The oil shock isn’t over — and rural America is still exposed

Key points

- Oil market aftershocks could persist for quarters or years as inventories rebuild and Middle East stability remains uncertain.

- Strategic reserves and commercial stockpiles are becoming central to energy security planning after repeated global supply shocks.

- Global energy volatility hits rural America especially hard with higher fuel, power, farm and supply-chain costs.

Global energy shocks rarely stay confined to oil markets. They show up in fuel bills, electric rates, farm expenses and supply chains — costs that often hit rural households, businesses and electric cooperatives first. To provide insight on what the current energy environment means for these stakeholders, Teri Viswanath spoke with energy expert, Kevin Book, managing director of research at ClearView Energy Partners. His perspective helps translate a fast-moving geopolitical disruption into practical questions about resilience, cost exposure and the policy choices that will shape energy affordability for rural consumers. More importantly, he emphasizes that this chapter in America’s history on geopolitics and oil will likely leave a mark.

Teri Viswanath: Kevin, I heard your remarks at a gathering in D.C., roughly a week before the U.S. announced a peace agreement with Iran. In that address, you noted that even with a political resolution, rebalancing the physical market would be difficult, and prices would continue to reflect that tightness. Oil never reached $150, but your comments suggest buyers may still face aftershocks they are not fully prepared for. Can you explain?

Kevin Book: Teri, it’s hard to get a firm, real-time bead on oil market fundamentals because the data tend to lag and can require significant revision. Yet even conservative estimates suggest the Hormuz crisis resulted in significant stock draws — probably well more than half a billion barrels. Given the historically strong inverse correlation between global petroleum inventories and front-month Brent crude futures prices, this suggests it may be multiple to calendar quarters — and, in some scenarios, maybe years — before supply-demand balances and stocks return to status quo ante levels and prices revert to where they were.

Much depends on how fast shut-in Persian Gulf oil production restarts. Some producers have suggested they could be back to full output within weeks; others have indicated it may take them months. But demand might recover faster than supply. Consumption typically trends higher in the second half of the calendar year. And, demand contractions caused by an absence of supply can rapidly rebound (unlike more enduring demand “destruction” caused by structural changes in capital stock). In its latest report, the International Energy Agency sees a return to surplus as soon as the fourth quarter of 2026. But that might depend on stability in the Middle East. And it could be too soon to bet on that.

