Tight farmer margins expected to slow input buying

Key points

- Higher input costs and weak commodity prices are tightening farmer margins, which may delay product movement through agricultural retailers.

- USDA projections show elevated production costs are becoming structural. Per-acre costs are rising and expected to remain elevated into 2027.

- While retailers should prepare for more cautious fertilizer and chemical buying, they have opportunities to provide farmers with insights on how to maximize yields.

Elevated input costs and weak commodity prices are expected to pressure farmer margins, slowing purchasing decisions and potentially reducing product movement through agricultural retailers. With lower commodity prices projected in 2026, producers will be focused on protecting yields while limiting input spending, forcing difficult choices on in-season chemical applications and fertility plans for the next crop year.

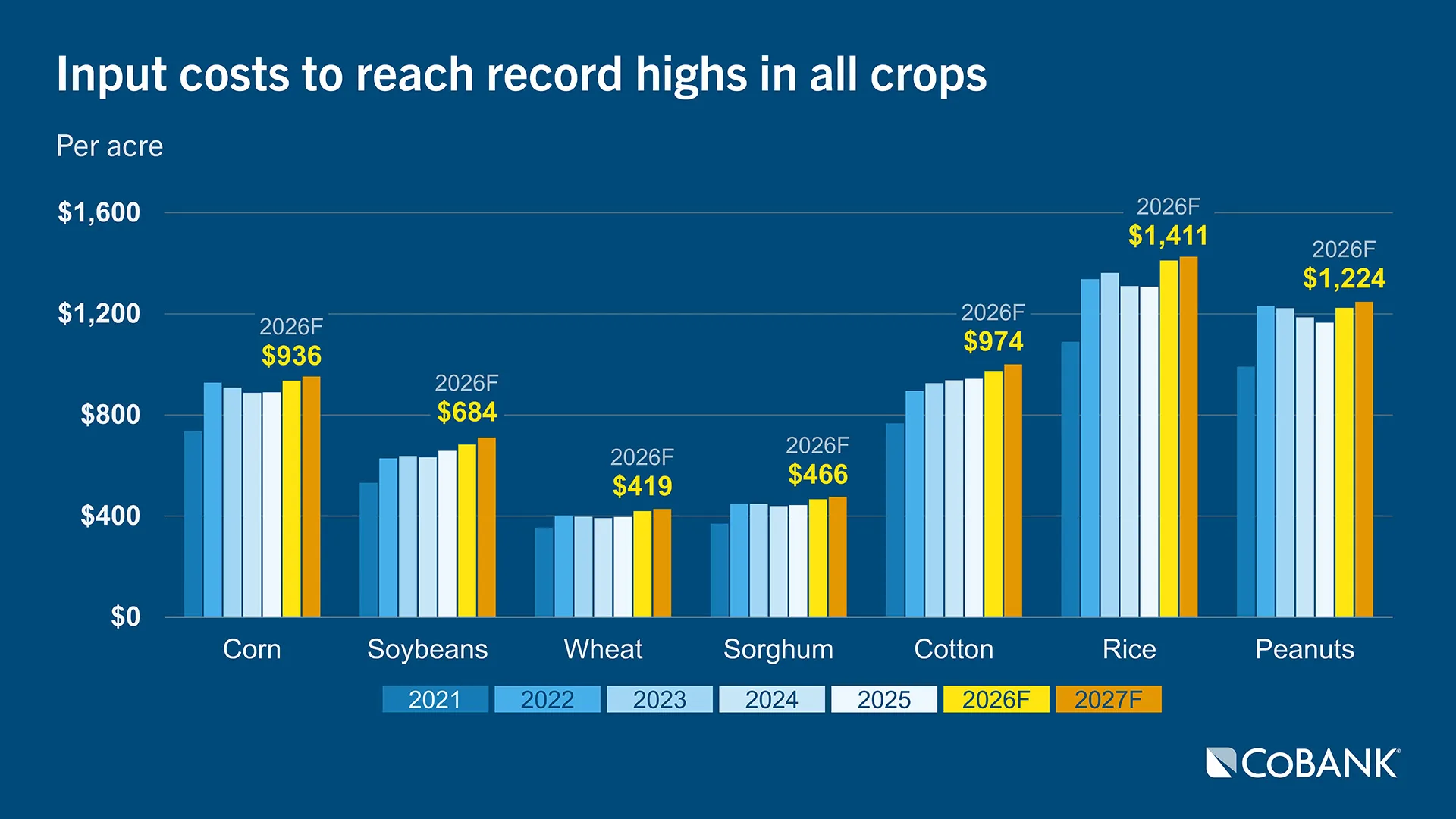

USDA updated its 2026 cost-of-production per acre cost estimates and offered a first look at 2027 projections, showing the structural shift of higher input costs is here to stay. The 2026 forecast was also up for all commodities from initial estimates provided earlier this year for the current growing season.

