Crunch time is now for meeting RVO

Key points

- This year’s level of blending will determine if EPA can continue to take the RVO on an upward trajectory for 2028 and beyond.

- The domestic biomass-based diesel industry will need to operate at the upper range of its demonstrated capacity while simultaneously relying on increased imports.

- RIN markets will need to be the equalizer to encourage blending or higher utilization rates.

The Environmental Protection Agency delivered an agriculture-friendly renewable volume obligation (RVO) mandate this spring, but the real test is whether the refining industry can ramp up to meet the ambitious blending volume targets for 2026 and 2027.

The industry is playing catch-up due to a variety of factors, including last year’s uncertainty around the rule, the 2025 elimination of the biodiesel blenders tax credit, the shift to the 45Z Clean Fuel Production credit that excludes non-North American fuels, and the rule’s late release.

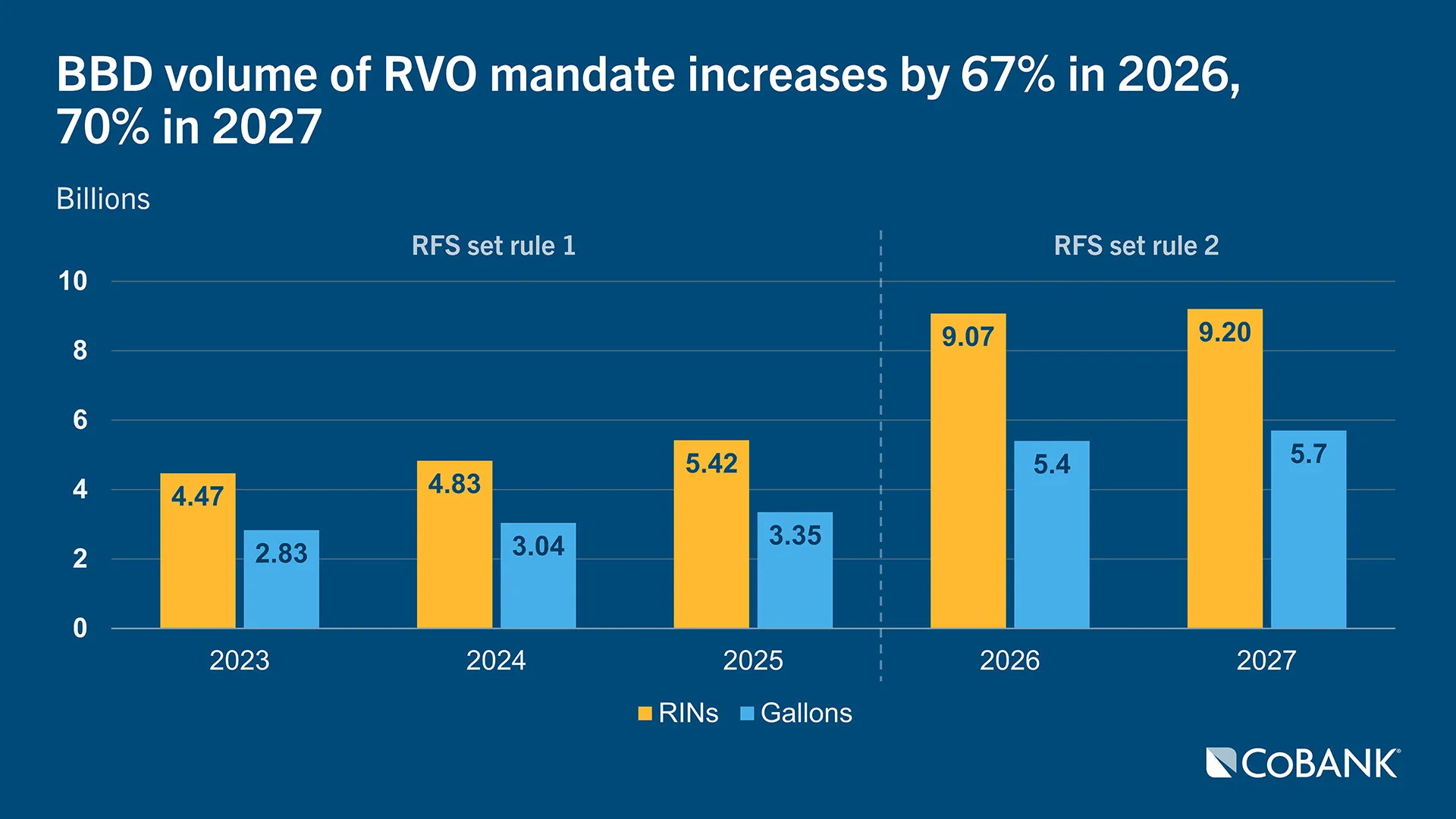

The RVOs for the next two years jump by 67% and 70%, respectively, above the 2025 total of 5.42 billion gallons. Previously, the largest year-over-year increase in the biomass-based diesel RVO was 28% in 2013. The Renewable Fuel Standard allows refiners to carry over 20% in excess renewable identification numbers (RINs) from the previous year.

Compliance data will shape EPA’s next move

EPA set Sept. 1, 2026, as the deadline for obligated parties to submit their 2025 RIN retirements, and it will release the official final 2025 annual compliance data and reports shortly thereafter. By the time EPA has this data, the market may be facing tight feedstock availability, a smaller RIN bank, and rising pressure from obligated parties trying to manage compliance for 2026 and into 2027.

EPA could propose mandated blending levels for 2028 and beyond as soon as this fall but is more likely to wait until 2027 to see how production capacity is tracking with the upward trajectory of the RFS.

For 2026, the Energy Information Administration projects renewable diesel (RD) output will be up 24% and biodiesel up 41%. Combined capacity utilization for RD and fatty acid methyl ester (FAME) biodiesel producers topped 70% in April 2026, versus 56% on average in 2025.

Meeting RVOs would require near-record FAME runs and unprecedented renewable diesel output, with capacity use rising to 90% in 2026 and 95% in 2027, well above the nearly 60% seen in 2025. In addition, refiners are unlikely to expand capacity or increase investment without clearer long-term policy signals.

