Shrinking rice production sparks price recovery

Key points

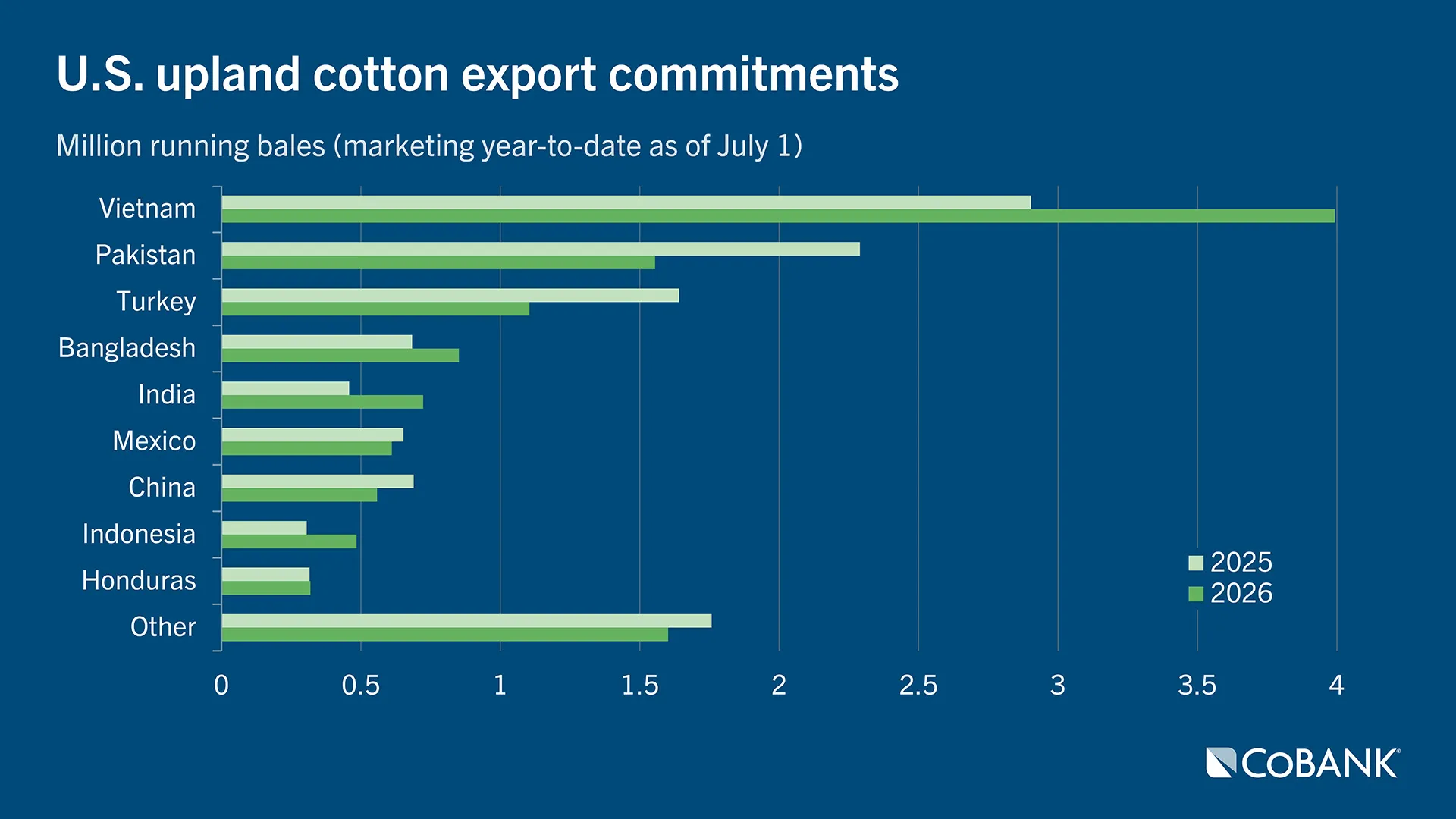

- Cotton exports remain strong on stout Vietnamese demand.

