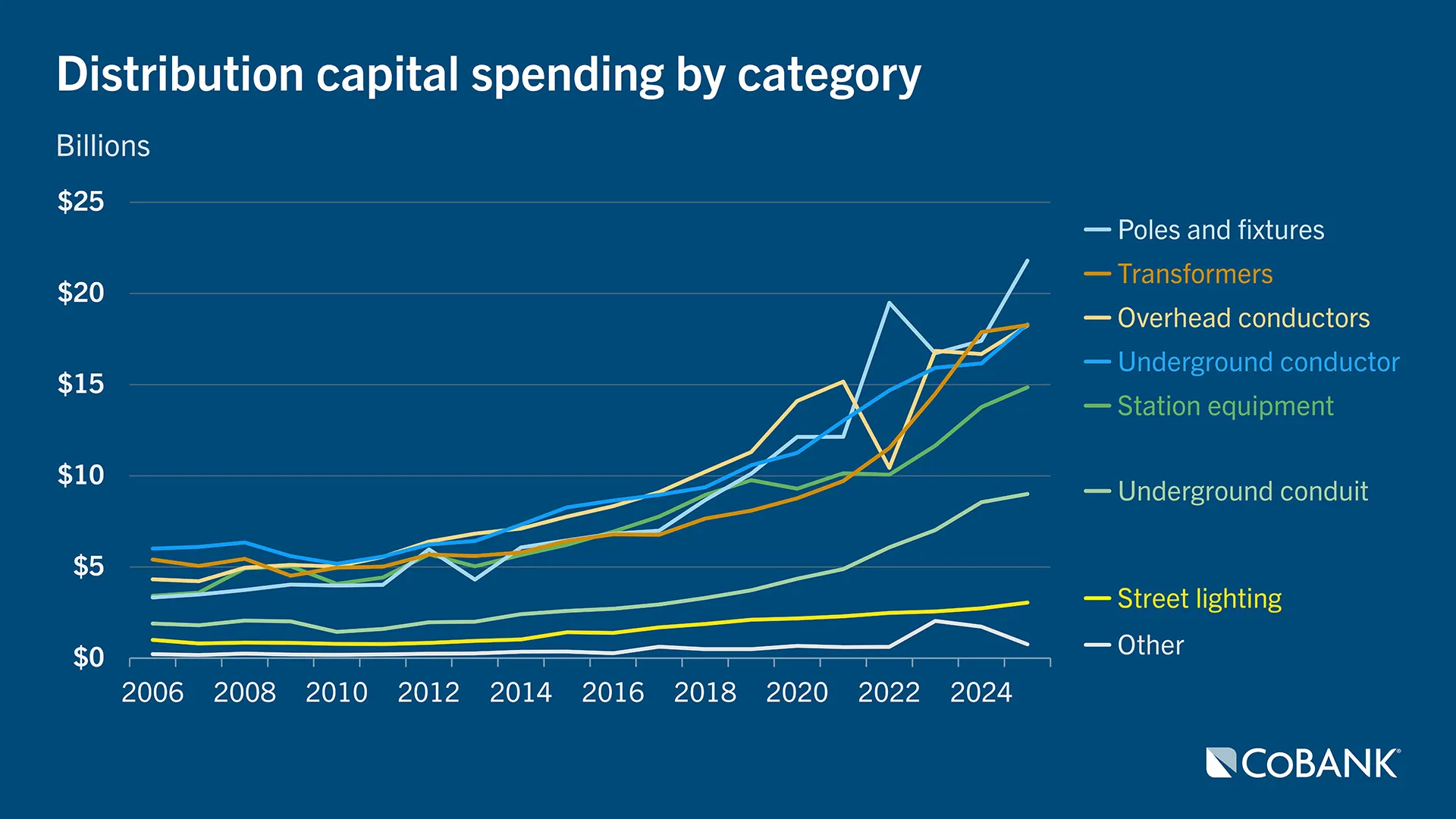

Distribution bears the first impacts of load growth, electrification, distributed energy resource programs and reliability, putting it under earlier and more continuous pressure than transmission or generation. Since 2020, spending in this category has nearly doubled; while increases are broad-based, they are concentrated. In 2025, 87% of the $104 billion spent on distribution went to four categories: poles and fixtures, conductors, transformers and station equipment. The sheer volume and fragmentation of distribution materials simply requires more capital expenditures than other parts of the system.

Rising investment throughout the utility value chain has introduced new challenges in supplying critical inputs. Early constraints emerged in manufacturing capacity and technical labor, especially for highly specialized equipment such as transformers, breakers and switchgear. Equipment lead times, once typically under a year, extended to as long as three and four years, making timely project delivery increasingly difficult. Today, manufacturing capacity is gradually expanding, supported by U.S. reshoring, original equipment manufacturer growth and increased global production, which should ease constraints over time. Meanwhile manufacturing labor supply remains strained, and cost inflation continues to plague the industry. Since 2020, cost inflation in key utility components has outpaced both the Producer Price Index and Consumer Price Index, signaling structural undersupply of critical inputs.

Looking forward, the investment cycle is only ramping up with S&P Global, Edison Electric Institute and Deloitte all anticipating total capital expenditures to exceed $1 trillion over the next five years. Major forecasters are broadly aligned on the key drivers of utility spending: rising load growth, grid hardening to address increasingly volatile weather, replacement of aging infrastructure and system modernization. This persistent increase in demand will test already fragile supply chains and the industry will likely continue to face extended lead times, labor shortages, raw material scarcity and rising cost pressures.

Near-term geopolitical events put more kinks in supply chains

Recent geopolitical events are intensifying inflationary pressures and worsening an already difficult operating environment. As the Iran conflict passes the four-month mark, utility industry producers are feeling the sting of oil supply scarcity and related high prices. Over the last quarter, the headline Producer Price Index has risen sharply. The PPI is up a surprising 6.5% year‑over‑year for May 2026 — the largest since the surge following Russia’s invasion of Ukraine in 2022.

Energy prices have been the primary driver, pushing producer inflation higher and impacting the utility supply chain across manufacturing, chemicals, freight, and transportation. However, in addition to energy-based increases, core PPI (which removes the influence of food and energy) also rose in May (0.8% month over month), which indicates broader cost pressures across labor and other supply chain inputs. While easing tensions with Iran would likely help moderate PPI, producers continue to face inflationary pressures beyond the current geopolitical environment.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.