Even as U.S. renewable diesel and biodiesel utilization improves, production remains below mandated levels. Imports and reduced exports may narrow the gap, but they likely won’t close it without more supply or policy changes. Earlier exported volumes do not count toward compliance, worsening the shortfall. While some facilities can shift from sustainable aviation fuel to renewable diesel (which has stronger margins), contracts and export incentives continue to divert SAF volumes overseas.

RIN markets become the pressure valve

The RIN bank started the year around 2.9 billion RINs and fell to roughly 680 million RINs within five months. Monthly shortfalls could be between 150 million to 165 million RINs, Bloomberg Intelligence projects. E15 fuel could add incremental voluntary blending, especially where retail price discounts are meaningful and infrastructure is already in place. However, ethanol produces fewer RINs per gallon than biomass-based diesel pathways.

The agricultural sector is eager to do its part to meet the RVO mandate. Soybean crush facilities are ramping up and seeing higher soybean oil prices as biofuel processors use additional soybean oil. The U.S. soybean industry expects to crush 57% of the domestic crop this year and next, up from 52% in 2024, to meet demand for biomass-based diesel.

In March, biomass-based diesel production utilized record amounts of domestic soy oil (1.28 billion pounds) and distillers corn oil (432 million pounds), EIA reported.

RINs are priced to encourage compliance and create an economic incentive to expand supply to meet the mandate. For its joint venture between Diamond Green Diesel and Valero Energy, Darling Ingredients produces 1.2 billion gallons of renewable fuels and can toggle between SAF and RD. In a recent investor call, Darling Chief Financial Officer Robert Day said, “RINs will need to be the great equalizer that creates the margin that we need to make enough volume to satisfy the RVO.”

The question remains whether there will be any RINs left at the end of 2026 to purchase for compliance by obligated parties for companies that don’t create their own. Without the former biodiesel tax credit, higher D4 RIN values help support the economics needed for positive biodiesel and renewable diesel margins.

At the same time, if RIN prices move to extraordinary levels and compliance becomes difficult or costly, the political coalition supporting biomass-based diesel could fracture. The American Fuel & Petrochemicals Manufacturers already announced a lawsuit over the RFS volumes, which sent soybeans’ value down 30 cents per bushel on the news. AFPM said the maximum cost of complying with the RFS could be 37.5 cents per gallon, with the low-end costs estimated at 8 to 10 cents per gallon. On the other side of the equation, EPA calculated that the finalized 2026-2027 volumes will generate over $10 billion in economic benefits for rural America and said the RVO demonstrates the administration’s “ongoing commitment to American farmers.”

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.