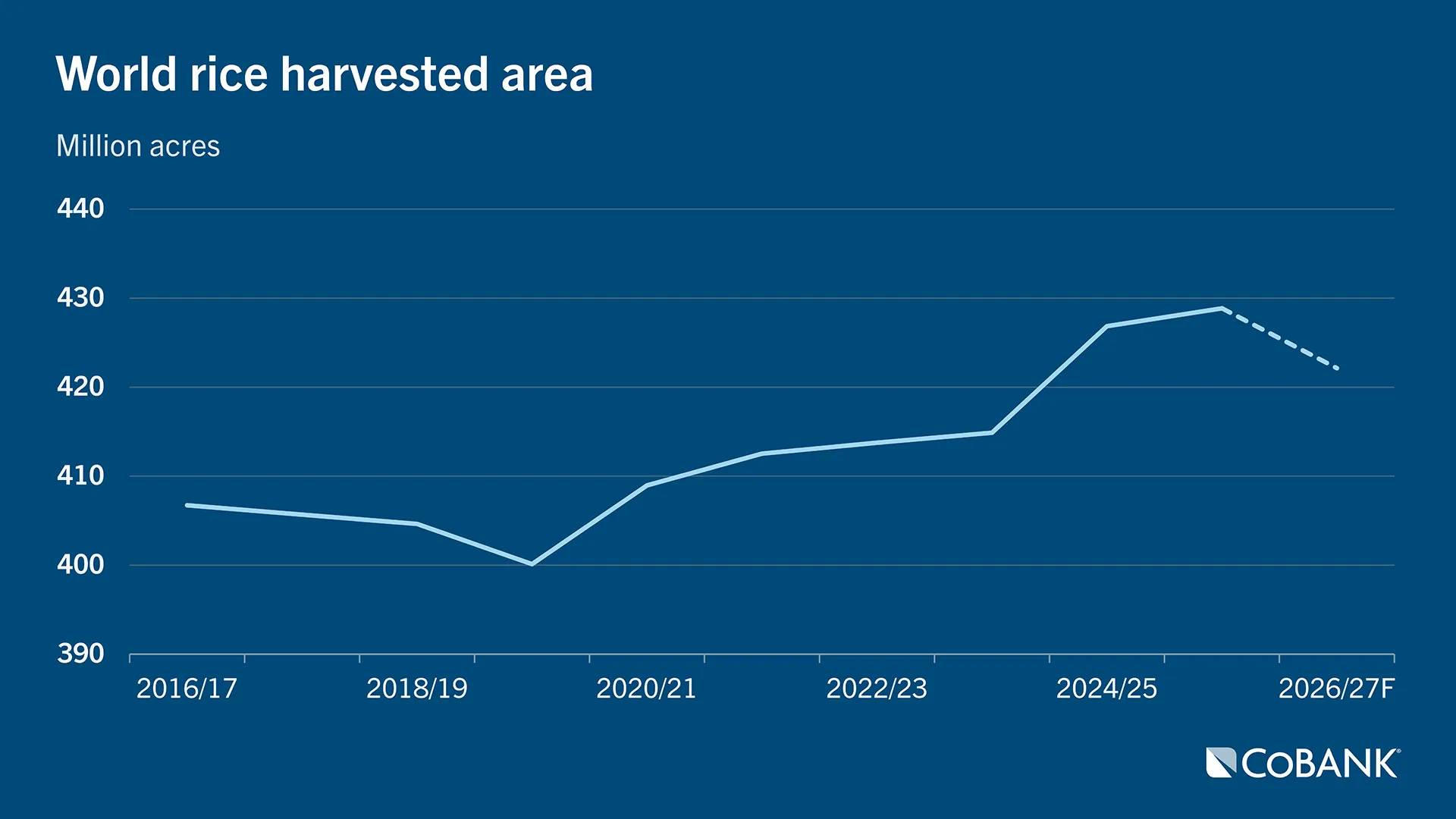

- Long-grain rice acreage in the U.S. has fallen to its lowest since 1974, plunging 34% YoY, causing grain dryers to idle operations.

- Sugar prices are climbing on U.S. smaller crops and rising consumer demand for natural sugar.