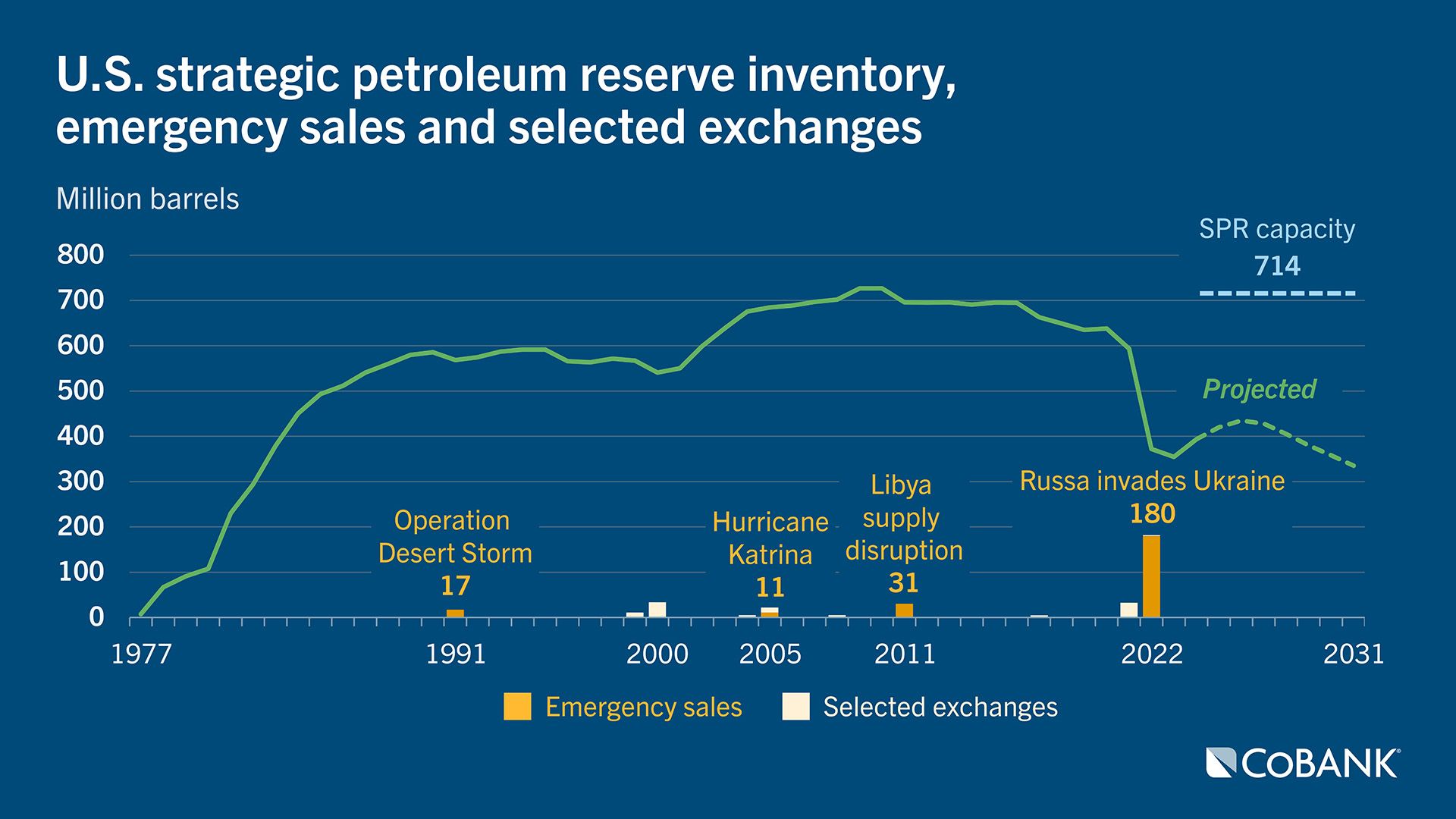

Viswanath: You also touched on the longer-term effects of this disruption and how it could reshape global thinking on energy security. There was a recent Financial Times op-ed piece, “The ‘new joule order’ is here. The west is last to realise,” (subscription required) where the author argues that “America is exporting its insurance policy,” noting that the extra barrels used for short-term global rebalancing didn’t come from new production but rather from storage. During the crisis, the Strategic Petroleum Reserve has fallen to the lowest level since August 1983 and is on track to hit a minimum level for operations by the end of summer. Let’s begin with our own energy security and then expand beyond our borders.

Book: Essentially, every importing economy is asking, “How do we make sure this never happens again?” Many are likely to be serious about the question because Hormuz was the second supply shock within a relatively short timeframe. This is reminiscent of the 1970s, when the 1973-74 Arab oil embargo was followed by the 1979-80 Iranian Revolution. If the first disruption focused minds, the second forced hands.

Then as now, importers seem likely to explore four broad, high-level solutions.

The first is to diversify sources and routes. In this respect, importers who previously might have prioritized proximity could give a new look to the U.S. and other Western Hemisphere producers. And as you mention, the U.S. has played a significant role in supplying tight global markets thus far. America can’t continue to deplete its commercial and strategic inventories forever, but this crisis could make it easier for some exporters to ink longer term supply deals — especially LNG producers looking to seal sale and purchase agreements with overseas counterparties.

The second is to build bigger inventories — both government strategic stockpiles and commercial ones. You mention the U.S. Strategic Petroleum Reserve, and you noted at the event that Pakistan is moving towards an SPR of its own. We might see more governments follow suit, but that’s not the only route to resilience. Governments can also mandate higher levels of commercial stockholding. And some commercial players — Persian Gulf producers especially — may see a case for expanding their inventories without government mandates.

For completeness, the other two solutions are an increased reliance on domestic energy, including electrification of end-use sectors, and ramped up efficiency measures.

Returning to the U.S. Strategic Petroleum Reserve: if the current volume commitment of 172 million barrels gets released, SPR inventories could fall to roughly 243 million barrels. That would be less than the 252.4 million barrels statutory minimum requirement for the president to be able to invoke his non-emergency release authorities (which is not a binding constraint). It’s also below the 250 million barrels that the Government Accountability Office recommended in the 1970s as a minimum inventory before considering a first draw (that wasn’t a binding constraint, either).

I believe the SPR could still operate down to 70 million barrels, and maybe below. There might be limited utility in the sludgy volumes at the bottoms of storage facilities. In addition, the DOE has indicated that flow rates will slow as inventory dwindles. But the main impact of repeated releases is that the U.S. — and the world — would have even less of a critical energy security resource available for the next supply emergency. And if I have learned anything over my career, there probably will be a next supply emergency.

Viswanath: If this episode exposed how little spare capacity and buffer the system really has, what practical lessons should policymakers and industry leaders take from it? Are we looking at a need to rethink strategic reserves, infrastructure resilience, or even the assumptions behind energy transition planning?

Book: Well, you mention spare capacity, and there generally isn’t much of it to be found outside of the production headroom OPEC member countries keep in reserve. It’s safe to say that both OPEC and importing nations generally prefer to fill supply gaps with flowing barrels instead of scarce stockpiles, but in this case, most of the producers’ group’s additional volumes were trapped by the Strait (along with much of Gulf states’ existing production).