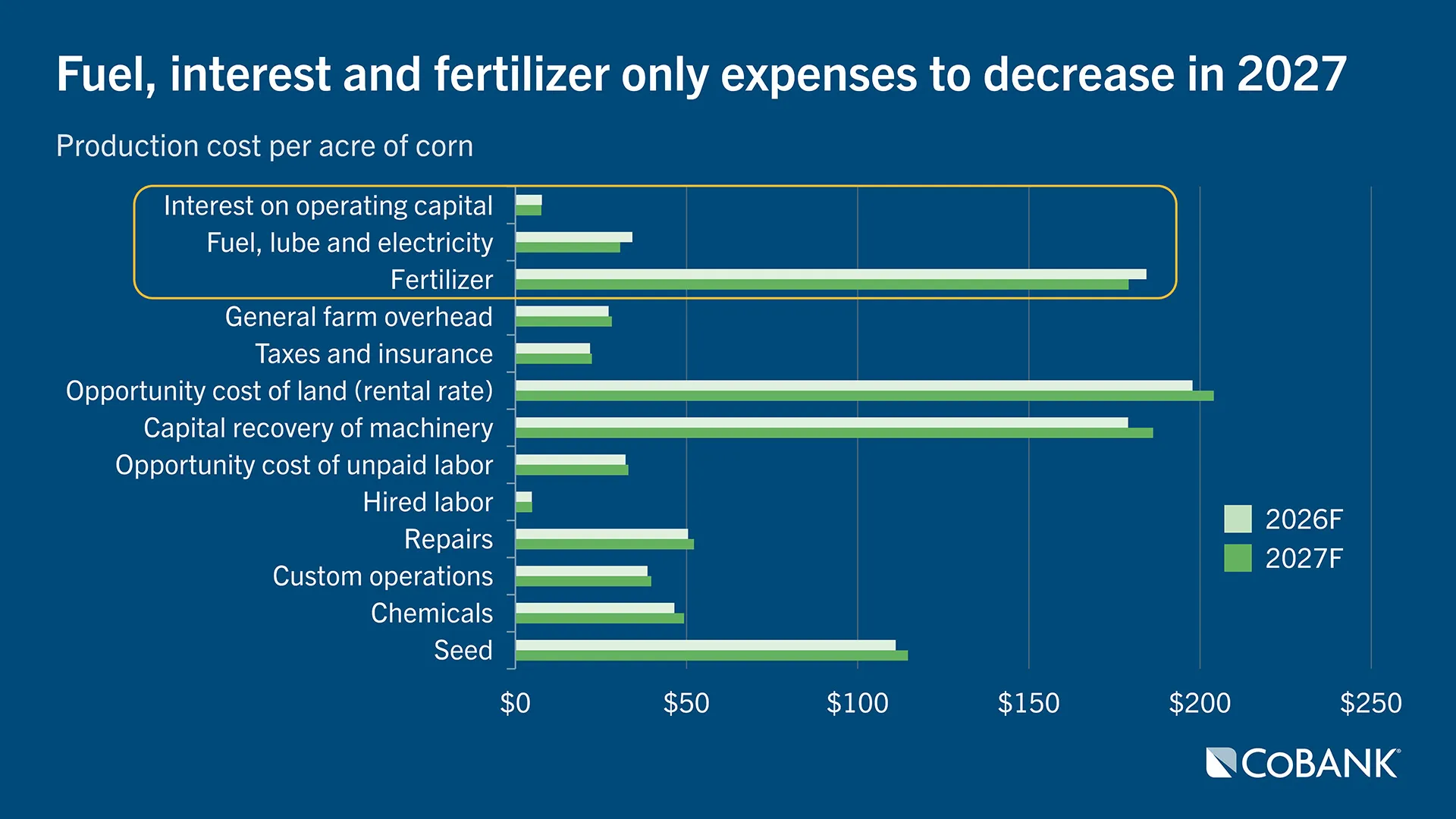

For the average national corn grower, it is estimated to cost $935.79 per acre with all operating and allocated overhead costs, up 2% from the forecast earlier this year at $917 per acre. Fertilizer prices were increased from previous estimates but do see a slight decline from an estimated $184 per acre this year to $179 per acre in 2027. Fuel, lube and electricity costs were projected higher from earlier USDA forecasts at $34 per acre and are anticipated to soften to $30.59 per acre next year. Interest rates are one of the few budget line items forecast to fall slightly, and that is contingent on what overall interest rates do in the face of inflation pressures.

A soybean producer’s costs per acre are estimated at $684 per acre, up from $678 projected earlier this year. Next year, that same expense is expected to climb to $701. For wheat producers, 2026 costs are projected at $419, up $10 per acre from estimates earlier this year, and USDA sees that escalating to $428 in 2027.

Working capital continues to erode in the countryside, but those farmers who own their land have a tremendous asset they can use as collateral to manage these higher input costs. These higher costs will also force producers to push the pencil and weigh every input decision.

USDA projects higher seed and chemical prices in 2027 versus 2026. Seed costs have consistently climbed over the past decade and because farmers are brand loyal, they’re unlikely to make major shifts to lower priced seeds. Although chemical costs are projected higher, agricultural retailers may be able to appeal to customers looking to reduce costs by offering more generic chemicals. Active ingredient patents are expiring faster than new products are coming online, opening the door for agronomy divisions at retailers to capture this growing market segment if they can still guarantee the efficacy of alternative chemicals.

Fertilizer demand remains hard to forecast

While fertilizer prices have backed off their highs resulting from the Iran conflict, the economics are still challenging for farmers. Retailers have already started buying phosphate supplies for fall application, and will continue buying through the summer. Yet estimating projected volumes may be tricky. Farmers have already pulled back on phosphorus and potassium nutrient purchases in their fertility plans over the last two years, and retailers should anticipate that mentality of restraint to continue. Phosphate applications were reduced especially in drought-impacted areas in the western and southern Plains. Many retailers may still have supplies held over from 2026 to meet some of the 2027 demand that is also anticipated to be lower.

The reality of farmers delayed buying of nitrogen could create supply chain headaches for retailers buying summer fill. The summer fill period may be pushed back a few months to balance anticipated grower demand while managing the higher interest rates. With interest rates at 6%-8%, retailers face a significant cost for several months if farmers don’t purchase until spring if nutrient prices remain at elevated levels.

For agricultural retailers to remain profitable, they also need to see their farmer customers find ways to profit in the tight margin environment. The balancing act of corresponding supply and demand of products at the right price level will be a challenge for retailers to help the farm economy adjust to the ongoing structural shift of elevated production costs and help farmers push yields higher to offset lower commodity prices.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.