Cotton

Cotton prices rose 8.0% last quarter despite a difficult macro backdrop that included a stronger U.S. dollar, shifting interest rate expectations, and volatility across the broader commodity complex. Even so, U.S. cotton exports remain a bright spot for U.S. agricultural trade as tightening global supplies shift more demand back to the U.S.

Cumulative cotton export commitments (shipped and unshipped sales) are running ahead of USDA’s projected pace, led by strong demand from Vietnam. Marketing year sales and exports are up 1.0% YoY. Meanwhile, USDA expects world cotton production to fall 5% YoY from last year as yields decline after last year’s record output. Australian production in particular is expected to suffer, falling by one-third YoY, while Brazil’s exports remain stable. With global consumption expected to exceed production, world ending stocks are on track to fall to the lowest in eight years.

U.S. consumer spending remains resilient, but consumers are showing fatigue from inflation. Retailers report softer unit sales for clothing and apparel, and more consumers are turning to thrift shops and consignment stores. Competition from cheaper synthetic fibers continues to limit mill demand for cotton. Because cotton competes with petroleum based synthetic fibers, the drop in crude oil prices further clouds cotton’s long-term demand outlook.

USDA expects U.S. farmers will plant slightly more cotton this year as cotton prices strengthen, with acreage rising 6.1% YoY to 9.85 million acres. Crop conditions started this spring stronger than last year, particularly in Texas, where early season moisture supported initial development.

Drought threats, though, have returned. More than half of the U.S. cotton crop — 58% — is now in drought, raising the risk that crop conditions could deteriorate if dryness persists, threatening yield potential. Above average temperatures expected across the Southwest could further stress fields that entered the season with limited soil moisture.

Rice

U.S. planted rice acreage plunged this spring to its lowest level in more than 50 years as farmers cut acres in response to abysmal rice prices and record-high input costs, causing numerous grain dryers in the U.S. to be idled. USDA estimates long-grain rice acreage is down 34.1% YoY to 1.4 million acres, the lowest since 1974. The combined acreage of short-grain and medium-grain rice is calculated at 622,000 acres, down 10.4% YoY and the lowest since 2001. In California, short- and medium-grain acreage was estimated at 445,000 acres, down 13.6% YoY.

Long-grain exports have stumbled under the weight of a global rice surplus, with marketing-year sales down 23.2% YoY. But a recent sale to Iraq is stirring hope of a sustained export recovery as global rice acres shrink. Medium-grain rice growers in California are enjoying strong and steady exports to Japan. Marketing-year export sales are up 4.1% YoY following last year’s trade negotiation between President Trump and Japan. Globally, rice acres are expected to decline for the first time in seven years amid high productions costs and a world glut of subsidized Indian rice.