For this reason, some importing nations seem likely to put money to work on option No. 3 — using domestic energy resources, including electricity generated within their borders. Given the small number of plug-in hybrid electric vehicles on the world’s roads today, electricity cannot immediately replace missing petroleum. But this wasn’t just about petroleum. Because the Hormuz crisis blocked flows of both oil and natural gas, it limited fuel substitution options in ways that seem unlikely to go ignored. When the Ukraine War cut off westbound gas flows to Europe, LNG cargoes that had been headed to Asia redirected to Europe, and Asian generators replaced some of that gas with liquids to fuel thermal generation. This time around, the world found itself short of both gas and liquids.

That’s likely to leave a mark. Deglobalization was already gaining momentum before the covid pandemic gave importers (of all kinds) reasons to re-examine just-in-time, globally sourced supply chains and consider putting more working capital into inventories and “just-in-case” resilience (including domestic clean manufacturing). Here, too, a second data point within a short interval seems likely to induce a certain amount of reflection. But I think Hormuz could cut two ways for clean energy transition.

On one hand, renewable electricity offers a mechanism for de-risking energy supply by keeping it within national borders. A switch to endogenous electrons might seem attractive after molecules went missing twice inside of five years. On the other hand, eliminating variable-cost risks associated with sourcing petroleum globally could introduce fixed-cost risks from imported transition metals, materials and technologies. Some governments might be leery of moving too far too quickly. Indeed, some countries will probably look again at their own domestic coal resources.

Viswanath: You suggested Washington has held unrealistic expectations that gasoline prices would return to $2.50 a gallon by the nation’s 250th anniversary. How has this disruption affected fuel inventories, and what should motorists reasonably expect for the rest of the year?

Book: It has been said that gasoline prices rise like a rocket and fall like a feather, and I can tell you that this rocket-feather phenomenon tends to generate as much criticism among political leaders as it does intellectual curiosity among academic economists. You might think that $4.50 per gallon gasoline would be a cut-and-dry catalyst for electric vehicle transition. But I have found that high prices tend to usher out elected officials faster than they usher in new technologies.

We are having this conversation on June 19, and the American Automobile Association’s national average regular gasoline price is now $3.97 per gallon. That’s about $0.59 per gallon below the recent peak on May 21 and about $1.01 per gallon below the nominal price in on this day in calendar year 2022 (during the turbulent early months of Ukraine War). But — sticking with nominal prices — it’s also $0.99 per gallon above the AAA average on Feb. 27, the day before the war broke out. Meanwhile, the Brent crude front-month futures price (the principal global benchmark for oil sales) is only $0.17 per gallon above Feb. 27 levels. Oil is the biggest component of U.S. fuel costs, so there’s room for pump prices to converge to the downside, and a similar dynamic applies to diesel, too.

But it might take a while. Refineries are running flat-out to supply domestic and international markets. That sounds like good news for consumers, because refined products supplies can dampen prices. But when facilities forego maintenance, they sometimes encounter serious problems. And disruptions to domestic fuel processing can drive up pump prices, too, even if the effects of refinery outages tend to be more localized.

Viswanath: As you look ahead, what indicators will tell you whether this episode marks the start of a more lasting repricing of energy? And which signals are you watching most closely to gauge where markets go from here?

Book: In a world of two-second video clips and 24-hour news cycles, it can be easy to miss early signs of significant changes. This is particularly true in energy, where supply tends to be sticky because infrastructure has long lead times and long lifetimes, and demand tends to be inelastic due to a combination of behavioral and pocketbook constraints. In this case, it doesn’t look like energy prices rose high enough or stayed there long enough — so far, anyway — to induce the sorts of innovation and investment which might significantly augment the supply side.

But I wouldn’t bet against meaningful demand-side changes.

For example, the average light-duty vehicle on American roads is now roughly 13 years old. That suggests a big replacement cycle could be in the offing, and with it, a possible transition into higher-efficiency vehicles even if they are not electric ones. In other countries without tariff and non-tariff barriers to low-cost Chinese EVs, I would expect adoption rates to climb.

When one looks back the fourth response I listed — efficiency — it’s easy to discount the possibility of transformation, because efficiency standards tend to draw backlash (it’s hard to get re-elected in America on a platform of small cars and hot buildings).

But small cars and hot buildings really have more to do with austerity (doing less with less) than efficiency (doing more with less). New technologies can change the game, too. Case in point: replacing incandescent bulbs with LEDs reduces watts per lumen by something like 85%. That might induce some upside demand response — “Jevon’s Paradox,” in economics literature — but demand for lumens was pretty saturated. Plus, even if you did leave your lights on 24 hours a day, in most conventional use cases the substantial efficiency gains from LED bulbs would probably lead to net savings.

In this context, one new technology that has been getting a lot of headlines for its energy consumption — artificial intelligence — might also enable energy savings in buildings and industrial processes (by scheduling demand and distributing load, and by optimizing business plans and processes). In circumstances where demand is closer to saturated, resulting savings could potentially outstrip induced consumption, perhaps even net of the energy the AI consumes.

Of course, in the more immediate foreground, it’s probably worth watching how the U.S.-Iran peace process plays out.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.