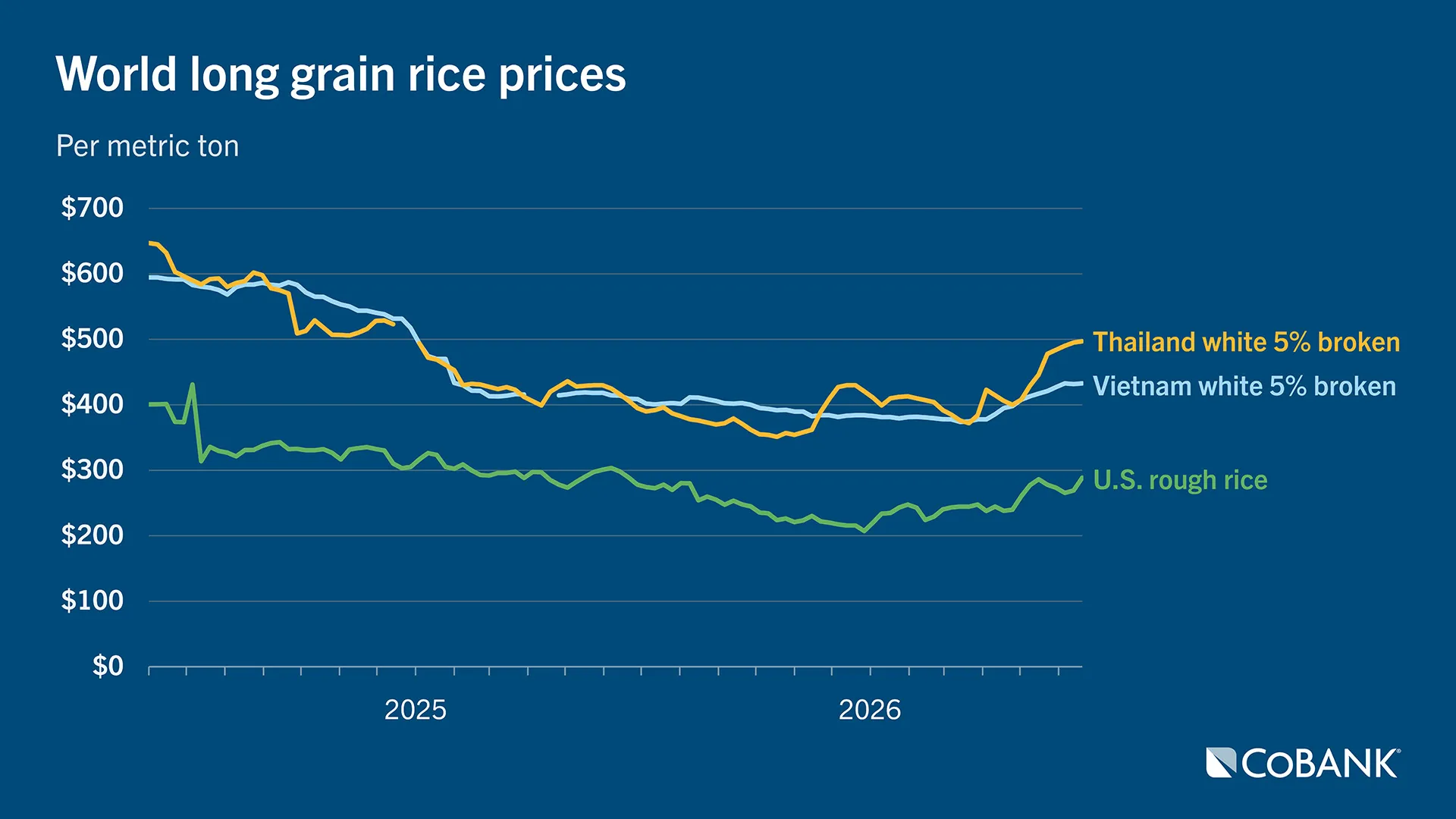

India’s record-large rice stockpile pulled prices to multi-year lows. But anticipation of a smaller world crop and record demand is awakening a price recovery, with CME rough rice prices up 20.7% last quarter. Concern is also building over India’s new kharif rice crop, which accounts for roughly 80% of India’s annual rice harvest. Indian farmers are struggling with weak monsoon rains and hot temperatures at planting time. India typically accounts for 40% of global rice exports.

The U.S. long-grain crop is starting the growing season in solid condition with crops in all six growing states rated above 70% good-to-excellent, according to USDA’s Crop Progress report. For farmers to be profitable, they will need optimal yields and a sustained price recovery. Large U.S. carryover stocks will give U.S. rice millers a needed buffer against the expected significant drop in long-grain production.

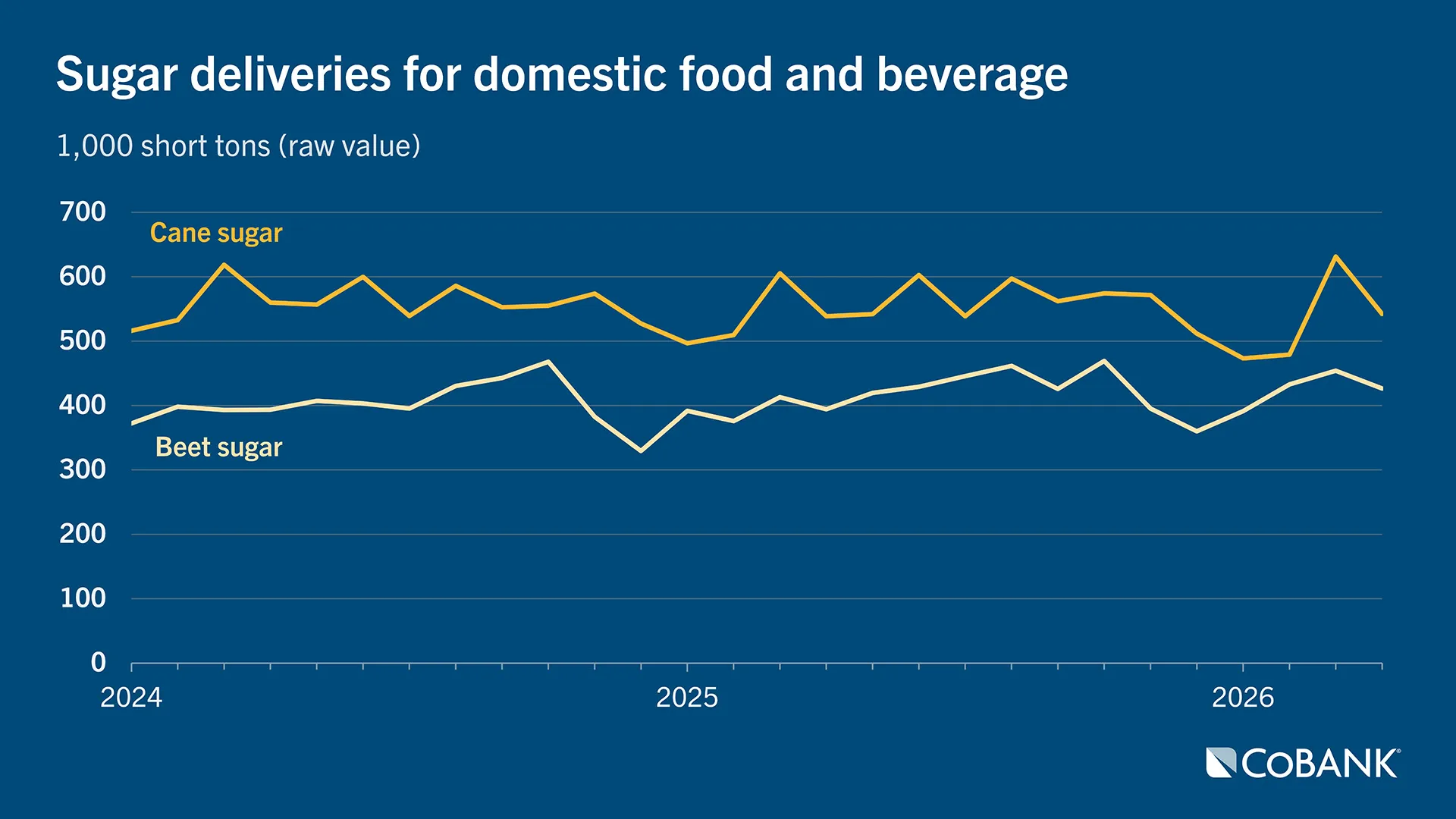

Sugar

Sugar prices are caught in a tug-of-war. Global supplies remain ample after record harvests in Brazil and India, pushing world raw sugar prices down 5.1% last quarter. But U.S. raw sugar prices last quarter rose 2.9% as domestic production fell and demand continued to grow.

In the U.S., beet and cane sugar production combined is expected to fall 5% YoY to the lowest level in seven years. Reduced beet acreage and frost damage to Florida cane sugar fields are weighing on production. Domestic sugar deliveries, meanwhile, for both raw cane sugar and refined beet sugar are rising as consumers shift from high fructose corn sweeteners and other artificial sweeteners in favor of natural sugar.

Globally, sugar stocks are abundant following a record harvest. The International Sugar Organization (ISO) expects a global surplus of 2.2 million metric tons in 2025/26, up from a deficit of 3.46 MMT the prior year. Still, world production could decline in 2026/27. ISO predicts a 1.1% YoY drop as a “Super” El Niño could crimp global production, particularly in major exporters such as India and Thailand. Higher ethanol blending mandates in Brazil and rising biofuel prices in the wake of the U.S.-Israeli war with Iran are also diverting more sugar to ethanol production, further raising the risk of tighter global supplies.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.